Regional Blocs: Emerging to Diverging Markets

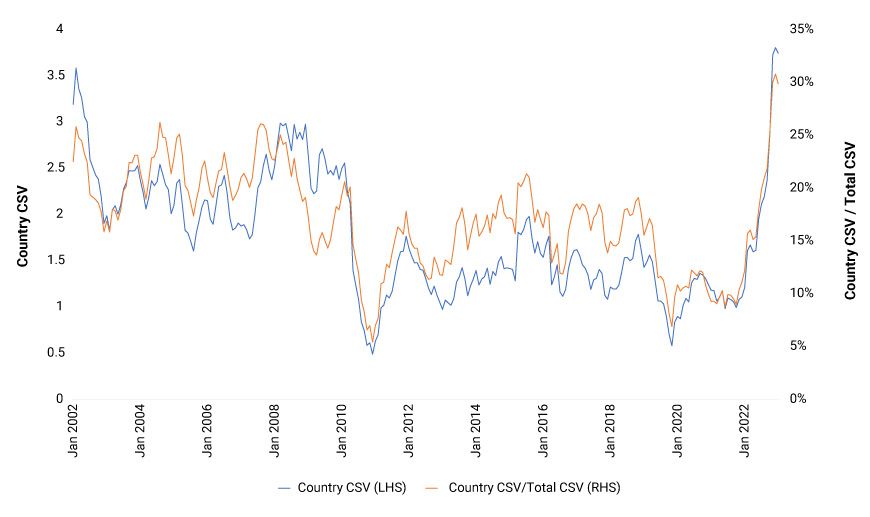

- The dispersion of emerging markets returns driven by country rose to historic highs in 2022, as deglobalization proceeded at an accelerated pace.

- Institutional investors responded to this trend by seeking more nuanced ways to allocate to emerging markets.

- Using geographical blocs can create a more flexible way of managing allocations to emerging markets, by capturing diversification benefits while avoiding the complexity of decision-making at the country level.

Cross-sectional volatility in the MSCI Emerging Markets Index

Data as of Jan 31, 2023.

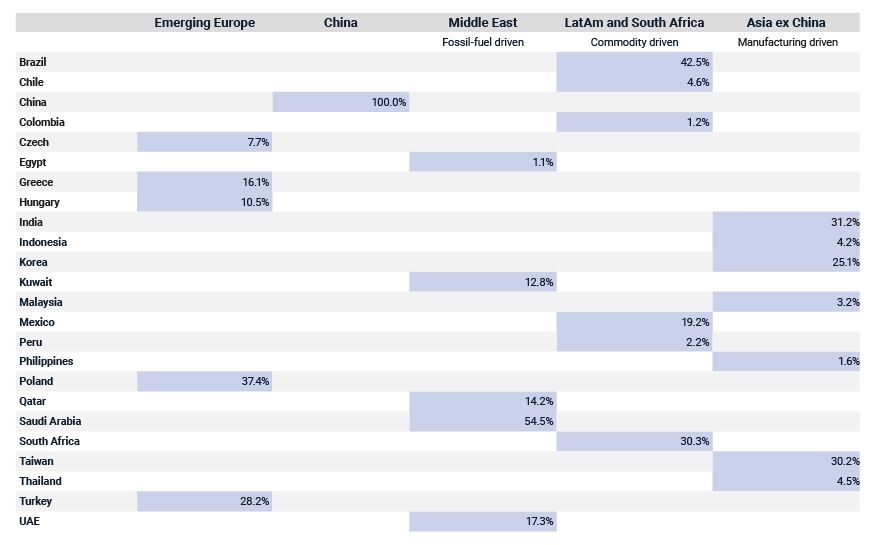

A diverse set of building blocs

A potential reaction to this dispersion has been the consideration of distinct allocations to China and EM ex China.1 By separating China, the largest EM country, allocators are aiming to manage country risk by assembling a more diverse EM portfolio. EM ex China includes countries with diverse economic fundamentals, industrial structures and varied exposures to market and geopolitical risks. However, the segregation of China may not provide enough flexibility in allocation decisions or achieve greater diversification.

Looking at it from another lens, a nuanced way to create an EM allocation is to focus on individual countries as the macro portfolio building blocks. While this level of granularity may provide ample opportunity for distinction and diversification, and may be suitable for some investors, others may not have sufficient resources to make 24 allocation decisions (one for every country in the MSCI Emerging Markets Index). We investigated the potential of remaining flexible in order to the achieve diversification benefits, while still maintaining a level of reasonable simplicity. We looked at how the risk-return tradeoffs would change when investors replaced a broad EM allocation (where they make just one allocation decision) with the following options:

- An allocation to China and EM ex China (two allocation decisions).

- An allocation to five geographic blocks (five allocation decisions).

- An allocation to individual EM countries (24 allocation decisions).

Country weights within regional blocks

As of Jan. 31, 2023.

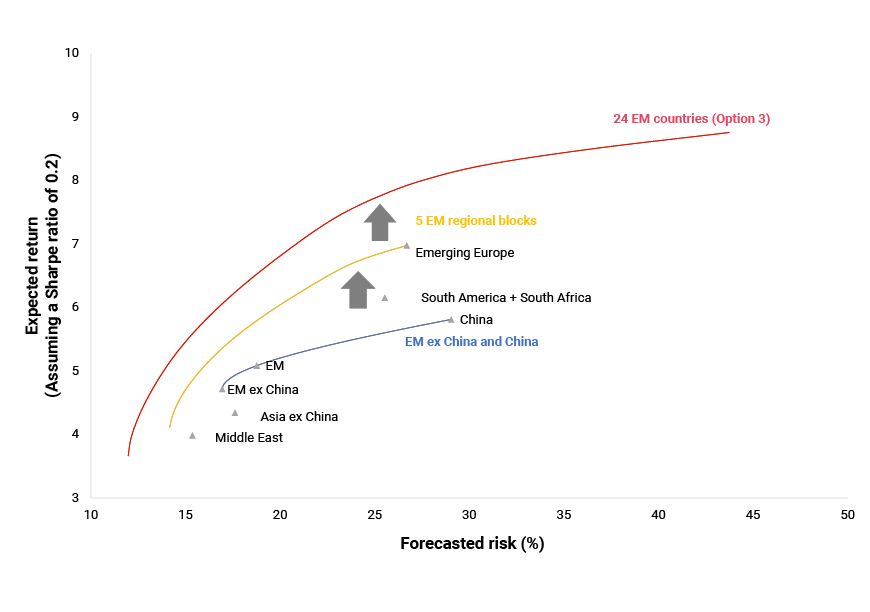

EM: The efficient frontier

We constructed efficient frontiers for the three options, using the covariance matrix from the MSCI Global Equity Factor Model and expected returns that assume an equal Sharpe ratio across all EM countries (as shown below).2 The MSCI Emerging Market Index is on the efficient frontier formed by MSCI China and MSCI EM ex China Indexes.3 Moving from one allocation decision to two provides enhanced portfolio-positioning flexibility with a greater choice of levels of risk and return. However, if investors take on the risk of the MSCI EM Index,4 they would still have to accept the same expected return as the EM index.

Moving to option three would involve ramping up the number of decisions from one to 24 decisions, but it has potential to enhance the risk-return tradeoff. Under our assumptions, for the same expected return as the EM index, the forecasted risk would be reduced from the 18.8% to 14%. The cost, however, is a significant increase in decision making complexity.

In comparison, option two provides a middle ground. Under our assumptions, for the same expected return as the EM index, the forecast risk could be reduced from 18.8% to 16.1% at a cost of only a mild increase in decision making complexity. The practical implication is that using blocks of similar countries can help allocators gain diversification benefits and create more allocation opportunities, while limiting the decision-making complexity.

The efficient frontiers of EM allocations

Data as of Jan 31, 2023.

The examination of allocations

Given the need for some institutional investors to construct more nuanced allocations to EM, would it be possible to construct an approach that offers greater flexibility and greater potential diversification benefits, while at the same time preserving parsimony? If we selected five geographical blocks of EM countries with similar return attributes, this may allow for the construction of a more flexible allocation to EM without decision-making making at the individual-country level. We believe a similar approach could be applied to developed-market equities and fixed-income markets, which have also been impacted by deglobalization.

The author would like to thank Anil Rao and Roman Mendoza for their contributions to this blog.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Asset-allocation decisions can vary significantly from market-classification decision. Simply, asset allocation aims to identify opportunities for differentiated returns, while market classification reflects institutional investors’ experiences of market accessibility and economic development.2Our aim is to show the potential for diversification, rather than forecast expected returns. We made an assumption that a unit of risk taken in each country’s equity market is equally rewarded with expected return. We assumed an expected Sharpe ratio of 0.2 for each EM country, and used the forecasted risk of the MSCI country index to back out an expected return. The forecast risk was obtained from the MSCI Global Equity Factor Model. The value of 0.2 is close to the historical cross-sectional mean across EM countries over the past 20 years. As long as a positive Sharpe ratio is assumed, its level does not impact the conclusions.3This is always the case, as EM is a linear combination of EM ex. China and China.418.8% as of January 31, 2023.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.