The value of standards in the investment process

Blog post

December 2, 2019

- As the investment process continues to evolve, common standards have become essential tools in helping investors to measure, evaluate and describe their portfolios.

- In addition to describing risk and return characteristics, standards for sector and factor analysis may provide additional insights and transparency into the investment process.

- Standards need to evolve over time to reflect the dynamic investment landscape.

Part I: The value of a standard as an objective measure

Perhaps one of the most important standards used in the investment process is the benchmark index, which can serve as a dispassionate arbiter of performance evaluation. However, benchmark misfit or lack of alignment between an active manager and a reference index can lead to unintended consequences.

Using the MSCI ACWI Index and the MSCI ACWI Small Cap Index as benchmarks versus a composite of actively managed global small-cap funds (the "global small-cap composite"), we can see the inconsistencies that may arise from benchmark misalignment.1

Consistent, but inconclusive active return vs. potential benchmarks

Data for periods ended September 2019

As we examined which index may be better suited as a benchmark for the fund, we see that lack of directional consistency in returns over different measurement periods rendered the results inconclusive in terms of benchmark selection.

For further analysis, we looked at the rolling 24-month tracking error between the global small-cap composite and the MSCI ACWI Index and MSCI ACWI Small Cap Indexes. Over this period, the global small-cap composite consistently had a lower tracking error versus the MSCI ACWI Small Cap Index compared to the MSCI ACWI Index.

Rolling 24-month tracking error: The global small-cap composite vs. two MSCI indexes

Tracking error over this period implies that performance of the global small-cap composite was more closely aligned with the MSCI ACWI Small Cap Index than the MSCI ACWI Index

Part II: Standards provide transparency and comparability

When analyzing portfolios, investors rely on a myriad of descriptive data such as country assignment, currency and sector exposures as well as industry classification. In addition, investors use stock-level data to measure exposure to style factors, such as value, size and momentum. Measuring exposure to style factors may help explain a portfolio's risk and return.

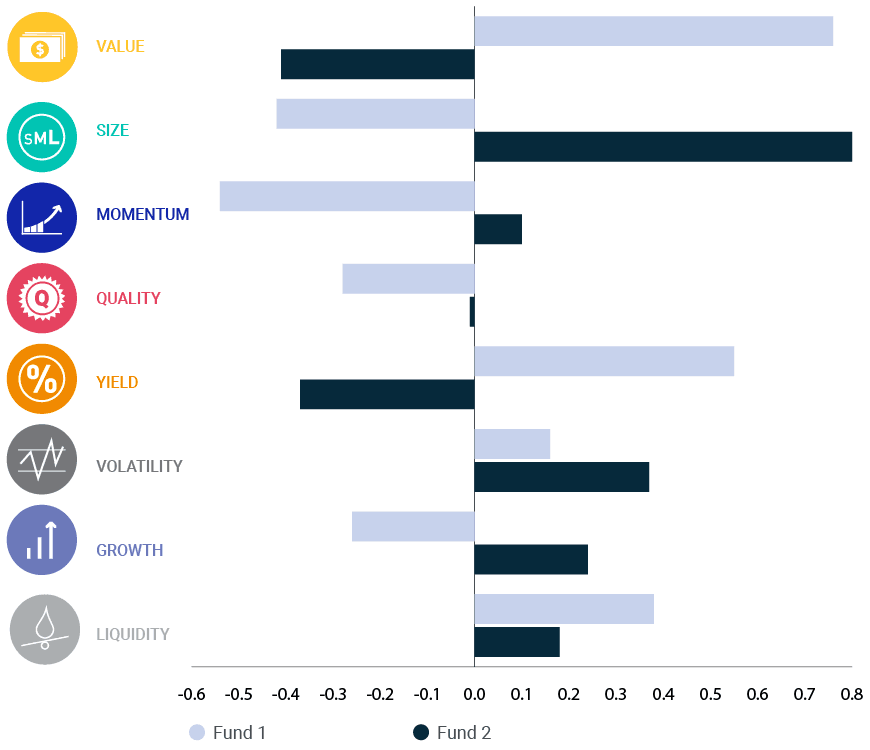

Here we use the factor classification standard, MSCI FaCSTM to compare to what extent the factor exposures for two international value funds were consistent with their fund name strategies.2

Active exposures for two international value funds vs. the MSCI EAFE Index

Active factor exposures as of Sept. 30, 2019

While both funds included "Value" in their name, only Fund 1 had a positive value exposure, as of the end of September 2019. Fund 2 had a growth exposure of +0.24; clearly inconsistent with a value-oriented strategy.

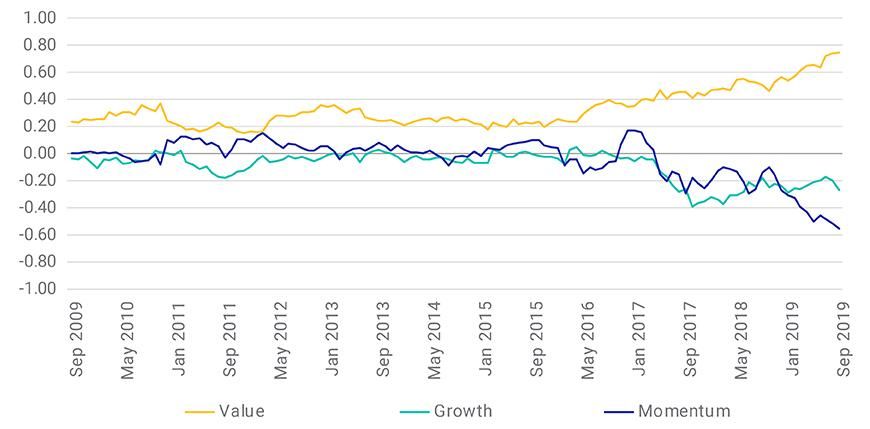

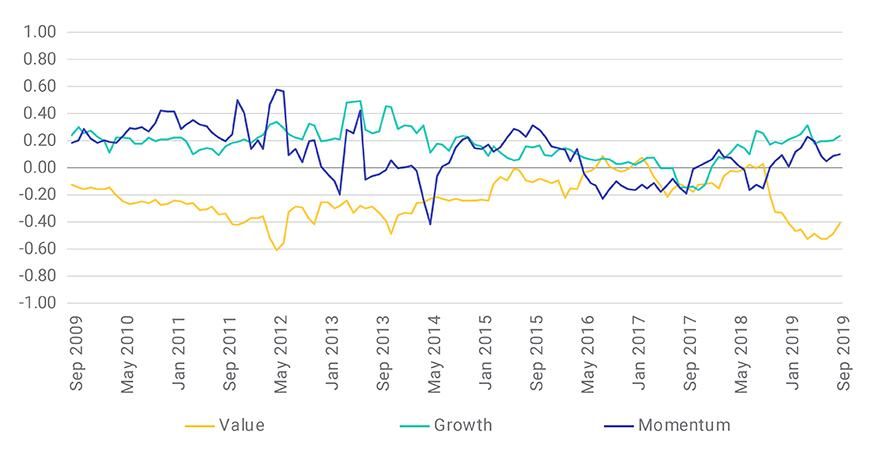

However, given the variability of factor exposures across time due to rebalances or the potential impact from shifts in the market environment, we examined the active factor exposures for each fund monthly from September 2009 to September 2019.

Active factor exposures for two "value" funds vs. the MSCI World Index

Data from September 2009 to September 2019

As we looked across the 10-year period, we see that Fund 1 maintained a consistent positive value exposure over time. While Fund 1 has had low average exposure to growth and momentum, we see that over the past two years, exposure to both factors has trended lower, implying that the stocks held by Fund 1 had lower growth and momentum exposure than those in the MSCI EAFE Index. Conversely, the value exposure for Fund 2 peaked in August 2016 (at +0.09). In addition, the growth and momentum exposures for Fund 2 are positive as of September 2019, at +0.24 and +0.10 respectively.

Based on this analysis, it appears that Fund 1 maintained a consistent value-oriented strategy while Fund 2 may have either drifted from value or changed strategies. Relying on a standard to compare factor exposures for each fund provided greater transparency and established a consistent basis for comparison across time.

Part III: Standards capture the evolving nature of the investment process

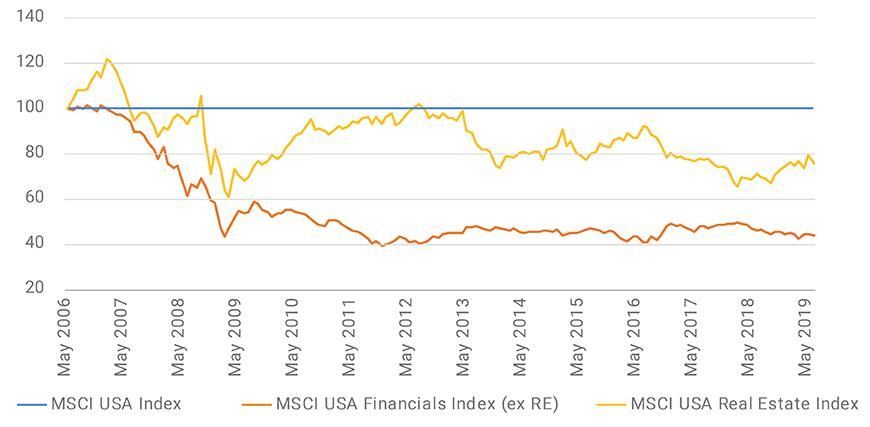

Since its development in 1999, the Global Industry Classification (GICS®)3 has become widely accepted as an industry analytical framework for investment research, portfolio management and asset allocation.

However, just as the investing landscape continues to evolve, so too must standards if they are to continue to accurately play their role. For this reason, GICS introduced real estate as an 11th sector in August 2016, separating it from the financials sector to reflect the fundamental difference between real estate and financial companies. Investors globally were speaking a different language when it came to these two types of companies. The GICS standard had to change to reflect that.

While real estate was not separated from financials until 2016, we can examine this change by looking at the hypothetical return relative to the MSCI USA Index. From May 2006 through June 2019, the MSCI USA Financials Index, ex real estate returned 2.3% versus the MSCI USA Index, compared to 6.9% relative return for the MSCI USA Real Estate Index.

Splitting the financial sector produced two distinct sets of returns

Unnamed: 0 | USA Financials (ex Real Estate) Index | USA Real Estate Index |

|---|---|---|

Unnamed: 0 Total return (%) | USA Financials (ex Real Estate) Index 2.3 | USA Real Estate Index 6.9 |

Unnamed: 0 Total risk (%) | USA Financials (ex Real Estate) Index 22.8 | USA Real Estate Index 24.1 |

Unnamed: 0 Price-to-book | USA Financials (ex Real Estate) Index 1.2 | USA Real Estate Index 2.6 |

Unnamed: 0 Dividend yield (%) | USA Financials (ex Real Estate) Index 2.1 | USA Real Estate Index 3.6 |

Period: May 31, 2006 to June 28, 2019

Evolving the GICS standard by separating financials and real estate into two sectors not only resulted in different historical returns but may provide potential opportunities for investors as they analyze these two distinct groups of companies.

Maintaining standards

Standards used across the investment process establish a common language to foster communication and provide clarity among market participants. We examined three standards — benchmark indexes, a factor classification system and a sector and industry framework — which can help evaluate manager returns, quantify factor exposures and measure the impact of changes in sector and industry trends. Ongoing consultation with market participants is critical in maintaining the vital role standards play in today's investment world. Whether these standards endure is premised largely on their ability to evolve and adapt in rapidly changing markets.

The author thanks Raina Oberoi for contributing to this blog.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The global small-cap composite consists of the top 5 largest mutual funds by AUM in the global small cap category for which ten years of returns and holdings are available2The funds used in the analysis are the two largest mutual funds by AUM in the international value fund category for which ten years of returns and holdings are available3GICS, the global industry classification standard jointly developed by MSCI and Standard & Poor’s. Please refer to Global Industry Classification Standard (GICS®)

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.