The Dividend Yield Factor: Defying Conventional Wisdom

Blog post

December 15, 2015

Ever since central banks slashed interest rates in response to the Global Financial Crisis, investors have been searching for yield. As bonds no longer kicked off the desired level of yields, many institutional and retail investors turned to high dividend-paying equities to meet their needs for income.

Historically, the dividend yield factor has delivered a significant risk-adjusted return as a stand-alone risk factor: Over the 88-year period ended July 2015, high dividend-paying stocks have outperformed the market by 1.5% per year. The factor also has produced significant return premium after controlling for traditional factors such as market, size, value and momentum and has performed better in emerging markets, where investors regard stable income as a safe harbor against local economic and currency risks.

However, a naïve high-yielding equity strategy can be vulnerable to various "yield traps," such as those stemming from temporarily high earnings, high payouts or falling stock price. A careful design of the yield strategy is therefore important.

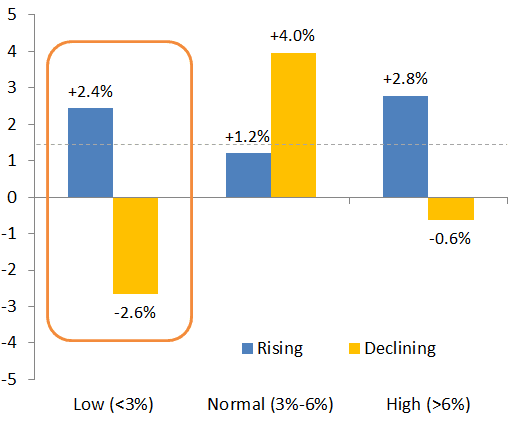

Contrary to the conventional wisdom that investors should hunt for yield in a declining or low interest rate environment, such regimes have historically coincided with low active returns for high dividend-yielding strategies. Rather, we found that the yield factor has tended to perform well during a structurally low and rising interest rate regime, as can be seen in the below exhibit. This could become a prevailing macroeconomic regime over the coming years as the Federal Reserve begins its rate-hiking cycle.

Yield Factor and Interest Rate Regimes

Source: Kenneth R. French Data Library, Robert Shiller

Read the paper, "Harvesting Equity Yield: Understanding Factor Investing."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.