The Roots of Active Managers' Underperformance in March and April

Blog post

July 7, 2014

March and April of this year saw one of the worst periods of active performance over the past 10 years for actively managed portfolios. And this happened, despite a flat stock market and historically low volatility levels.

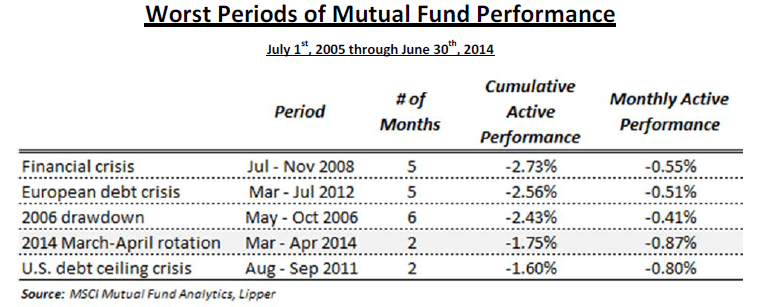

To give you some elements of comparison, by "worst performance" we mean that it is comparable to periods of large economic shocks (see chart 1) such as the financial crisis of 2008 and the European debt crisis of 2012.

Chart 1:

This rightly unnerved investors and prompted us to take a closer look at the root causes of this underperformance. As I recently told the FTfm's Chris Flood, the worst-performing funds tended to have more exposure to more-volatile high-beta stocks, momentum stocks that had done well over the previous 12 months, and growth-orientated equities. To better understand this, we ranked active style exposure of each fund (the 10 funds with the worst performance and the 10 funds with the best performance for these two months) with respect to its peer group and assigned a percentile rank. What we found is that the worst perforating managers fell in the 93d, 89th and 85th percentile in terms of their exposure to growth, beta and momentum, while the best performing managers had heavy exposure to Value, Profitability and Earnings quality. It seems now that sector and style rotation in those two months was driven by uncertainty about the speed of the economic recovery. As we explained in our paper "Market Spin Cycle: Understanding Style and Sector Rotation in a Flat Market" while it is too early to say how long this rotation will last, investors can benefit from managing their portfolio exposures to the most impacted investment styles.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.