There is More Than Equity in Private Equity

Blog post

June 29, 2015

Private equity is both "private" and "equity." The valuations look smooth from quarter to quarter, but in the long run, private equity shows a strong relationship with equity and is exposed to many of the same systematic factors that drive traditional assets.

But "equity" is not the full story. There is also a strong "private" component. A key question for investors is how much is private equity driven by each component. Is the strong historic performance of private equity due to skill or a liquidity premium? Or is the performance just driven by leverage and a plain-vanilla risk premium? Is an investment in private equity a diversifying "alternative" or a risky bet on systematic risks hidden by a lack of transparency?

There are substantial differences between public and private equity. Some of the difference is due to the nature of private markets: Returns of investments made in vintage years with large capital commitments tend to suffer in the long run, for example, perhaps driven by higher prices and lower quality investment opportunities. And some of the difference is simply due to a mismatch of the constituents of public and private markets: Even a micro-cap stock can look like a mature blue chip compared to early stage ventures.

Therefore, the private component of private equity is substantial, and cannot be proxied by public investments. Understanding the true nature of private equity helps institutional investors determine how the asset class fits into their overall portfolios. If the "private" component is large, then private equity may be a compelling choice for long-horizon investors who can tolerate a lack of liquidity.

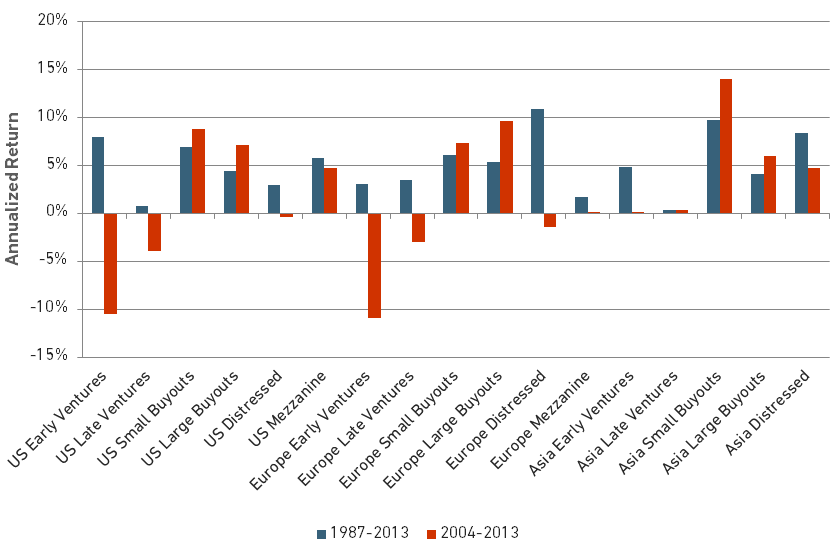

The Barra Private Equity Model (PEQ2) helps shed light on these questions with new estimates of private equity betas and "pure private" factors. New methodology sees past the smoothness of private equity valuations and reveals much higher betas. Nonetheless, many segments of private equity have significantly outperformed the market even on a risk-adjusted basis, as shown in the figure below.

Of course, "past performance is no guarantee…"

Historical Private equity alpha

Source: MSCI Barra Private Equity Model (PEQ2). Data from The Burgiss Group, LLC and Private iQ®. Private iQ® is a registered trademark of The Burgiss Group, LLC.

Net of the higher betas (and net of fees), most segments of private equity have significantly outperformed the market over the long run, although ventures have underperformed in the more recent period.

Read the paper, "Model Insight - The Barra Private Equity Model (PEQ2)."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.