What if Credit Spreads Widen?

Blog post

August 21, 2018

BBBe careful out there

Despite robust economic growth in the U.S., market conditions — as defined by tight spreads and high valuations — have wary credit investors on the lookout for trouble as the credit cycle matures. One area of scrutiny is BBB-rated credit, which sits in the middle of the rating hierarchy. Should spreads suddenly widen, investors may want to be prepared for a potential wave of BBB credits cascading into the high-yield market.

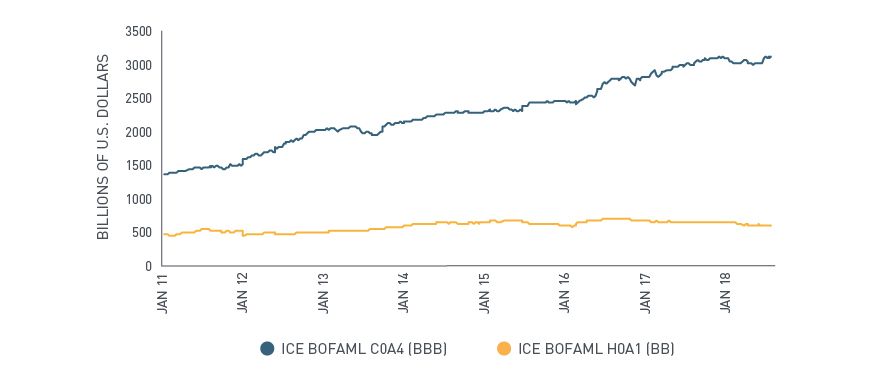

BBBs: A LARGE AND GROWING MARKET

The demand for yield among investment grade (IG) buyers, who are limited to holding assets in the AAA-BBB quality range, has driven the outstanding amount of BBB paper to historic highs (see exhibit below). As of Aug. 10, 2018, the ICE BofAML BBB Corporate Index (C0A4) was roughly six times larger than its BB counterpart, the ICE BofAML BB US High Yield Index (H0A1). However, as illustrated later, the strategy of harvesting yield from nominally IG credit seems to have run its course in terms of risk-adjusted compensation — by some measures the BBB sector looks more like junk quality than IG.

Yield-hungry investors drive BBB-rated US corporate debt to historic highs

Data for the ICE BofAML BBB US Corporate Index (C0A4) and ICE BofAML BB US high-yield Index (H0A1) market values provided by ICE BofAML Global Research, used with permission.

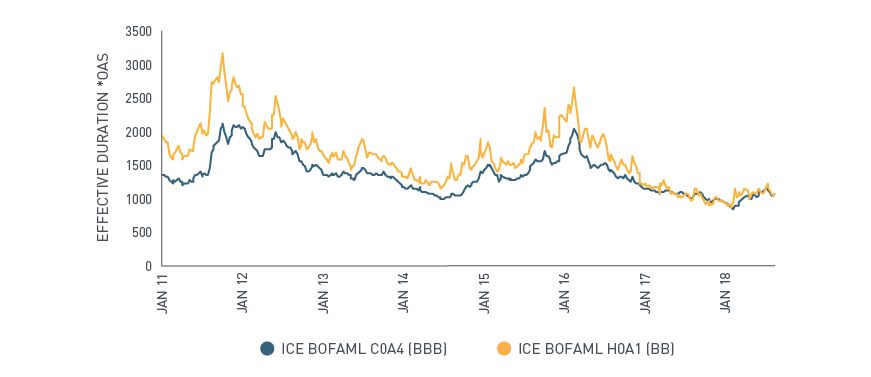

Duration-times-spread (DTS) is a key indicator of forward-looking credit risk used in MSCI's new fixed-income models. DTS, or the product of an asset's sensitivity to spread movements and its market spread, is a strong forecaster of bond price volatility. The DTS riskiness of BBB credit has converged to that of BBs over the past year and a half (see exhibit below). Decomposing DTS into its components indicates that as spreads have compressed across the credit spectrum, duration has extended in investment-grade debt and contracted in high-yield bonds.

BBB credit risk mirrors that of high-yield risk

Data for the ICE BofAML BBB US Corporate Index (C0A4) and ICE BofAML BB US High Yield Index (H0A1) effective durations and option-adjusted spreads provided by ICE BofAML Global Research, used with permission.

EFFECTS OF A DOWNGRADE SCENARIO

The first exhibit also illustrates the potential for an enormous amount of supply to hit the BB market if spreads widen broadly or many investment-grade bonds are downgraded to high-yield territory. MSCI's CreditManager maintains through-the-cycle estimates of probabilities for downgrades; the data show a 4% probability of a BBB credit being downgraded to BB. If such an event were to occur, the composition of the high-yield market could change by roughly 20% on a market-value basis. Hence, in a spread-widening scenario, the whammy could hit investors twice as a sudden rush of supply comes into the high-yield market.

Finally, as we have previously discussed, if high-yield spreads are currently focused on compensating investors for taking duration risk, how will the market react to a rapid extension of duration across all high-yield credit as long-duration1 paper is forced off IG books and fall onto the junk market? There's no time like the present to strategize for seemingly remote scenarios.

1 BBB corporate bonds have on average a duration 2.5 years longer that than of BB bonds.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.