Selecting the Blend of Factor Indexes

Blog post

December 9, 2014

Many institutional investors have struggled to determine the appropriateness of factors for their own plan, what role these allocations might play, which factors should be adopted and how factor indexes can be used.

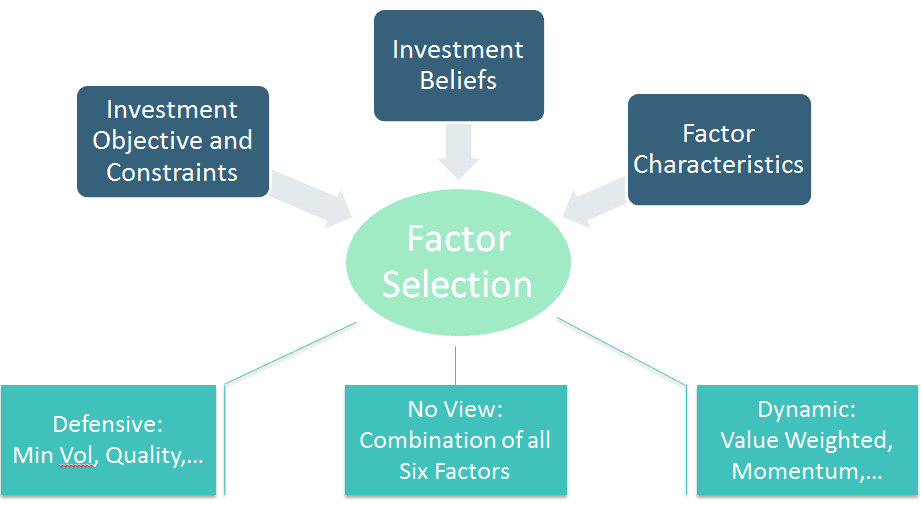

First, investment objectives and constraints, including evaluating the internal governance structure and establishing key constraints such as risk tolerance, should be assessed

Then, factors should be selected. Certain factors have strong theoretical foundations and have historically earned a persistent premium over long periods. We have identified six such factors: Value, Low Size, Low Volatility, High Yield, Quality and Momentum.

Finally, implementation options should be explored. Here, we focus on passive implementation based on indexes. The plan's objectives and constraints inform the combination of the factors chosen and the degree of investability required in the factor allocation. As an example, very large allocations may not be capable of implementation for certain highly concentrated or long/short strategies.

Is Combining Factors Easier than Timing Them?

The institution's objectives and constraints drive the factor allocation decision, not the indexes themselves, a point that is often lost in the arguments about why one index might be superior to another. Choosing a factor index is one of a number of an implementation decisions that turn the objectives, goals, and factor beliefs into actual allocations.

Simply focusing on a particular index's rules and construction process leads to the slippery slope of data-mining. There are thousands of options for generating indexes by varying the weights or criteria for selecting constituents.

Instead, institutional investors should focus on factors they believe will persist in the future. For example, an institution seeking to enhance risk-adjusted returns may be looking for a somewhat more aggressive allocation (higher return and higher risk), a defensive allocation (moderate return and lower risk), or a balanced allocation (something in between).

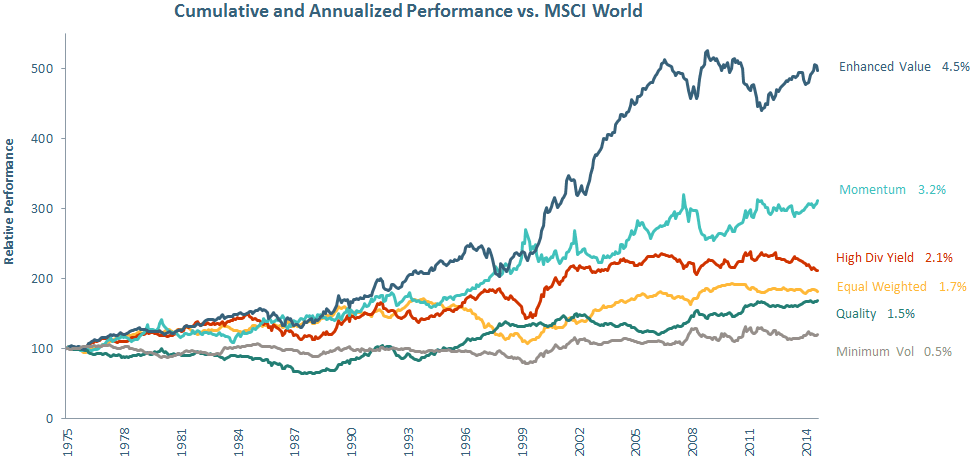

Next, factor selection should also take into account the correlations between factors, which affects portfolio-level risk. Factor returns have historically been highly cyclical.

But while individual factor returns have been cyclical, their periods of underperformance have not been identical. Systematic factors have historically been sensitive to macro-economic and market forces but not in the same way.

There is also strong empirical evidence that factors performed differently over various parts of the business cycle. Some factors such as value, momentum and size have historically been pro-cyclical, performing well when economic growth, inflation and interest rates are rising. Other factors such as quality and low volatility have historically been defensive, performing well when the macro environment was weak. Similar to macro business cycles, investors may seek factors that have performed well under different types of market cycles such as high/low market volatility.

Cyclicality is a key dimension

To recap, the key criteria are choosing an appropriate factor combination, risk, correlations with other factors and performance in different business cycles.

In sum, we think there is no universal factor solution, either in the form of a single factor or a combination of factors that is right for all institutions.

Read the paper, "Deploying Multi-Factor Index Allocations."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.