Multi-Factor Strategies Highlight Benefits of Diversification

Blog post

March 14, 2016

The cyclicality of factor strategies means that individual factors can deliver a premium against the market over time but that any one factor can experience periods of underperformance.

Institutional investors can alleviate the effects of cycles by diversifying their portfolios across several factors. A year ago, MSCI introduced Diversified Multi-Factor (DMF) Indexes for use in constructing portfolios that are exposed to multiple factors.

The indexes track the performance of four factors—value, momentum, quality and size—while maintaining risk at the level of the underlying parent index.

So how have these strategies performed, and have they tilted consistently toward their targets? And which factors have contributed to outperformance?

Twelve months represent a relatively brief period to assess performance, but the experience of the DMF indexes merits attention for two reasons.

First, it shows the performance of live strategies as opposed to backtests. Second, the year was marked by a falloff in equities and a rise in volatility. It remained to be seen how the indexes would respond, especially without low volatility among the target factors.

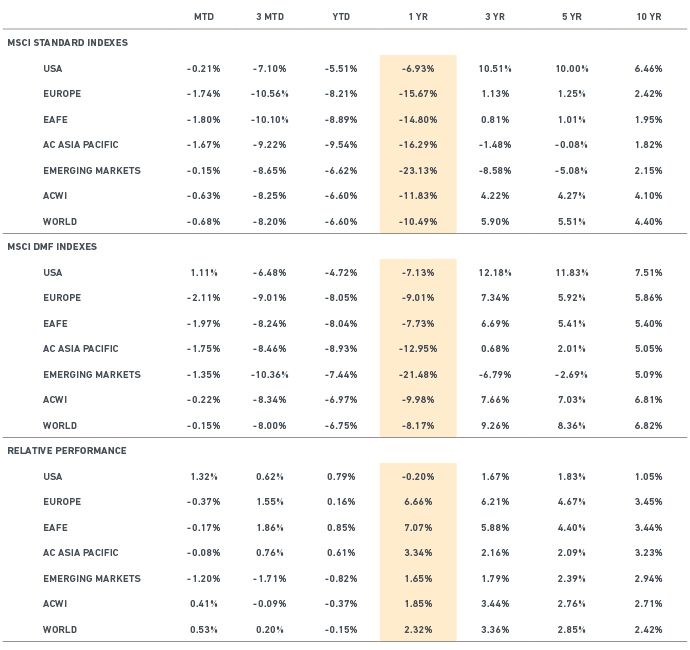

As the table below indicates, the DMF indexes outperformed their benchmark in six of seven regions worldwide over the year that ended February 29.

Data as of February 29, 2016, Gross Total Returns, USD. Actual (annualized) return for periods shorter (longer) than 1 year.

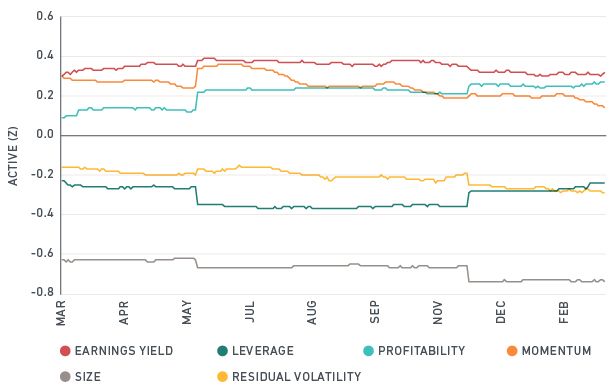

To see what influenced this performance, we analyzed the MSCI World DMF Index through the lens of the latest Barra Global Equity Total Market Model. The chart below shows that the index provided exposure—positive or negative—to its target factors consistently over the period.

World DMF exposures (year ending Feb. 29)

For example, because the DMF indexes tilt toward the quality factor, the portfolio tends to seek companies that exhibit high profitability and low leverage compared with the broad market. Another tilt, toward value, explains why the portfolio maintains a positive exposure to earnings yield compared with the market. The chart further shows that the DMF indexes had low exposure to the residual volatility factor. This factor is negatively correlated with size and helps to hedge the significant low-size tilt of the DMF strategy.

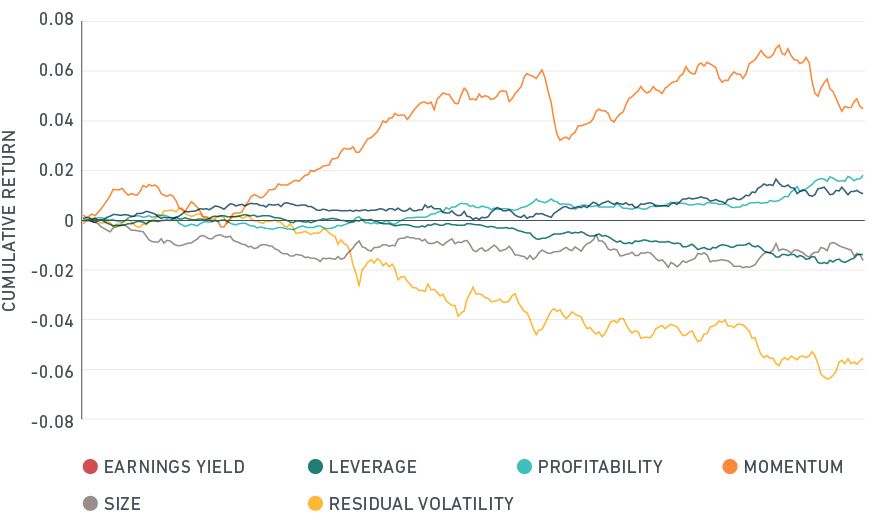

The chart below highlights the advantage of a diversified strategy. Over the past year, investors in the broad market generally rewarded momentum and low residual volatility. Thus, if the DMF indexes held stocks that were exposed to these factors, the strategies should have and, in fact, did harvest some of that positive excess return. Tilts toward value provided low excess returns over the same period.

Global factor returns (year ending Feb. 29)

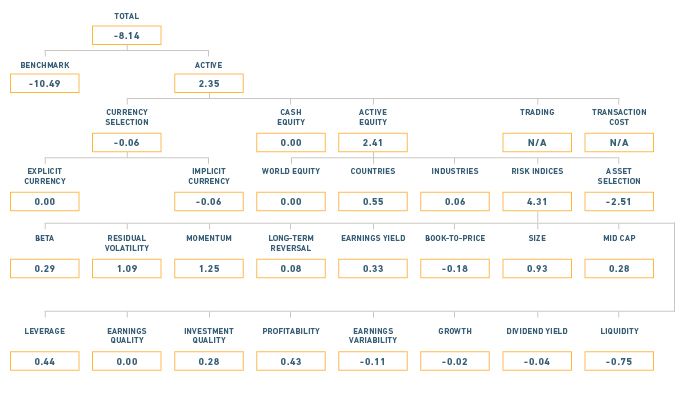

Finally, investors can decompose excess return for the MSCI World DMF Index, which, as the table below shows, outperformed the broad market by 2.35% over the period.

Momentum, which contributed the most to alpha, added 125 basis points. The two size factors (size and mid cap) added 121 bps. The quality factors (leverage, earnings quality, investment quality, profitability and earnings variability) contributed 104 bps. By contrast, value factors (book-to-price and earnings yield) only added 15 bps.

Thus, the DMF strategy targeted three factors that generated positive returns over the last 12 months and one (value) that did not. Taken together, the strategies paid off and provided further evidence that combining factors may confer the benefits of diversification.

Further reading

The MSCI Diversified Multi-Factor Indexes: Maximizing Factor Exposure While Controlling Volatility

Deploying Multi-Factor Index Allocations in Institutional Portfolios

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.