As factor investing becomes increasingly "business as usual," institutional investors have become keenly interested in the ability of strategies that replicate factor indexes to persistently capture the desired exposures. Such investors may wish to gauge how much capital can be invested in funds that replicate factor indexes before their return expectations diminish so that the range of competing investments seem more attractive.

In our recent paper1 published in The Journal of Index Investing, we looked at this issue from a practical perspective and highlighted six different ways that factor indexes can be better designed to handle this challenge. We looked at the tradeoff between investment capacity and factor exposure. We showed that, with care, by drawing on the six approaches in the exhibit below, the capacity of a factor index strategy could have been improved without significantly compromising exposure to the target factor.

To be clear, not all these methods can or should be applied in a single index. Different investors may find different approaches better suited to their needs, and thus may want to explore a selection. For the MSCI Factor Indexes, whether constructed using optimization — such as the MSCI Minimum Volatility and the MSCI Diversified Multiple-Factor (DMF) Indexes — or not, the consideration of the first three, most central approaches are also at the core of the index design process.

Existing approaches used to measure investment capacity that rely on forecasting the expected return of the strategy may be vulnerable to error. Instead, we use the exposure characteristics of factor indexes directly to gauge the capacity pressure that factor index strategies may be feeling.

Market-cap indexes tended to have the highest capacity and lowest turnover because a fund tracking such an index typically owned the same percentage of each company as the index and they tended to have the lowest turnover. For factor indexes, the idea is to achieve the highest level of factor exposure while not taking unnecessary or concentrated positions versus the parent market-cap index. One measure of closeness is the relative weights of individual stocks and level of turnover, as then we can gauge the capacity of factor indexes with reference to their market-cap counterparts.

Six approaches to manage the investment footprint of factor indexes

One possible approach to manage capacity is to constrain the weight of any individual stock to be within a narrow range of its weight in the parent index. We do this in non-optimized factor indexes such as the MSCI Enhanced Value, Quality and Momentum Indexes by starting from the market-cap index and allowing a strictly limited degree of tilt based on each stock's factor score. We have more direct control with the MSCI Minimum Volatility and the MSCI DMF Indexes. For example, in the MSCI DMF Indexes, the maximum weight of each stock is limited to be the minimum of (the parent index weight + 2% and parent index weight x 10).

Limiting regular turnover to levels where nevertheless we can still achieve enough of the desired factor exposure when we rebalance the index is another natural way to seek to improve capacity and is a standard part of all MSCI Factor Indexes. Again, for the MSCI Minimum Volatility Index and the MSCI DMF Indexes, this control can be enforced explicitly in the optimization, rather than be achieved indirectly by selection buffers.

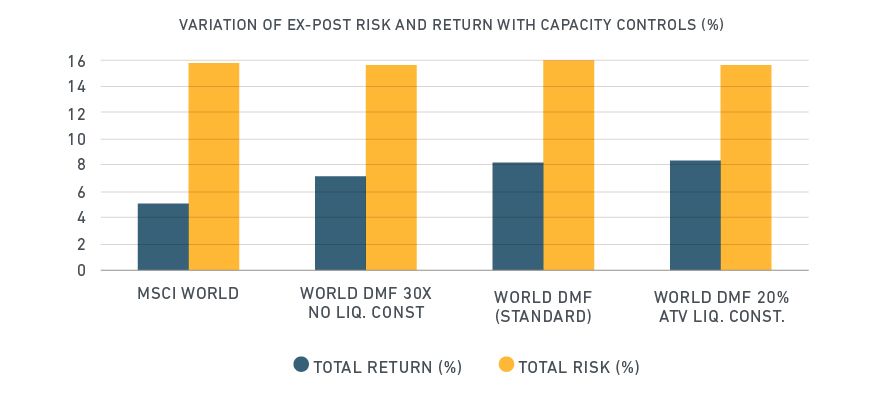

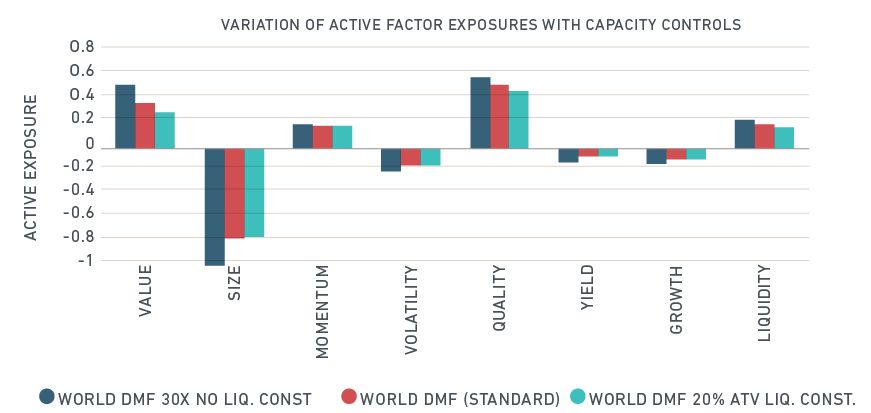

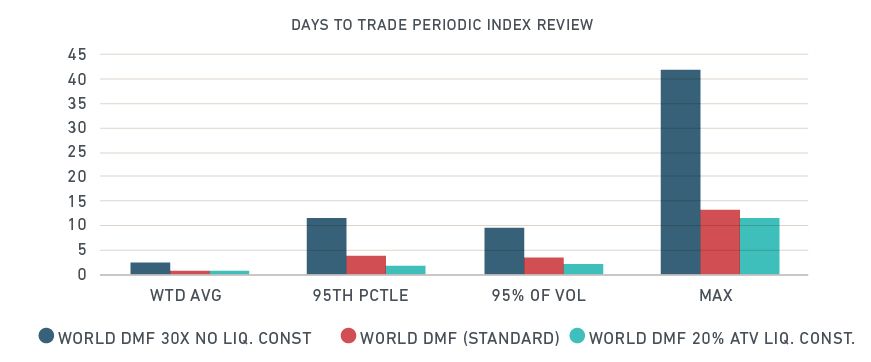

In the exhibit below, we illustrate the first two approaches — constraining the weight and limiting turnover — using the example of the MSCI DMF Index which targets exposures to the value, momentum, quality and size factors.

Variation of realized risk, return, factor exposure and days to trade with capacity/liquidity control2

In the third approach, the annual turnover budget is kept fixed, but the rebalance frequency is increased. This spreading of turnover more widely over time aims to reduce market impact and event risk but may lead to reverse turnover ("flip-flops") for slower moving factors like value and quality. Considering the liquidity of individual constituent adds and deletes during the proposed index rebalances is another layer of control that may also help (option 4). Adds and deletes during each rebalance can be limited to those with sufficient liquidity in the underlying stock (the impact is also shown in the exhibit above). There is typically a tradeoff between achieving higher capacity and the amount of factor exposure that may be achieved. But our research has shown that this tradeoff has not been linear and considerable improvement in capacity was achieved without compromising the factor exposures. Moreover, we find that the historic risk and return characteristics of the MSCI Factor Indexes were robust to these tests, reflecting the capacity considerations built into the index design, and were not a fiction generated from illiquid stocks.

Staggered rebalancing (option 5) is a further way to spread turnover over more rebalance days. It is similar in effect to increasing the rebalance frequency (option 3). To execute, we can set up multiple calendar-offset indexes with otherwise the same index methodology. For example, if we allocate 50% of the total market cap of the index to each offset index, only half of the index is rebalanced at each quarterly rebalance. Staggered rebalances can also be applied to indexes that are rebalanced monthly or away from the regular quarterly cycle.

Spread rebalancing is the final approach we analyzed. For this, we do not change the rebalance frequency, but instead a portfolio replicating the index would spread the "trades" needed to replicate each rebalance over several days rather than a single day (effective date). Of course, this "trade-scheduling" approach is one already used by active factor managers and those running factor index portfolios to reduce market footprint.

Capacity is an important and practical topic for factor investors. Using the MSCI Factor Indexes as examples, we illustrate approaches that can be used in index design to balance high exposure to the target factors with a high level of investment capacity.

1 Alighanbari, M. and S. Doole. (2018). "The Capacity of Factor Index Strategies: Assessment and Control." The Journal of Index Investing. Vol. 9, No. 2, pp. 34-52.

2 In the standard DMF index, the maximum benchmark multiple allowed at rebalance is 20x. Here we look at what happens when this is relaxed to 30x. Conversely, we review the impact of a trade size liquidity constraint that we can only rebalance up to 20% of ATV for any stock.

The author thanks Mehdi Alighanbari for his contributions to this post.