Tilting to U.S. Small Caps: Using MSCI Analytics in Portfolio Construction

Blog post

May 15, 2015

U.S. cap-weighted, small-cap benchmarks have historically displayed structural biases that affect performance. For example, small-cap indexes have sector, revenue and style tilts compared to the broad U.S. market. U.S. small caps are more concentrated in financials and industrials, while their revenue exposure is more domestically oriented than the broad market.

Despite showing outperformance versus their large- and mid-cap peers over the whole period, U.S. small-cap companies were also less profitable and had lower quality earnings than the broad market. Both of these tilts negatively affected returns during the period from February 1997 to December 2014.

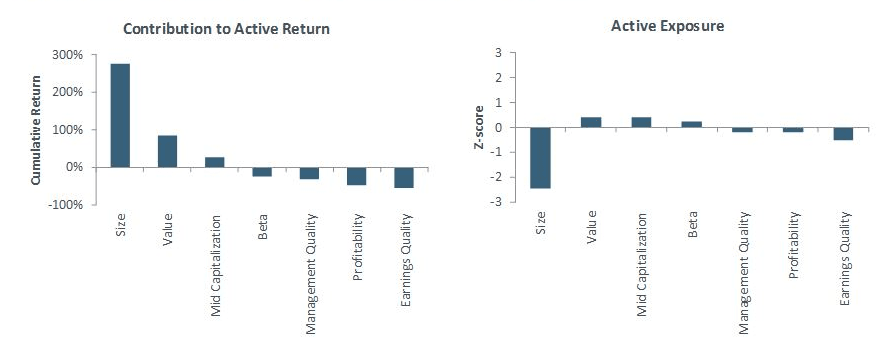

Sources of Active Return on MSCI USA Small Cap vs. MSCI USA

Data from February 1997 to December 2014

Managers can hedge or avoid these unwanted exposures and this would have historically improved performance of their small-cap portfolios: Using the Barra US Small Cap Model, we find that an Enhanced Small Cap simulated strategy outperformed the MSCI Small Cap benchmark on a risk-adjusted basis by increasing exposure to the Earnings Quality and Profitability factors. By using equity risk models tailored to the investment universe, active managers can hedge out or avoid unwanted exposures, conserving their risk budgets for asset selection. Alternatively, managers could employ a portfolio replicating an index that seeks to tilt toward high quality small-cap companies, such as the MSCI USA Small Cap Diversified Multi-factor Index. Read the paper, "Tilting to U.S. Small Caps."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.