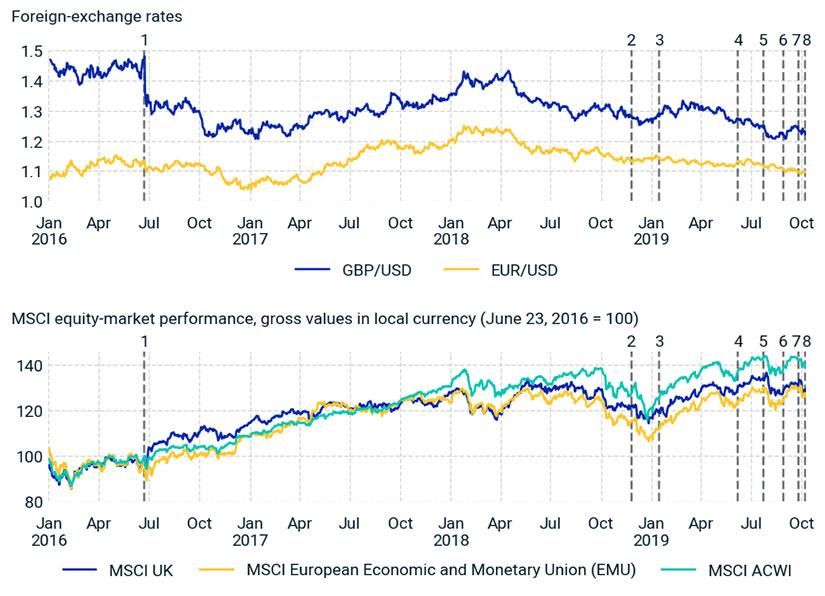

Stress testing Brexit: Deal or no deal?

- As the Oct. 31 deadline for Brexit nears, we look at the potential market impact of two possible scenarios: deal or no deal.

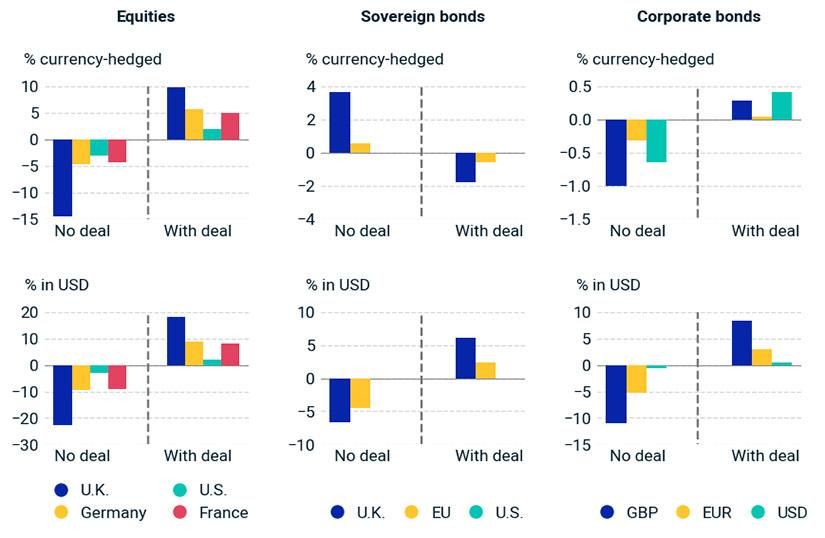

- In our stress-test scenarios, a disruptive no-deal scenario could weaken the U.K. equity market by 15% and the GBP by 10% relative to the USD, as well as hurt corporate-bond markets.

- If the U.K. and EU reach a last-minute deal, however, the U.K. equity market could gain by 10% and the GBP could rise by 8% relative to the USD.

Applied shocks | No-deal Brexit | UK leaves EU with a deal |

|---|---|---|

Applied shocks Equity predictive stress test Relative shocks | No-deal Brexit Equity predictive stress test Relative shocks | UK leaves EU with a deal Equity predictive stress test Relative shocks |

Applied shocks U.K. equity | No-deal Brexit -15% | UK leaves EU with a deal +10% |

Applied shocks German equity | No-deal Brexit -5% | UK leaves EU with a deal +6% |

Applied shocks U.S. equity | No-deal Brexit -3% | UK leaves EU with a deal +2% |

Applied shocks Interest-rate predictive stress test Absolute shocks in basis points | No-deal Brexit Interest-rate predictive stress test Absolute shocks in basis points | UK leaves EU with a deal Interest-rate predictive stress test Absolute shocks in basis points |

Applied shocks GBP 10-year govt. | No-deal Brexit -30 bps | UK leaves EU with a deal +15 bps |

Applied shocks EUR 10-year govt. | No-deal Brexit -10 bps | UK leaves EU with a deal +10 bps |

Applied shocks USD 10-year govt. | No-deal Brexit 0 bps | UK leaves EU with a deal 0 bps |

Applied shocks Credit stress test Relative shocks | No-deal Brexit Credit stress test Relative shocks | UK leaves EU with a deal Credit stress test Relative shocks |

Applied shocks U.K. credit spreads | No-deal Brexit +40% | UK leaves EU with a deal -15% |

Applied shocks EU credit spreads | No-deal Brexit +16% | UK leaves EU with a deal -10% |

Applied shocks Other credit spreads | No-deal Brexit +8% | UK leaves EU with a deal -5% |

Applied shocks Currency predictive stress test Relative shocks | No-deal Brexit Currency predictive stress test Relative shocks | UK leaves EU with a deal Currency predictive stress test Relative shocks |

Applied shocks GBP/USD | No-deal Brexit -10% | UK leaves EU with a deal +8% |

Applied shocks EUR/USD | No-deal Brexit -5% | UK leaves EU with a deal +3% |

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.