Real Estate's Income Risk in an Inflationary World

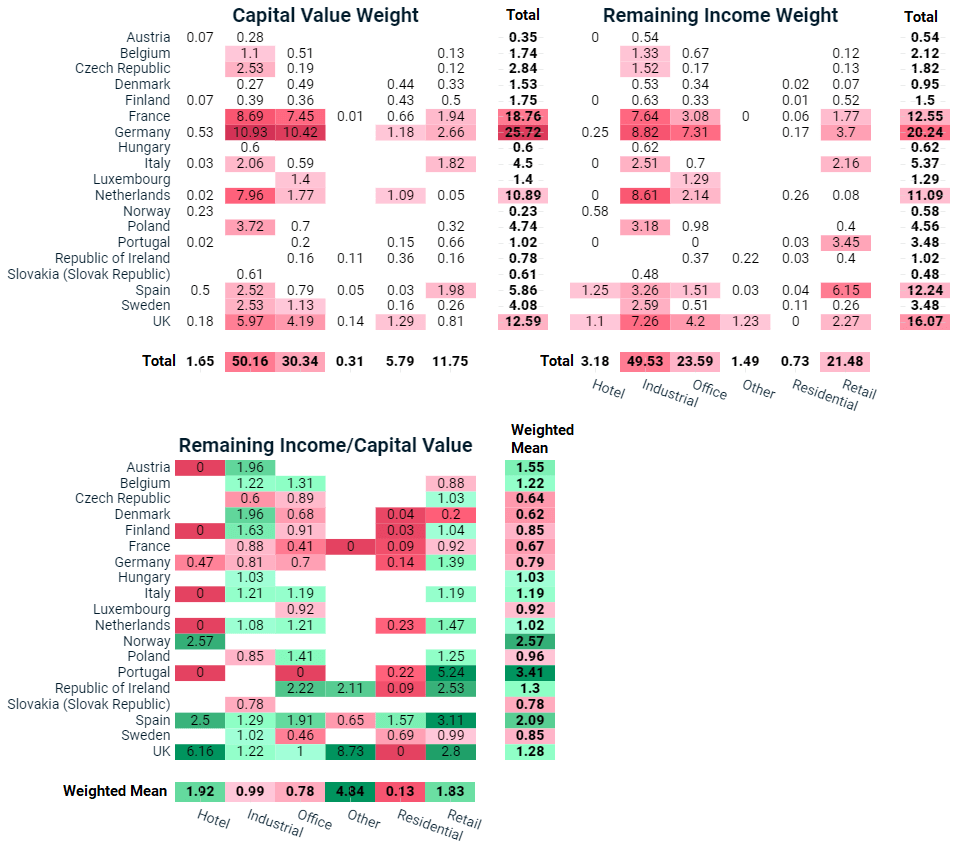

- The constituents of the MSCI Pan-European Quarterly Property Fund Index have, in aggregate, more significant exposure to industrial and retail property types, when measured by remaining income instead of by capital value.

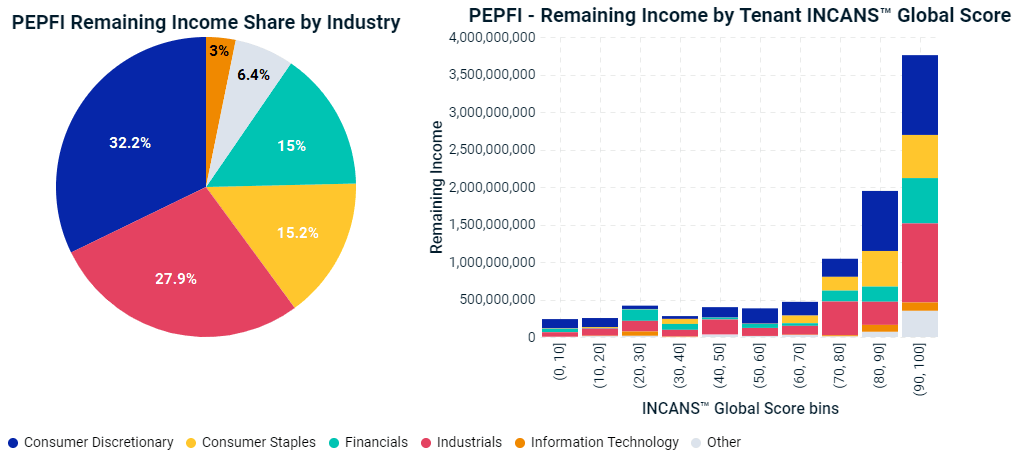

- Three-quarters of remaining income is contracted to tenants in the consumer-staples, consumer-discretionary and industrial segments.

- The majority (60%) of remaining income was owed by companies that had an INCANSTM Global Score above 75, equivalent to a BBB- or better bond rating and deemed to be of investment grade.

Real estate income varied greatly below the index level

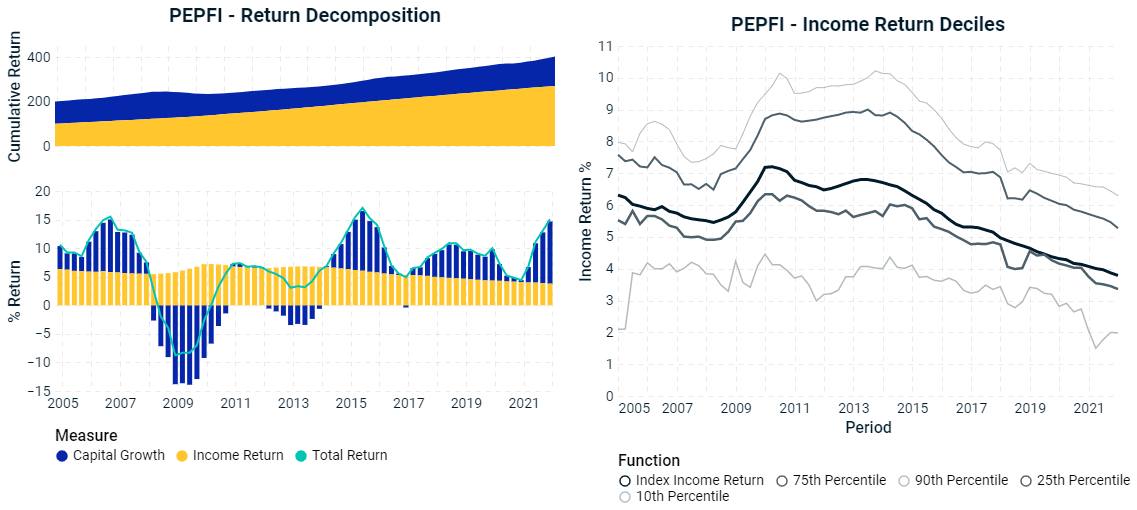

Although real estate income returns have tended to be stable in aggregate, the right-hand chart below illustrates the extent to which they have varied across individual properties in the MSCI Pan-European Quarterly Property Fund Index (PEPFI). For many investors, risk analysis focuses on the measurement of capital exposure across property types and geographies. But with income return making up such a significant part of long-run returns, it may make sense for investors to understand income exposure across tenant types, concentration risk to individual tenants and the probability of default on rental payments.

Income return constituted the bulk of total return over time

Exposure analysis through an income lens

Investors usually think of their exposures in terms of capital value, but the exhibit below highlights how exposure to property types and geographies can look different when measured instead by remaining income, or the total amount of contracted income outstanding on the lease up to the next break-clause date.2

The upper-left panel in the exhibit below shows the capital-value weight by property type and country across PEPFI. The right-hand panel shows the weight of remaining income. This provides an indication of what proportion of the PEPFI's contracted rental income was derived from a particular sector-geography pair. The lower panel shows the ratio of the two to highlight the extent to which exposure differed on the two measures.

In general, across many countries, exposure to industrial and retail was higher when measured by remaining income than by capital value, as indicated by the green cells in the lower matrix. The opposite has often been true for residential and office. Across countries such as the U.K., Spain and Italy, we have seen consistently higher exposures to remaining income than capital value across all property types. France and Germany, countries with high exposure in 2021 on both capital-value and income bases, saw the opposite, with significantly less weight to income than capital value. The main drivers of these trends were yield and lease length, which both determine the relationship of remaining income to capital value and varied themselves by property type and country.

Income as an alternative measure of exposure

The bottom-left panel shows the ratio of a given country-sector pair's "Remaining Income" weight (as a percentage of the overall index) to its "Capital Value" weight. The vertical "Weighted Mean" column is the ratio of the "Remaining Income" weight by country to the "Capital Value" weight by country, and the horizontal "Weighted Mean" is the ratio of the "Remaining Income" sector-totals row to the "Capital Value" by industry segment.

Property type can hide a range of economic exposure to tenant industries

Classifying portfolio tenants by industry can provide an alternative lens for analysis, showing, for example, that three-quarters (75.3%) of remaining income was contracted to tenants in just three segments: consumer staples, consumer discretionary and industrials. The split between consumer discretionary and consumer staples may be particularly important since an asset's property-type designation as "retail," for example, may obscure important characteristics about tenants' industry exposure and how it affects their ability to pay rent. For example, a significant proportion of the income from a retail asset may be derived from nonretail tenants or from retail subsegments, like consumer staples, which may be more resilient to online retailing and inflation than consumer discretionary.

Looking through to tenant industry and default risk

Income risk varied across — and within — industries

Looking through to tenant industries may give investors a better sense of the economic drivers of income, but leaves a lot unsaid about the risk of default, which can vary significantly across tenants within industries. The combination of tenant industry with the INCANSTM Global Score, a proprietary score of tenants' payment-default risk, is illustrated in the right-hand panel above. 60% of remaining income was owed by companies that had an INCANS Global Score of above 75, equivalent to a BBB- or better bond rating and deemed to be of investment grade. While most income from financial tenants was concentrated in the lower-risk end of the spectrum, income from tenants in consumer staples and industrials was spread right across the default-risk spectrum.

Identifying individual companies with outsized exposure and risk

Often tenant companies have complex holding-company structures that make tenant concentration risk difficult to estimate, especially for cross-border portfolios. It is especially relevant to track corporate structures if parent companies grant rental-payment guarantees to the landlords of their child companies, since the default risk is likely to be lower. By looking at aggregated income of parent companies, in conjunction with the weighted average default-risk scores, it may be possible to spot specific tenants that contributed disproportionately to the risk of the overall portfolio.

Highlighting company exposures of concern

Loading chart...

Please wait.

We found that PEPFI constituent funds were most highly exposed to companies that tend to have lower default risk, indicated by their higher-than-average INCANS Global Scores. The company with the highest rental-income exposure was a financial company with relatively low risk of default. Exposure to this company was less significant when measured by remaining income due to relatively short leases. The opposite was true for the grocery-store company that had the second-highest remaining income exposure. Both companies have reasonably strong covenants. Of more concern may be the industrials company to the left of the left-hand chart above, because of its significant income exposure and relatively weak covenants.

In an environment of rising inflation and interest rates, investors may become more focused on the resilience of their real estate income streams. Continual monitoring of income risk can help investors understand the economic exposure behind their returns and the risk of their tenant's default on rental payments. Going beyond aggregate-portfolio analysis may help investors identify concentrations of risk tied to geographies, tenant industries and individual companies across their holding structures.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1“2021 Institutional Real Estate Allocations Monitor.” Hodes Weill & Associates and Cornell Baker Program in Real Estate, Nov. 10, 2021.2Calculated as the gross rent passing multiplied by the remaining lease term (i.e., to the first break clause).

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.