Using Risk Analytics to Highlight Opportunities in Volatile Markets

Blog post

May 18, 2020

- Many MSCI clients have integrated risk across their investment process, from compliance to trading and strategy development.

- The role of risk for compliance is typically defensive, while for trading and strategy development, it may be used to more flexibly navigate a crisis and capture additional opportunities.

- Risk takes different forms across different markets and opportunities, and can be put in a common context using a detailed and flexible quantitative risk framework.

Combining Risk with Trading Decisions

By measuring risk at the right level of detail, and combining risk with trading decisions, portfolio managers may identify new opportunities for alpha generation. Take, for example, a credit strategy: Volatile markets create greater differentiation in the market price of credit risk across issuers, potentially increasing opportunities to make bets on individual issuers. In this situation, risk can provide a framework for opportunistic alpha capture.

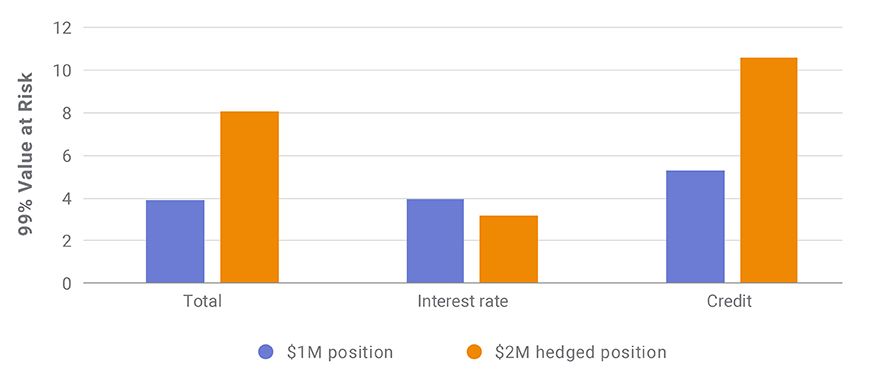

Consider a hypothetical situation where a benchmarked portfolio needs to closely match the benchmark's interest-rate risk. A portfolio manager may want to take on additional exposure to an issuer's credit. For example, in following the benchmark the hypothetical portfolio may have USD 1 million of exposure to an issuer; but to take an active view, the manager would need to buy an additional USD 1 million in that issuer's bonds. A quantitative risk framework in this example may help the manager identify a hedged trade — buying USD 1 million of the issuer's bonds, while taking a short position in bond futures to offset the additional interest-rate risk. The portfolio manager is thereby in a position to take on twice the exposure to the issuer, while staying aligned to the benchmark's interest-rate exposure. The exhibit below shows how we used a quantitative risk framework to analyze the risk of such a hypothetical trade.

Different but Equal Rate Risk — and Varying Potential Alphas

The hypothetical portfolio consists of bonds issued by a large corporate issuer and Treasury futures, each with a 4.5% coupon and 15 years to maturity. The value-at-risk (VaR) measure is computed using a one-year lookback and daily returns. Analysis date is May 1, 2020.

Taking a Firmwide View on Risk Allocation

The traditional segregation of trading desks can obscure firmwide bets that span multiple markets. A detailed, firmwide risk framework can put these bets in a common context — and enable conscious risk allocation at the firm level.

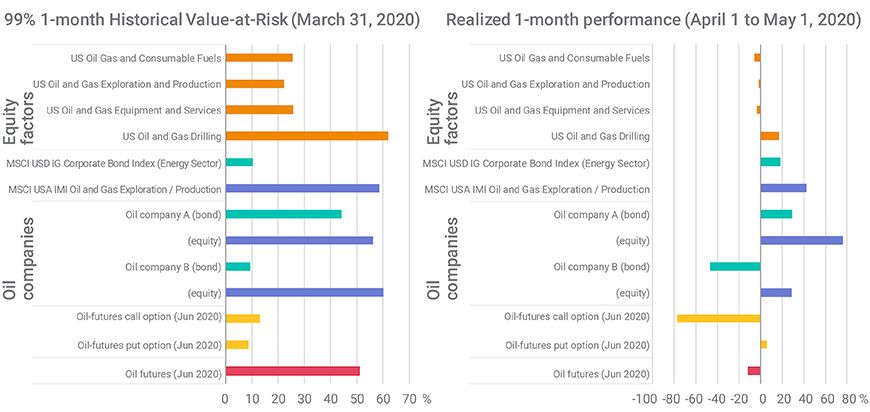

For example, consider the recent dislocation in the oil market. Some investors may take a view on oil through multiple markets: oil futures; options on oil futures; oil companies' debt, credit-default swaps, preferred shares, equity and equity options; oil-equity factor replication; etc. A robust risk framework can help an investor evaluate these possible investment opportunities using a consistent risk methodology, allowing them to highlight trading opportunities and draw on a framework for expressing a risk-weighted directional view.

The exhibit below shows how a wide range of oil-related investments can be analyzed in a common risk context, along with the realized performance of those investments. Note that the illustrated performance over this period is not indicative of future performance, but simply a hypothetical example of how performance can be considered in the context of a uniform risk framework.1

Examining Oil Investments Through a Uniform Multi-Asset-Class Risk Framework

Bonds represent hypothetical 5-year zero-coupon bonds with fully hedged interest-rate risk. VaR for futures and futures options are expressed as a percentage of the futures price. Oil companies are selected constituents of the MSCI USA IMI / Oil and Gas Exploration and Production Index.

Risk in Practice to Navigate a Crisis

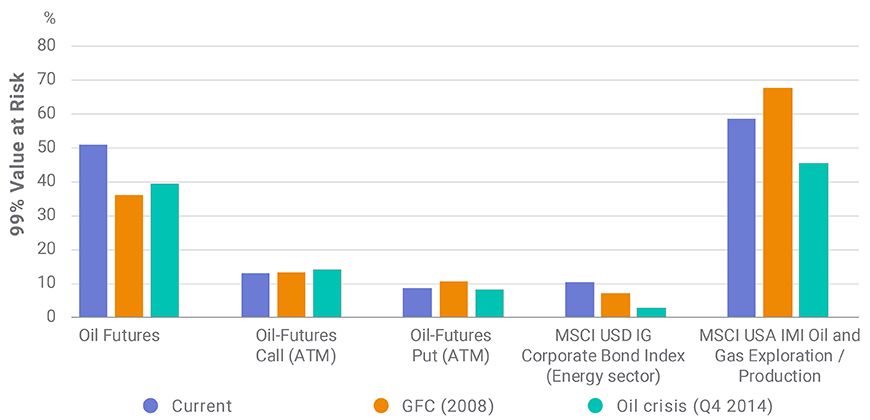

The successful deployment of a risk framework is typically an active, dynamic and multifaceted effort. In addition to looking at the most recent period to build risk forecasts, risk may be managed against many historical and hypothetical scenarios. We analyzed risk in the COVID-19 environment using historical data from the 2008 global financial crisis (GFC), the oil crash of 2014 or combinations of those periods as a reference. Investors may consider historical crises in analyzing risk during more recent events such as the COVID-19 downturn.

Managing Risk Against Historical Lookback Periods for Additional Insight

The current risk estimate uses trailing-return data for the year preceding the analysis date. The estimate for the GFC replays the risk-factor returns during 2008, while the oil-crash estimate replays risk-factor returns during the fourth quarter of 2014.

Risk analytics can be integrated in many parts of the investment process, including trading and strategy development, and provide a consistent quantitative framework for decision-making that may be especially important in times of crisis.

The author would like to thank Ajinder Banns for his contribution to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Another important dimension is liquidity; although oil futures have the largest VaR, they are relatively liquid instruments, with a bid-ask spread of 29 basis points (measured with respect to the underlying futures price). In contrast, the most liquid oil-company bond has a relative price bid-ask spread of 113 basis points. These bid-ask spreads are estimates as of May 1, 2020, from MSCI’s RiskMetrics® LiquidityMetrics®.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.