US inflation: The market’s implied view

Blog post

April 21, 2020

- Some investors worry that aggressive monetary policy, fiscal stimulus and rising levels of public debt will lead to high inflation in the long run.

- Breakeven-inflation (BEI) curves can be used to gain insight into market-implied inflation expectations.

- Current market-implied expectations, based on MSCI's methodology for BEI curves, point to downward pressure on prices in the near future and do not indicate abnormally high inflation over the longer term.

Inflation or deflation?

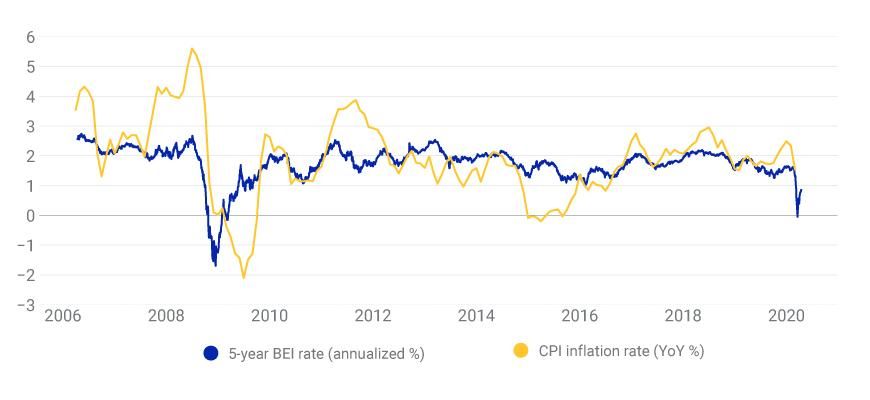

Over the past year, inflation — as measured by the consumer-price index (CPI)2 — averaged 1.5%. In contrast, the one-month inflation rate between February and March of this year was -.4%. And the one-year market-implied inflation expectation was -.8%, as of April 14, highlighting the distinct possibility of deflation over the next year. The five-year market-implied expectation is now .8% on an annualized basis.

Deflationary pressures may be partly attributed to the coronavirus-induced slowdown in economic activity and plunging prices of commodities, with the price of crude oil down by approximately 50% year over year.3 By way of comparison, during the 2008 global financial crisis (GFC), the price of crude oil declined by more than 60%, and the realized year-over-year CPI inflation rate was negative for eight months in a row.4

Breakeven inflation pointed to lower reported inflation

Sources: U.S. Bureau of Labor Statistics, MSCI

Concern about long-term inflation risks

Since the coronavirus outbreak, the Federal Reserve has moved aggressively to calm markets and stabilize the financial system. The Fed's balance sheet increased by 41%, or almost USD 1.8 trillion, between March 9 and April 8.5 The fiscal response has also been of historic proportions, with recently enacted legislation providing significant new federal spending, in response to the pandemic crisis.6

Some investors are now concerned that aggressive monetary policy, fiscal stimulus and rising public debt levels may lead to high inflation in the long run.7

What does market-implied inflation tell us?

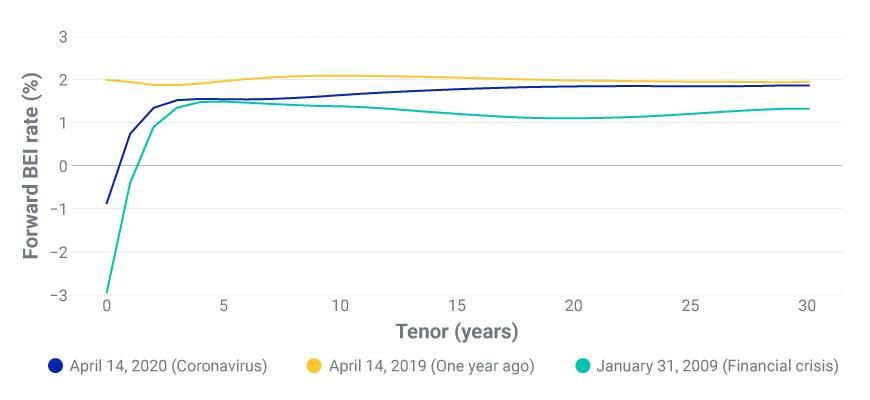

The one-year forward BEI curve can be used as a measure of market-implied year-over-year inflation expectations.8 Using this measure, we find that current market valuations suggest deflation only for the next year — and low positive inflation afterward for an extended period of time. One-year implied inflation 10 years in the future is approximately 1.5%, below the Fed's 2% target and the average inflation rate of 1.7% prevailing since the GFC.

Market-implied inflation below Fed's 2% target

Calculated using MSCI BEI curves.

Is talk of inflation just a lot of hot air?

In a time of great economic uncertainty, market participants are trying to distinguish the true inflation signal from the inflation noise that we may see in coming months.

Our analysis based on MSCI BEI curves indicates that U.S. Treasury market-implied inflation expectations have increased over the past several weeks, during a period characterized by massive monetary and fiscal stimulus, but market-implied inflation expectations for the next 10 years still average only 1.2% annually. While monetary and fiscal stimulus may trigger future rises in prices, current market-implied measures of inflation suggest future rates of inflation that are modest by historical measures.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Breakeven-inflation curves are calibrated using prices on U.S. nominal Treasurys and U.S. Treasury inflation-protected securities.2The month-over-month measure is seasonally adjusted, while the year-over-year measure is not. “Consumer Price Index for All Urban Consumers: All Items in U.S. City Average.” U.S. Bureau of Labor Statistics.3The year-over-year change was calculated as of April 14, 2020, using the three-month tenor of the MSCI Light Sweet Crude Oil curve.4From April 2009 through October 2009.5"Recent balance sheet trends.” Federal Reserve Board.6For estimates of the increase in federal spending and fiscal deficits, see: “New Projections: Debt Will Exceed the Size of the Economy This Year.” Committee for a Responsible Federal Budget, April 13, 2020.7Mackintosh, J. “After Coronavirus, We Will Have to Reckon With the Debt.” , March 29, 2020.8The one-year forward curve shows the evolution over time of one-year BEI rates. For example, the forward curve at the 10-year tenor may be interpreted as the market-implied one-year expected inflation rate 10 years from now.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.