No Country for Old Firms? Revisiting Growth and Thematic Investing

- Thematic equity investing has gained wide traction with financial advisors and retail investors, but a critique voiced by institutional investors has been its similarity to traditional growth investing.

- While growth stocks generally focus on rising earnings and sales, thematic stocks tend to be aligned with longer-term, structural megatrends. We found that growth indexes could have overlooked sustainable and energy-related firms.

- A simulated multi-thematic approach outperformed a traditional growth index over the past half-decade, due in large part to its overweight to more 'thematic' firms.

Splitting the difference

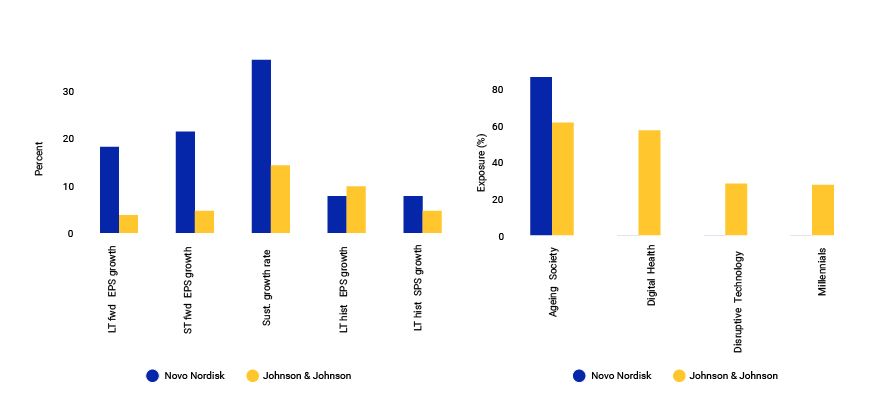

As previously mentioned, a primary difference between growth and thematic investing is fundamentals. Growth firms usually have a track record of rising earnings and sales, while thematic firms typically have an economic linkage to a longer-term, structural megatrend, but without the prerequisite of recent growth. As an example, we look at two venerable, century-old pharmaceutical firms, Denmark's Novo Nordisk A/S and Johnson & Johnson of the U.S. Novo Nordisk handily bests Johnson & Johnson across most growth measures, such as forward earnings estimates and sustainable growth rate (left plot below). As a result, it is classified as a growth firm and included in the Growth index.3

Two similar firms with different growth and thematic characteristics

EPS and SPS refer to earnings per share and sales per share, respectively. Only themes with non-zero exposure are shown. Fundamental data and thematic exposures as of Sept. 30, 2022.

The picture is quite different, however, when viewed through a thematic lens. Far from being a dated centenarian, Johnson & Johnson has a sizeable presence in four themes based on MSCI's Thematic Exposure Standard, shown in the right plot above. As a result, while it is not included in the Growth index, it is included in corresponding MSCI indexes based on its thematic footprint.

Some themes are less growth-oriented than others

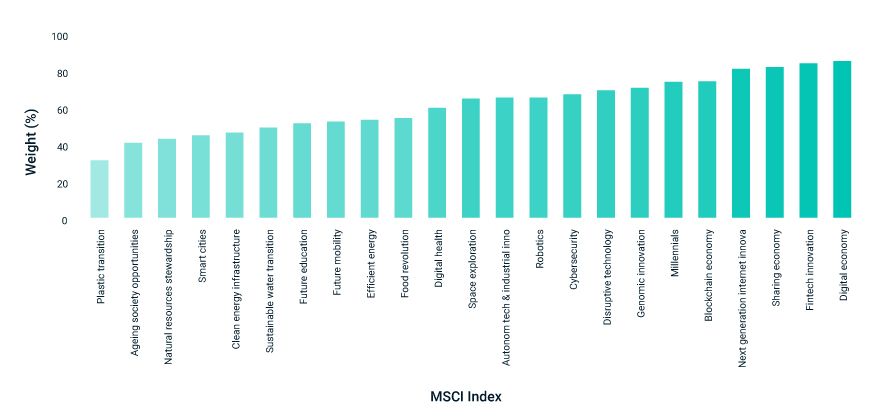

Given that backdrop, we examined the growth composition of MSCI's thematic indexes. We found that the degree of overlap with 'pure growth' stocks varied widely by thematic index (shown below).4 Some indexes such as the MSCI ACWI IMI Digital Economy Index and MSCI ACWI IMI Fintech Innovation Index were largely composed of pure growth firms that were classified as a growth stock. Other indexes, including many sustainable and energy-related themes, historically have had a much smaller share of growth-oriented firms. That implies that a traditional growth investing style could have overlooked many of the firms most aligned with these themes.

Weight in growth firms varied across thematic indexes

Weights are monthly averages from the earliest common date for all indexes. Dec. 2016 through Sept. 2022.

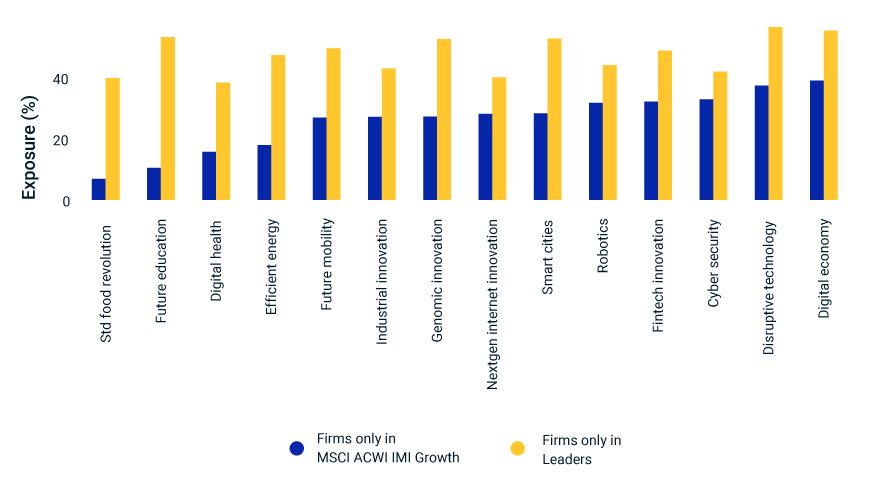

Combining multiple themes didn't overload on growth stocks

We examined the effects after combining several individual themes together. We used the "Leaders" approach, which selects firms that scored the highest across several themes while preserving investability characteristics. We found that Leaders and Growth did not have a large overlap. Leaders historically had about a third of its weight in firms not found in the Growth index, while the Growth index had about 60% if its weight from firms not found in Leaders. Importantly, the firms unique to the Growth index tended to have a lower exposure to the selected themes (shown below).

'Growth only' firms tended to have lower thematic exposures

Only those themes that the Leaders approach aims to capture are shown. Exposures are the average across all firms in each cohort as of September 2022.

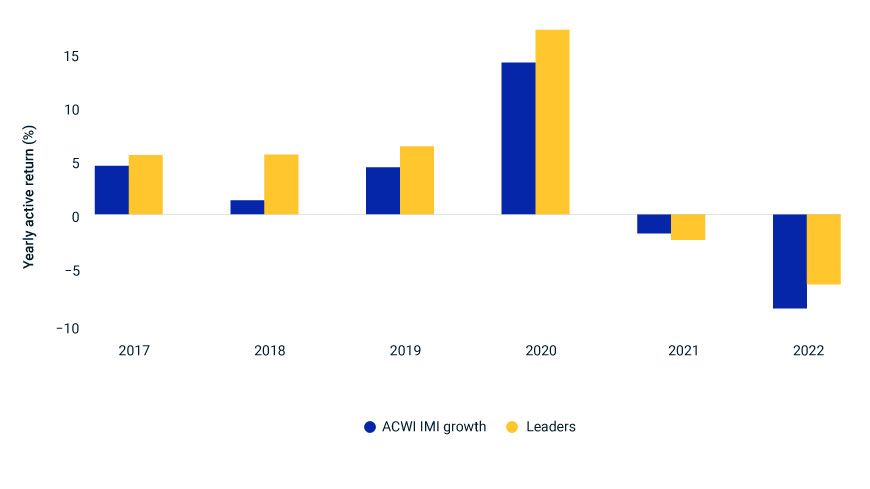

Those differences help explain the outperformance of the Leaders approach relative to the Growth index over the past half-decade (shown below). Notably, the Leaders approach has been more resilient than the Growth index throughout the recent slide in equity markets. Furthermore, our research reveals that the bulk of Leaders' longer-term outperformance was due to its overweight in high-scoring, thematic firms.

Leaders outpaced Growth since 2017

Returns are annual gross in USD and relative to the MSCI ACWI IMI Index.

Shining a light on the long term

Lastly, the firms in the Leaders approach have seen their weight in the broader market (as represented by the MSCI ACWI IMI Index) rise from about 25% in 2017 to just under 40% today. While this change has occurred only over the past five years, it could herald a tendency where established firms continue to relinquish share to those that are best aligned with longer-term trends. Whether they are upstarts or rejuvenated incumbents, thematic investing can complement traditional growth investing by illuminating those disruptors.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 Abdulla, Mahmood, Atlantic Council, “The startup industry is struggling. Here’s how founders can navigate the current funding environment,” Nov. 1, 2022.2 Higgins-Dun, Noah, CNBC, “The IPO market went from ‘boom to bust’ in 2022. Here’s what’s driving the massive slowdown,” Sep. 23, 2022.3 Note that we only show the growth characteristics of the two firms. Valuation characteristics also determine how much of a firm’s capitalization is attributed to MSCI Growth and Value indexes.4 A pure growth firm refers to a firm whose market capitalization is fully attributed to an MSCI Growth index. Per MSCI Value and Growth index methodology, firms can be wholly growth or value, or in less frequent cases, a combination of the two.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.