Repo-market turmoil may not spell SOFR’s end

Blog post

October 24, 2019

- The recent spike in the rates of U.S. repurchase agreements (repo) has raised concerns over the greater volatility in the secured overnight financing rate (SOFR) relative to LIBOR benchmark rates, as SOFR is based on the repo market.

- Most market participants do not rely on the overnight repo market for funding. But because SOFR will be widely used as a benchmark rate, many market participants could be indirectly impacted by repo-market volatility.

- End users may demand appropriate averaging of rates based on SOFR to smooth out excessive volatility in the repo market.

What caused the spike?

Last month's turmoil in overnight repo was attributed by some observers to a combination of factors — including a large volume of Treasurys that settled, and a large amount of corporate tax payments that came due, on those dates.3 But these events were expected well in advance, so they may not fully explain the SOFR turbulence. More recent analysis attributed much of the spike to particularities in the cash management of an increasingly small number of dominant players in the repo market.4

Repo disturbance can ripple outward

One of the primary reasons the Alternative Reference Rates Committee selected SOFR as a benchmark risk-free rate is that it reflects transactions from a large and liquid market. While the repo market is vast — with hundreds of billions of dollars in daily outstanding volume5 — the September spike highlights the obscure market frictions that can drive the repo rate. Most market participants that do not rely on the overnight repo market for funding were not directly impacted by these frictions. But they were indirectly affected, due to SOFR's use as a benchmark for setting various borrowing rates beyond the repo market.

The challenge of smoothing out SOFR volatility

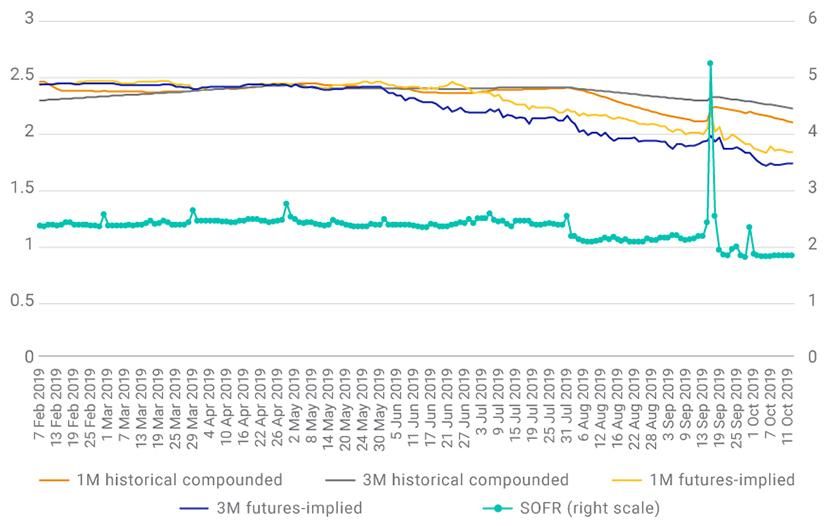

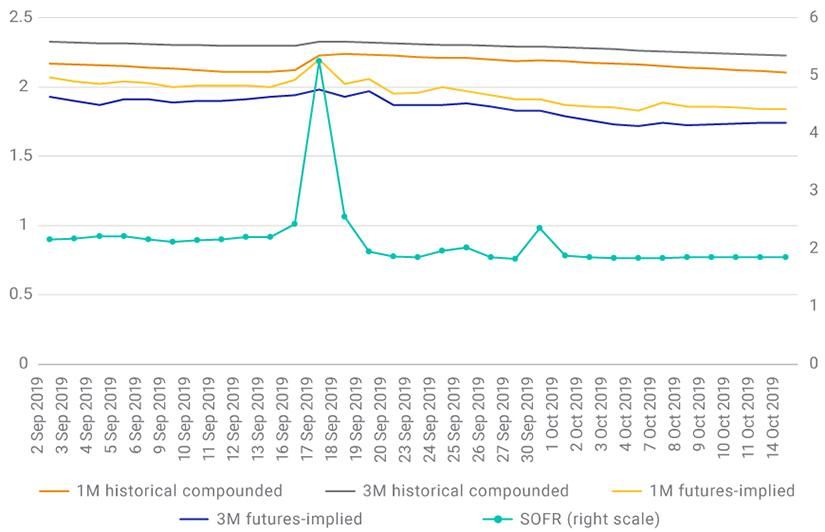

Industry participants have argued that an average or compounded overnight rate will need to be used to reflect the relevant borrowing term.6 However, the recent spike reveals the limitations of averaging: The 30-day compounded in-arrears average rate spiked by 13 basis points (bps) in response to the one-day spike in the overnight rate. The spike only became muted when using a medium-term average such as a 90-day average, where the resulting increase was 3 bps, as the exhibit below shows.

Using average or forward-looking repo rates mitigated daily benchmark-rate volatility

Top chart captures data from Feb. 7, 2019, through Oct. 14, 2019. Bottom chart zooms in on data from Sept. 2, 2019, through Oct. 14, 2019. Source: Federal Reserve Bank of New York, MSCI

Another proposal to accommodate certain cash-market users is to use a forward-looking SOFR term rate derived from derivatives. This could also smooth out short-term fluctuations in the overnight SOFR rate.7 However, the September spike also spilled over into the futures market. In fact, the 30-day futures-implied rate spiked by 15 bps before coming back down to pre-spike levels the following day. The 90-day futures-implied forward rate, in contrast, increased by 4 bps. In general, the forward-looking term rates were more volatile than the historical averages (as the exhibit above shows) — and exposed end users to spikes in overnight rates due to the possibility of their term rate's resetting on a day when future expectations were inflated.

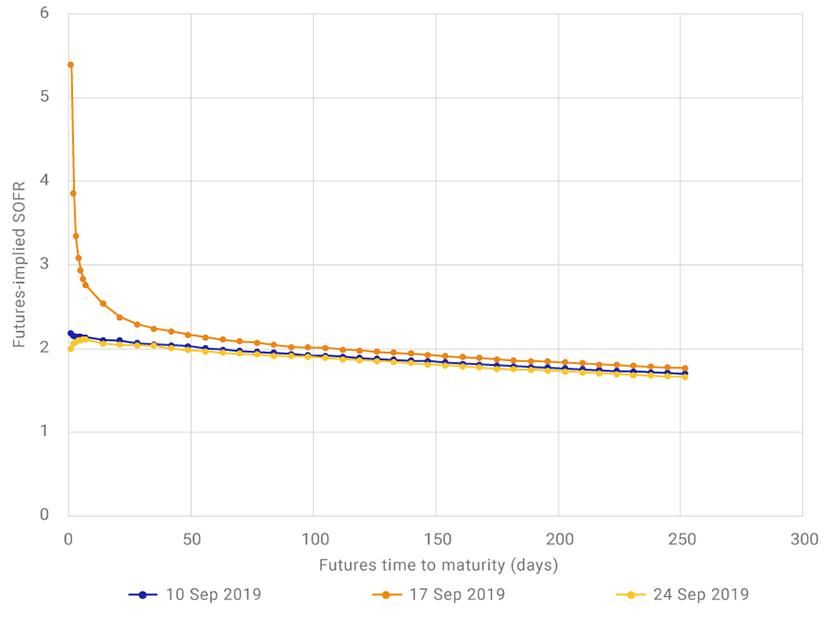

SOFR futures curves suggest that the market did not anticipate the Sept. 17 spike — and does not anticipate subsequent spikes

Source: MSCI RiskMetrics® DataMetrics®

The Fed has supplied liquidity through mid-October,8 and communicated plans to start increasing its balance sheet,9 to guard against such significant spikes. The SOFR futures market reflected market expectations that spikes will not recur: The expected future SOFR rate reverted to pre-spike levels within a few days of the spike, as shown in the exhibit above. Still, as SOFR increasingly becomes the standard reference rate, demand for stable rates from end users requires appropriate averaging to guard against potential volatility in the repo market.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The Alternative Reference Rates Committee selected SOFR, the interest rate on secured overnight loans collateralized by Treasury securities, to replace LIBOR in 2022.2“Repo gyrations bode ill for move away from Libor.” Financial Times, Sept. 19, 2019. “Repo-Market Tumult Raises Concerns About New Benchmark Rate.” Wall Street Journal, Sept. 23, 2019.3“Repo-market ructions were a reminder of the financial crisis.” Economist, Sept. 26, 2019.4“Big Banks Loom Over Fed Repo Efforts.” Wall Street Journal, Sept. 26, 2019.5“US Repo Market Fact Sheet, 2019.” Securities Industry and Financial Markets Association, Sept. 18, 2019.6“A User’s Guide to SOFR.” Alternative Reference Rates Committee, April 2019.7Heitfield, E. and Park, Y.-H. “Indicative Forward-Looking SOFR Term Rates.” Federal Reserve Board, April 19, 2019.8“New York Fed to continue operations in overnight funding market until mid-October.” CNBC, Sept. 20. 2019.9“Fed to resume asset purchases to prevent a cash crunch.” Financial Times, Oct. 8, 2019.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.