The Search for Yield: Leveraged Loans vs. High-Yield Bonds as Interest Rates Rise

Blog post

January 19, 2017

The low interest rate environment continues to send institutional investors on a search for yield. But with the Federal Reserve signaling an increased pace of tightening in 2017, many are reducing interest rate exposure and seeking higher yields in credit instruments.

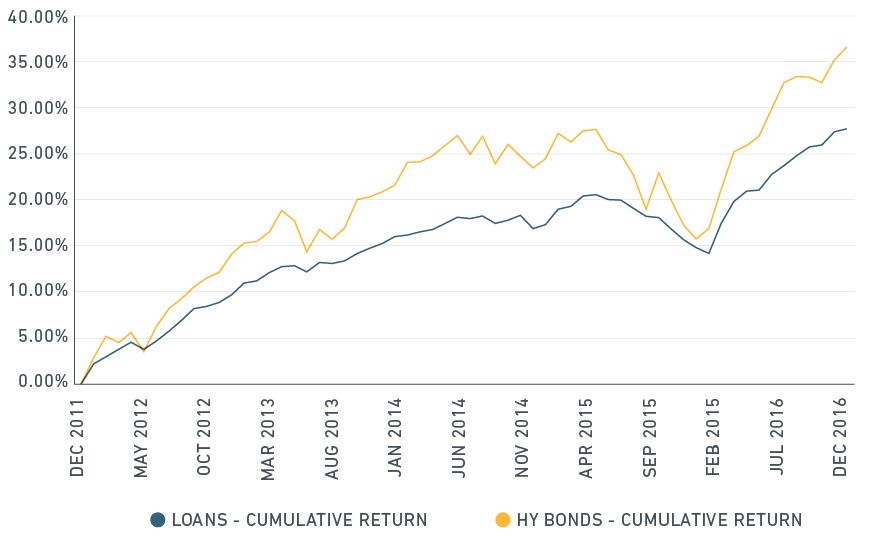

For fixed income investors, leveraged loans (also known as syndicated bank loans) have emerged as an alternative to the typical high-yield bond allocation. As seen in the exhibits below, such loans performed favorably on a risk-adjusted basis over the five years that ended Dec. 31, 2016.

Leveraged Loans and High-Yield Bonds: Performance Over Time

Source: MSCI Research. U.S. high-yield bonds represented by the Markit iBoxx USD Liquid High-Yield Index. U.S. leveraged loans represented by the Markit iBoxx USD Liquid Leveraged Loan Index.

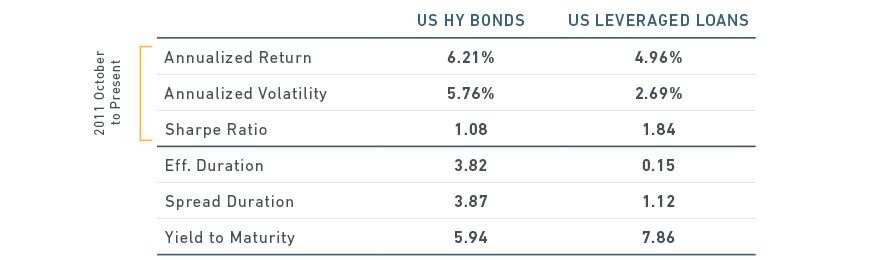

Return and Risk Characteristics for US high-yield bonds and US leveraged loans

Source: MSCI Research. U.S. HY Bonds represented by the Markit iBoxx USD Liquid HY Index, U.S. Leveraged Loans by the Markit iBoxx USD Leveraged Loan Index. All statistics are as of Nov. 30, 2016.

Should rates continue to rise, the comparison could become starker. Comparing risk measures for the Markit iBoxx USD Liquid Leveraged Loan Index and the Markit iBoxx USD Liquid High-Yield Index, MSCI's leveraged loan model suggests that such loans would behave very differently from high-yield bonds in a changing interest-rate environment.

The floating-rate coupons of leveraged loans give them significantly less exposure to rising rates than fixed-rate high-yield bonds. As rising LIBOR rates lift more loans off their coupon floors, the index duration has shortened further. Leveraged loans' seniority and security in the capital structure could provide an extra degree of downside protection compared with high-yield bonds.

Loans carry their own distinctive risks, however, particularly the risk of borrowers calling in their loans prior to maturity. Projected cash flows, and thus sensitivity to credit spreads, depend critically on whether bonds are called, yet many investors use simplistic rules of thumb for estimating average loan lives.

MSCI's leveraged loan model draws on more than a decade of loan performance data to calibrate loan-specific prepayment forecasts. With average loan prices approaching par and the likelihood of issuers calling their bonds relatively high, the model indicates spread durations are considerably lower for loans than for high-yield bonds, as seen in the exhibit below.

Still, if spreads widen, the model suggests the impact would be twofold. Widening spreads tend to be accompanied by increased spread volatility, and reduced calls would extend cash flows further into the future, increasing spread durations. That would leave investors facing heightened exposure to a larger source of risk.

The author thanks Andrew DeMond and Hamed Faquiryan for their contributions to this post.

Further reading:

Analyzing Credit Strategies from a Risk and Return Perspective

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.