Small Caps - No Small Oversight

Blog post

December 9, 2014

Many institutional investors recognize that their reference universe should include large-, mid- and small-cap equities and that smaller companies should earn a risk premium over larger ones. In practice, however, many of these investors - particularly in Europe and Asia - underweight the small-cap segment.

Omitting small caps constitutes a significant active decision. An investor with a neutral view on small caps - that is, one who neither over- nor under-weights the global equity benchmark - would have had a small-cap allocation of 14%. Over the decade ending September 2011, excluding small-cap stocks would have forfeited 60 basis points of annual performance, while consuming as much as 50% to 75% of an asset owner's risk budget. In contrast, median out-performance of large- and mid-cap managers over the same period has been a modest 22 bps for U.S. portfolios and 36 bps for non-U.S. portfolios, based on eVestment data.

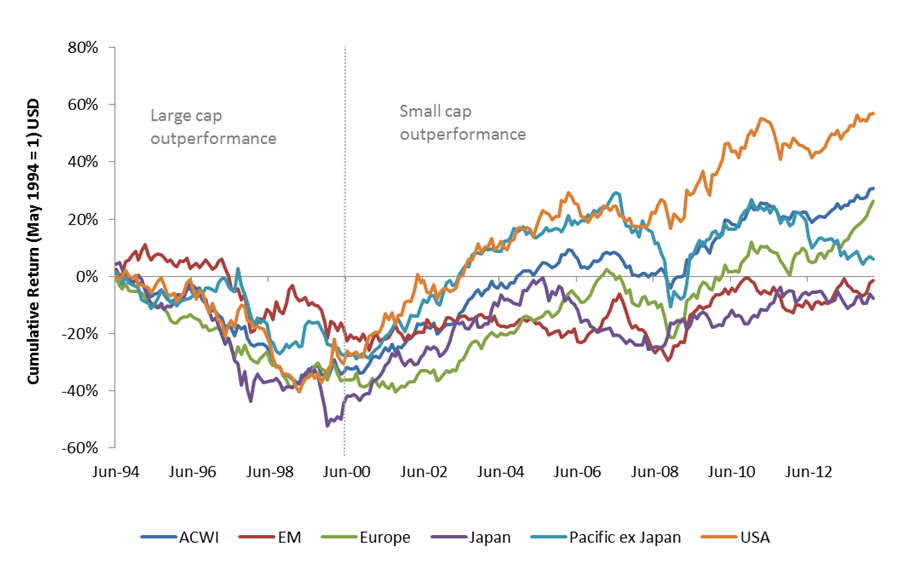

More recent data shows persistent outperformance by small-cap stocks, especially in the U.S.:

Historical performance of small caps around the world

Source: MSCI

We looked at what drives small-cap performance in a global portfolio, and we identified four important ways in which these stocks differed from those of larger companies. Perhaps the most important was small caps' sector tilt: industries with large economies of scale, such as energy and consumer staples, were under-represented, while the financial and consumer discretionary sectors were over-represented. This made small caps more cyclical and less defensive. Small caps also derived less revenue from abroad, were more likely to be owned by management and often differed in company fundamentals such as earnings growth.

What reasons do institutional investors give for excluding global small caps from their equity universe? Some are content with the implicit small-cap exposure they get from their large- and mid-cap managers who invest in small-caps opportunistically. Yet this consumes part of the risk budget, which should be used to find alpha, in beta exposure.

Some investors maintain that small-cap investing is too complicated, costly and resource-intensive and that it is hard to find good small-cap managers, particularly outside the U.S. We respond that they could get exposure to the segment through passive allocations. Alternatively, institutional investors can use alternative weighting schemes within small-cap stock portfolios as a way of efficiently capturing this factor premium.

We also find that, while trading costs for small caps are generally higher and liquidity is generally lower, the differences are not as large as some may have believed. If more institutional investors embrace this segment, liquidity is likely to improve, which in turn will drive the creation of products, resulting in a virtuous cycle.

To read the paper, "Small Caps - No Small Oversight," click here.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.