Same target, different destinations

Blog post

July 31, 2019

- Target-date funds have gained wide adoption in U.S. defined-contribution plans due partly to the ease of selecting investments based on retirement date.

- Features such as glidepath philosophy and choice of a "to vs. through" retirement design go only so far in explaining differences across funds with the same target date.

- We show how modern risk models can further illuminate the reasons for these differences and identify where a fund's risks may lie.

Identifying differences

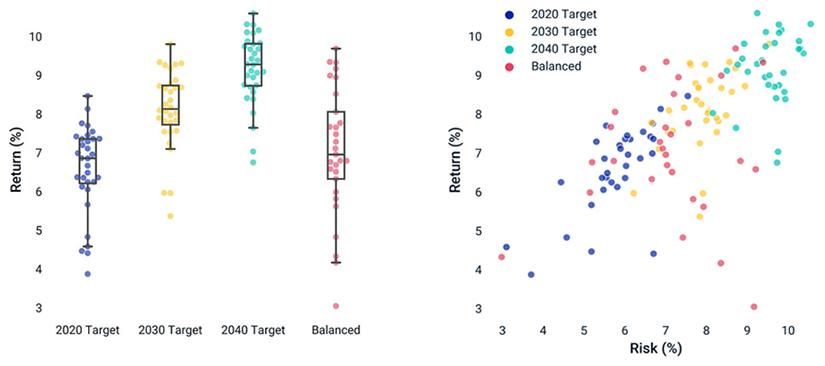

We start by examining the returns of funds across three target retirement dates: 2020, 2030 and 2040 (approximately 30 in each cohort) from 2016 to 2019.1 The average equity allocation for each of these targets is increasingly aggressive, at about 50%, 70% and 80%, respectively. We also looked at traditional balanced funds for comparison.

Given the upward-trending equity market of the last three years, it's perhaps unsurprising that the 2040 funds, on average, delivered the highest returns.

One interesting finding is that the TDFs in our sample had a tighter range of outcomes when compared to balanced funds, whose return and risk spanned across those of all three target dates. However, as expected, we also noted wide dispersion within the same target-date cohort even over the relatively short three-year period of our analysis.

Risk and return dispersion was wide within target-date cohorts

Data from Jan. 1, 2016, to March 31, 2019. Each point represents one fund. Annualized returns and risk are calculated from eVestment monthly returns. Only funds with continuous returns for the full period are included. The average return is used for similar funds with multiple share classes

What lies beneath

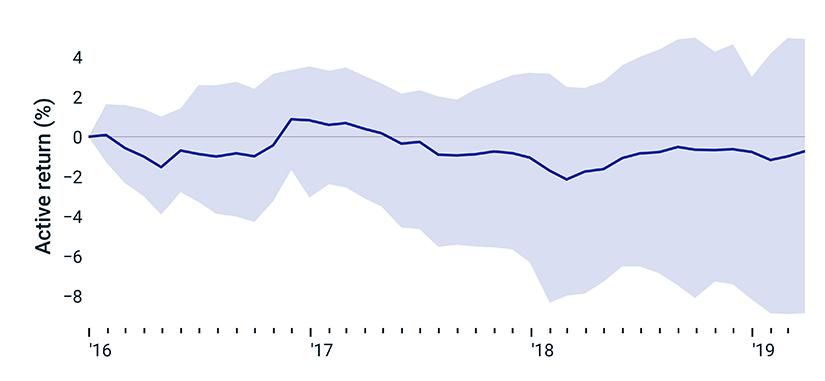

To gain a better understanding of the reasons behind these differences, we first compare how the funds performed compared to a benchmark.

Benchmark choice for TDFs is varied: peer-based, blended and even equity-only indexes are used. For our analysis, which we'll confine to the 2030 cohort, we select a blended benchmark composed of 70% the MSCI ACWI IMI (equity index) and 30% the Bloomberg Global Aggregate Bond Index (representing the average allocation for our sample of 2030 funds).

On average, the funds we analyzed kept pace with the benchmark. However, the range between the top and bottom performer was wide, ranging from a -8% to 4% relative return, as of the end of March 2019.

2030 fund returns vs. the benchmark varied widely

Data from Jan. 1, 2016, to March 31, 2019. The benchmark return is represented by 70% MSCI ACWI IMI Index in gross USD and 30% Bloomberg Global Aggregate Bond Index in USD.

Same path, different shoes; same building, different views

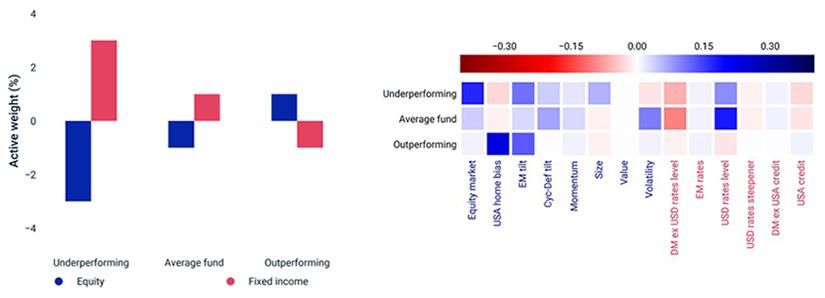

Next, we take three funds from the 2030 cohort — an underperforming, average and outperforming fund — and compare their holdings against the 70/30 blended benchmark used above. We'll use the MSCI Multi-Asset Class (MAC) Factor Model to peer through the holdings to the underlying risk exposures.

The left side of the exhibit below shows the traditional split between equity and fixed income relative to the benchmark (active weights). The right-hand portion translates the active weights to the sources and levels of risk relative to the benchmark (active risk). While not shown, the overall levels of historical and forward-looking active risk were similar (approximately 200 basis points) for each of the funds.

Additionally, all three funds in our example generated risk from their underweight to emerging-market equities. Their tilts toward equity factors such as momentum, size, value and volatility were also generally muted.

Yet their largest sources of active risk were quite different:

- The outperforming fund's largest source of risk was its overweight to the U.S. equity market. It was so large, in fact, that it obscured most of the other equity and fixed-income tilts in the fund.

- The underperforming fund's principal risk was its underweight to equities. To a lesser, but still meaningful extent, it also had a bias toward larger stocks.

- The average fund's largest source of risk was its sensitivity to U.S. interest rates, despite its slight underweight to equities. Why was this the case? It may be that, other than its exposure to riskier, more volatile stocks, its equity allocations were the most similar of the three funds to the benchmark's equity allocations.

Three funds with three different sources of risk

Active weights are shown relative to the blended benchmark. Risk decomposition is shown relative to the blended benchmark using Tier 2 of the MSCI MAC Factor Model. Holdings and model estimates are as of February 2019. Fund holdings are taken from publicly available information and represented using the MSCI Peer Analytics fund universe.

Measure twice, cut once

Peering deeper into TDFs can help providers, consultants and plan sponsors move beyond traditional explanations for risk and return differences between funds with the same target date — and provide a more detailed, nuanced view of how portfolios are constructed.

1 Years 2016 to 2019 represented the longest period where there was a large enough sample set of funds that met the criteria of continuous monthly returns.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.