Multi-Factor Indexes Made Simple

Blog post

June 24, 2015

Institutional investors are increasingly gravitating towards multi-factor allocations as the preferred approach to factor investing. But how should factor indexes be combined?

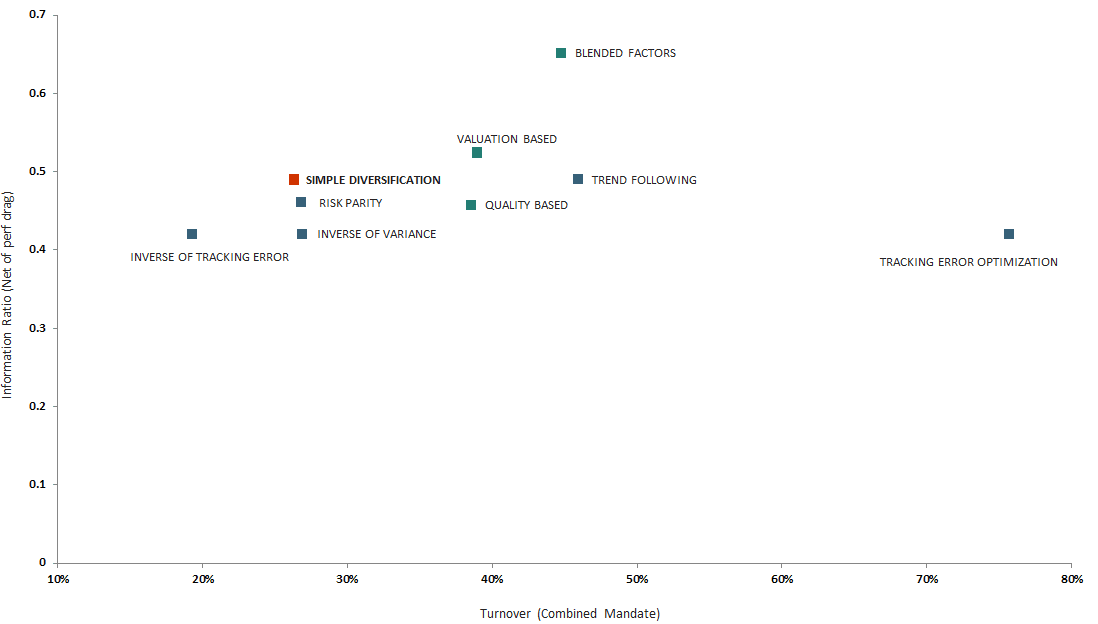

We studied return and risk characteristics of nine static and dynamic factor weighting strategies based on 36 years of MSCI live and simulated factor index history. They included one simple equal-weighted strategy (Simple Diversification); five rules-based/optimization-based weighting strategies (Inverse of Variance, Inverse of Tracking Error, Trend Following, Risk Parity and Tracking Error Optimization); and three fundamentals-based weighting strategies (Valuation-Based, Quality-Based and Blended Factors). Except for equal weighting, the other eight strategies involved dynamic adjustment of factor weights.

Our analysis found that a Simple Diversification strategy that equally weighted six factor indexes has historically proven more effective than many of the more complex approaches, especially after accounting for index turnover cost. This approach may appear naïve in construction but offers simplicity, transparency and robustness and can serve as an attractive starting point for factor allocation — especially where investors do not have active investment views and skills.

In addition, we also found that the fundamentals-based approaches have produced attractive results in simulation. The three strategies tested in this study have delivered higher active returns than the Simple Diversification strategy – pointing to the potential benefits of exploiting fundamental insights in the construction of a multi-factor index. Such strategies, however, are active in nature and typically come with the extra "costs" of higher turnover and greater complexity. Thus, the decision depends on the investors' investment beliefs and process and — critically — whether the investor believes she has the insight or skills to manage factor exposures dynamically.

The relative merit of each strategy as measured by the information ratio versus turnover — a key element of cost — can be seen in the below exhibit.

Information Ratio vs. Turnover of Multi-factor Indexes

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.