U.S. Real yields: Opportunities and Warning Signs

Blog post

December 12, 2018

Despite the recent rally in the U.S. government bond market, real U.S. bond yields (i.e., nominal yield minus the market-implied rate of inflation) still remain substantially higher than at the beginning of the year. This may be both a blessing and a curse for investors. While today's higher yields still present one of the best opportunities to lock in real returns since 2010-2011, we found that this year's rise may partly reflect a reduction in the supply of savings coming into the U.S. from abroad. If true, the continuation of this trend could hurt returns for bonds and equities.

Trends in real yields

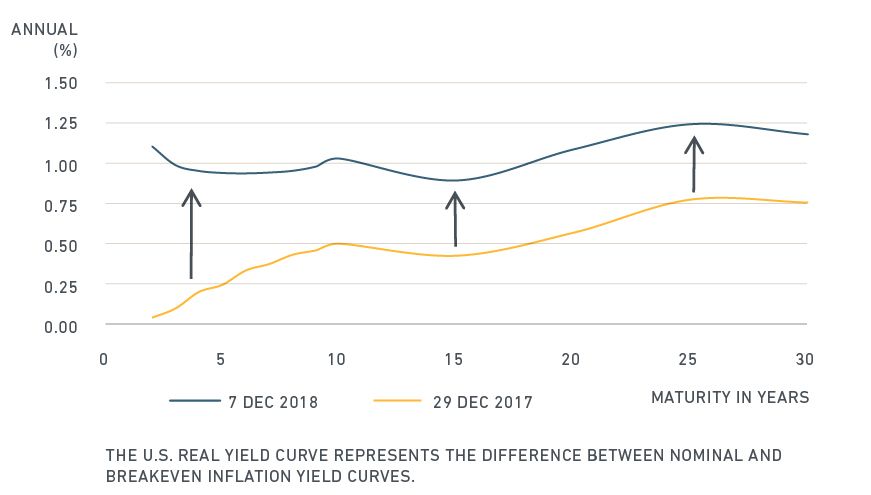

In 2018, yields have risen across the yield curve, with 2-year real yields up 107 basis points (bps) through Dec. 7 and 10-year real yields up 53 bps.

U.S. real yields have risen this year

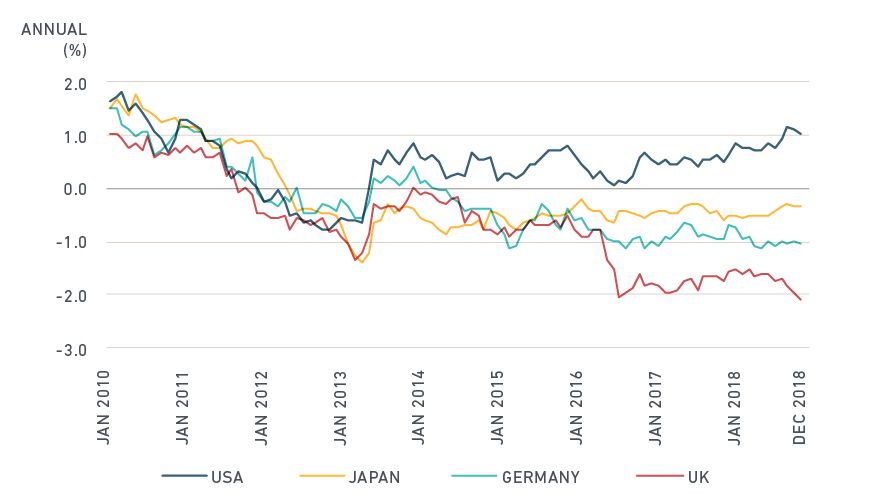

In addition, the exhibit below shows that the de-coupling of yields between the U.S. and other major countries has accelerated this year, with U.S. real yields now substantially higher than those available in other developed markets. These shifts are important in and of themselves for asset allocators, but it may be worth considering the subtext and examining the underlying drivers.

U.S. 10-year real yields higher than other developed markets

What's the real story? Demand or supply?

The corporate demand for investment capital and the supply of savings are fundamental drivers of real interest rates. An increase in demand for capital may reflect improved technology, lower corporate taxes or expectations of a stronger economy, and may be expected to push up both real rates and stock prices.

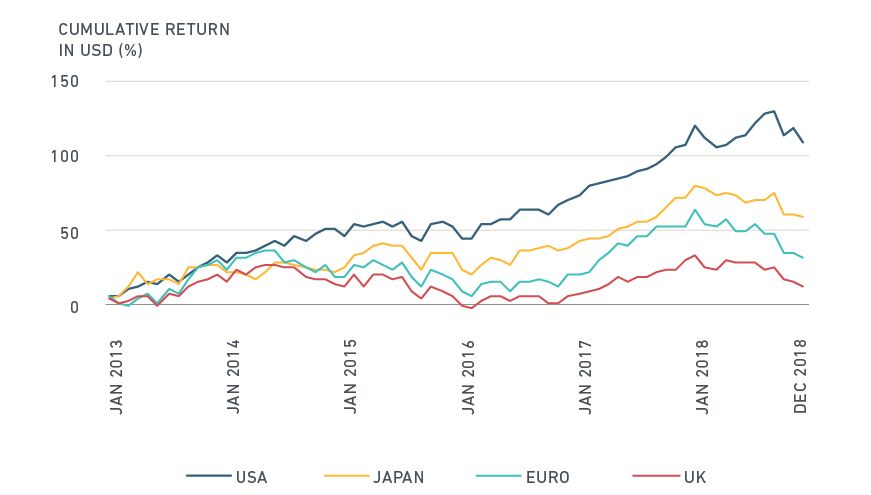

Over the past six years, equity performance in major developed markets has generally aligned with differences in real rates, with high real yield countries, such as the U.S., generating relatively strong returns while low real yield countries, such as the U.K., produced much lower equity returns (see exhibit below). This is consistent with strong investment demand in the U.S. resulting from improved investment opportunities.

Equity market performance has aligned with real rates

However, the flat performance of the U.S. equity market in 2018 (.2% as of Dec. 7) despite strong gross domestic product (GDP) growth and corporate tax cuts suggests that forces other than investment demand may have also played a role in driving real yields higher.

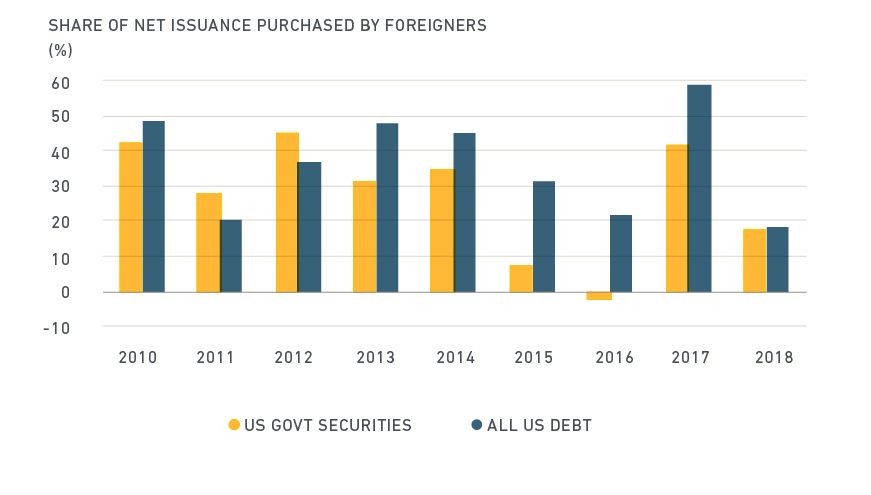

So, what about supply factors? Everything else being constant, a contraction in the supply of savings – of which savings from abroad is an important source – may result in higher rates and lower valuations for both U.S. bonds and equities. Between 2010 and 2017, foreign net purchases of U.S. bonds averaged 39% of net bond issuance, (i.e., the amount of new bonds issued minus bond redemptions). This year, the share of net foreign purchases of all net U.S. debt issuance fell to 19% through the end of the second quarter. This relative reduction in foreign capital coming into the U.S. market may reflect several distinct factors, including foreign exchange reserve management by central banks and expected returns on U.S. versus non-U.S. assets.1 Regardless, it appears that this supply reduction may have played a role in driving U.S. real yields higher.

Foreign savings supply has fallen this year

*Source: U.S. Federal Reserve

Implications for investors

For investors bullish or neutral on real yields, U.S. Treasury Inflation-Protected Securities (TIPS) offer the most direct way to lock in higher real returns resulting from the rise in yields since the beginning of the year. Nominal bonds may also offer higher real returns as long as inflation does not rise above levels currently reflected in market-implied breakeven inflation (currently ranging from 1.6% for 2-year maturities to 2.0% for 20-year maturities), and, for corporate bonds, credit spreads do not widen.

However, real yields could continue rising. For investors concerned about this possibility, the short end of the curve may offer a relatively safe harbor. This is because its shorter duration leaves it less exposed to the potential for further increases in real U.S. bond yields.

The author thanks Aniko Maraz for her contribution to this post

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 U.S. Treasury Department data through August show foreign official holdings of long-term U.S. debt have fallen this year relative to private foreign holdings within each debt category (Treasurys, agencies, corporates).

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.