Resilient carbon-transition portfolios: a road map

- Transition to a low-carbon global economy may expose investors to significant risks associated with fossil-fuel dependent companies.

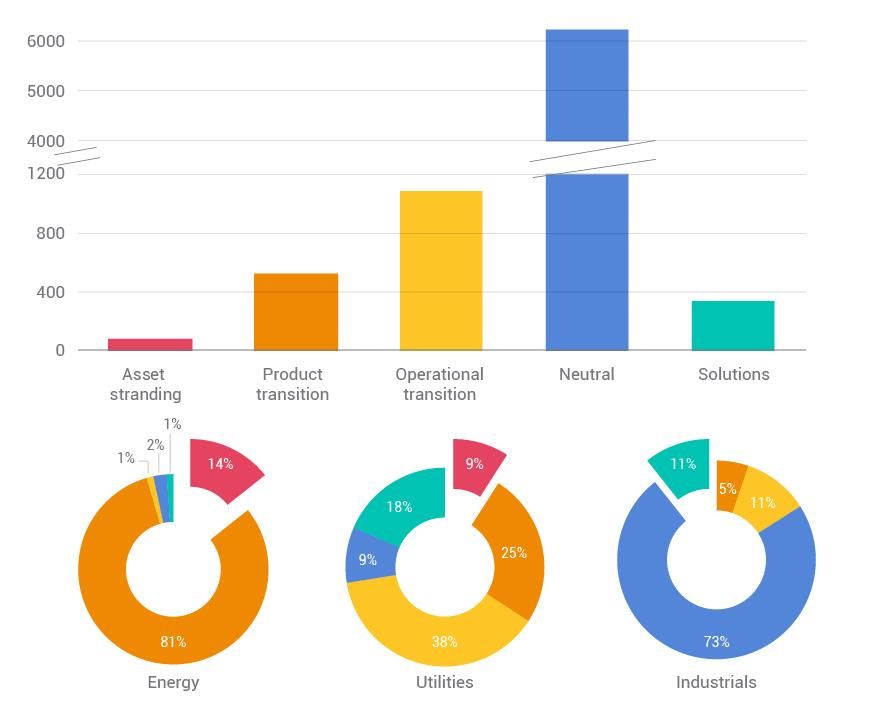

- Energy and utilities sectors were most exposed to "asset-stranding" risks. Those standing to benefit were those companies offering low-carbon products and solutions as well as those firms equipped to adapt their business models.

- Identifying leaders and laggards can be used by portfolio managers to mitigate fossil-fuel risks and capitalize on clean-tech opportunities.

LOW CARBON TRANSITION CATEGORY | LOW CARBON TRANSITION RISK / OPPORTUNITY |

|---|---|

LOW CARBON TRANSITION CATEGORY ASSET STRANDING | LOW CARBON TRANSITION RISK / OPPORTUNITY Potential to experience "stranding" of physical or natural assets due to regulatory, market and technological forces arising from "low- carbon" transition. |

LOW CARBON TRANSITION CATEGORY PRODUCT TRANSITION | LOW CARBON TRANSITION RISK / OPPORTUNITY Reduced demand for carbon-intensive products and services. Winners and losers are defined by the ability to shift product portfolio to low-carbon products. |

LOW CARBON TRANSITION CATEGORY OPERATIONAL TRANSITION | LOW CARBON TRANSITION RISK / OPPORTUNITY Increased operational and capital cost due to carbon taxes and investment in carbon emissions mitigation measures leading to lower profitability of companies. |

LOW CARBON TRANSITION CATEGORY NEUTRAL | LOW CARBON TRANSITION RISK / OPPORTUNITY Limited exposure to "low-carbon" transition risk. Companies could face physical risk or indirect exposure to transition risk via lending, investment operations. |

LOW CARBON TRANSITION CATEGORY SOLUTIONS | LOW CARBON TRANSITION RISK / OPPORTUNITY Potential to benefit through the growth of low-carbon products and services. |

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.