Surging Corporate-Bond Supply: Reason to Worry?

Blog post

July 1, 2020

- Net issuance of corporate debt surged in the aftermath of the March announcement that the Federal Reserve would begin purchasing corporate bonds and ETFs.

- Our analysis finds that corporate borrowers with poorly performing stock prices significantly contributed to this surge in supply.

- The increase in the corporate debt burden — already high going into the crisis — combined with a weakened economy, may be a potential warning signal to credit investors.

Turmoil Followed by Relief

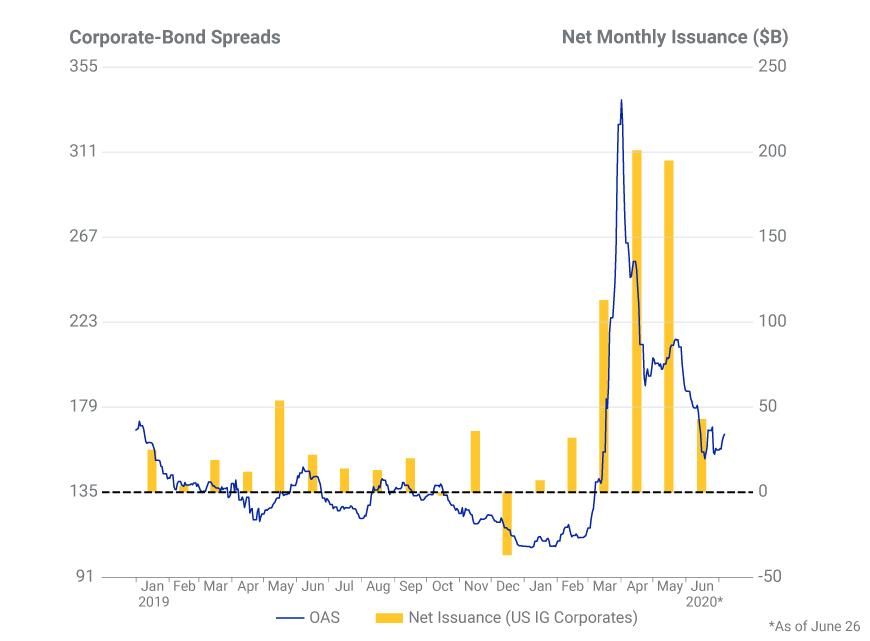

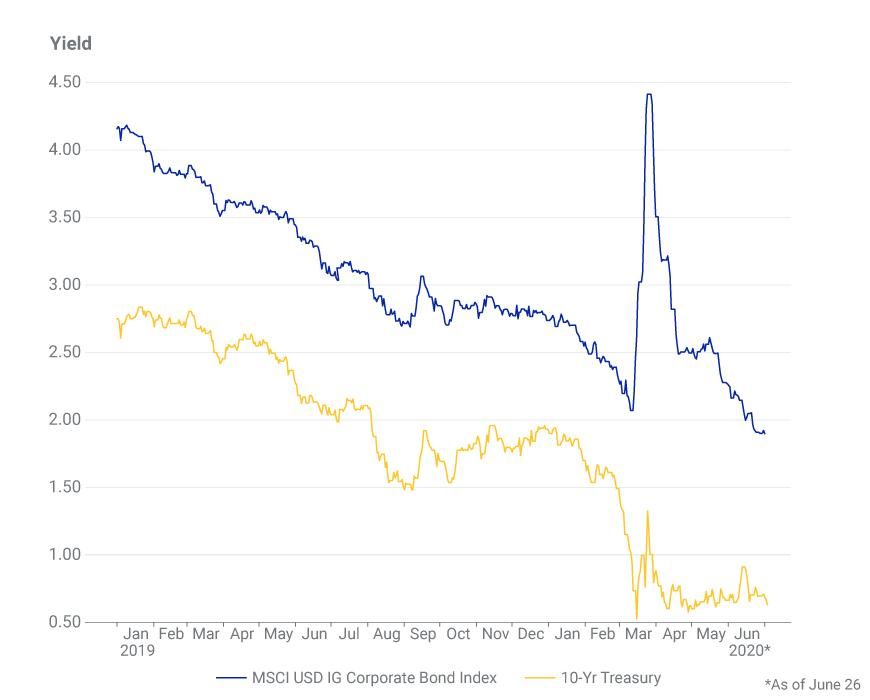

The impact of the coronavirus epidemic on the corporate-bond market was swift and severe. Between Feb. 19 and the peak on March 23, spreads of the MSCI USD Investment Grade Corporate Bond Index widened by more than 200 basis points (bps). Spreads tightened just as quickly after the U.S. Treasury Department and Federal Reserve announced the establishment of new facilities to purchase corporate bonds, with a goal of stabilizing the market and providing support for an eventual economic recovery. As of June 26, spreads were 165 bps, or about 73 basis points higher than just before the onset of the crisis.

Corporate-debt net issuance surged once spreads began tightening.2 Net issuance measures the change in the outstanding supply of corporate-bond debt.3 As a result of this increase in issuance, the outstanding supply of U.S. investment-grade (IG) corporate bonds increased by approximately 10% between March 1 and June 26.

Exceptionally Strong Issuance as Spreads Tightened

Corporate-bond spreads were calculated as option-adjusted spreads (OAS, in bps) on the MSCI USD Investment Grade Corporate Bond Index.

This surge in issuance may partly reflect the needs of companies to fund existing operations while facing revenue shortfalls. It may also reflect the desire of corporate treasurers to take advantage of historically low rates. Regardless of the reason, the corporate debt burden grew significantly over the past several months in the face of weaker economic conditions.

Low Yields May Have Contributed to Higher Issuance

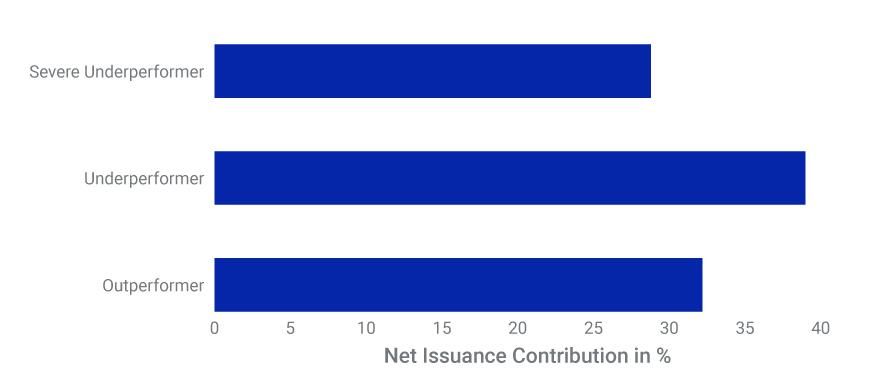

Corporate Borrowers and Equity-Market Performance

To better understand the source of the issuance surge, we analyzed corporate issuers according to their equity-price performance. Based on equity returns between Feb. 19 and June 26, we placed issuers in three categories:

- COVID outperformer: Equity return exceeded return on the MSCI USA Index.

- COVID underperformer: Equity return was below return on the MSCI USA Index but higher than -30%.

- COVID severe underperformer: Equity declined by 30% or more.

Equity-Market Underperformers Drove the Majority of Bond Issuance

Sometimes Words Speak Louder than Actions

Corporate-bond supply surged in March through May, but net issuance in June moderated significantly, as corporate spreads and rates stabilized and moved within narrower bands than in previous months.

Future supply, however, is not the only consideration for investors to weigh. Strong demand for corporate bonds in the face of the supply surge resulted in tighter spreads over the past several months.5 The Federal Reserve's direct purchases contributed relatively little to this demand.6 But over this period, the Fed had been very vocal in expressing its intentions to support the market. The spread tightening that occurred may partly reflect the Fed's credibility among market participants. Sometimes words may mean more than actions, particularly if those words come from the Fed.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1As far back as April 2019, the International Monetary Fund highlighted the potential risk to the corporate sector from a significant economic decline given the growth in corporate-bond leverage. “Global Financial Stability Report.” International Monetary Fund, April 2019.2MSCI’s methodology for net issuance is based on bond-level characteristics from Refinitiv and bond-level ratings from Standard & Poor’s and Moody’s.3Net issuance may differ from gross issuance. Maturing bonds, or bonds called by issuers, may be replaced with newly issued bonds. This may generate gross issuance of bonds while net issuance is unchanged. Such “churning” of existing debt does not reflect an expansion in the outstanding supply of debt.4Not all bond issuers had publicly traded equities. In our analysis, we removed such firms. The share of issuance shown in the exhibit is the share of issuance for firms with publicly traded equities.5Strong demand has partly been driven by purchases from non-U.S. investors: Rennison, J. “US corporate borrowing costs sink to record low.” , June 19, 2020.6The Federal Reserve made the first purchase for its corporate-credit facilities on May 12. It had purchased a total of USD 8.7 billion in corporate bonds and ETFs by June 24. “Factors Affecting Reserve Balances - H.4.1.” Federal Reserve.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.