What is Going on With Factor Returns?

Blog post

July 18, 2018

Value and momentum factors typically move in opposite directions — that is, when one outperforms the market, the other usually underperforms. In June, however, both factors underperformed the market, leading several publications1 to question whether this change in market behavior is impairing quantitative strategies.

Based on our analysis, using Factors by MSCI (research, analytics and indexes), we found that performance of the value and momentum factors in June was indeed challenging, but not unusual. The only aspect that was exceptional was the fact that both factors underperformed: Every other month of 2018 showed the two factors moving in opposite directions (indicating negative correlation). Further, we found that a different definition of "value" could lead to conflicting conclusions about that factor's performance.

How unusual was June?

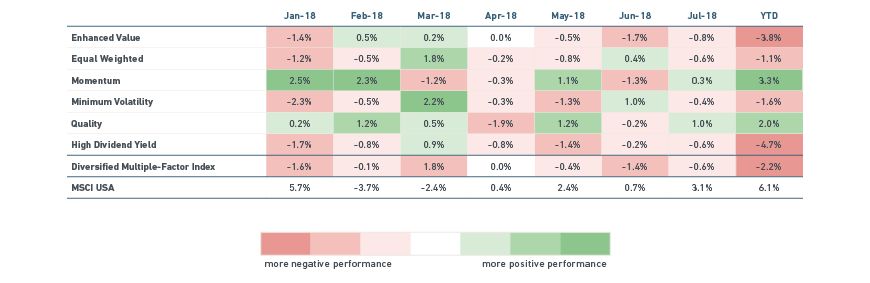

The exhibit below shows the monthly and year-to-date performance for select MSCI factor indexes. Both the MSCI Enhanced Value Index and the MSCI Momentum Index underperformed the capitalization-weighted MSCI USA Index in June, by 1.7% and 1.3%, respectively. However, when compared to their active risk, this underperformance was not unusual on a risk-adjusted-basis (less than one standard deviation). Furthermore, for the first five months this year, plus the first two weeks of July, the two indexes moved in opposite directions, which helps explain the large difference in their performance year-to-date.

Digging deeper, we found that while the MSCI Quality Index and the MSCI High Dividend Yield Index also underperformed the MSCI USA Index in June, the MSCI Equal Weighted Index (reflecting small size) and the MSCI Minimum Volatility Index outperformed by 0.4% and 1.0%, respectively.

Active returns of MSCI U.S. Factor Indexes vs. the MSCI USA Index

July performance is through July 13.

Performance attribution reveals underperformance drivers

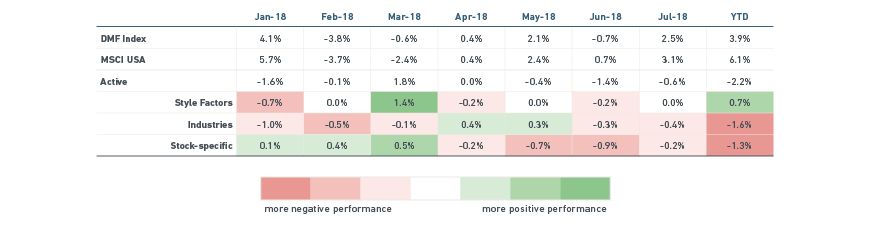

The correlation among factors year to date does not appear exceptional when we consider the performance of the MSCI USA Diversified Multiple-Factor Indexes, which maximize exposure to four factors – value, momentum, quality and low size – while maintaining a risk profile similar to the underlying capitalization-weighted index. The index underperformed in June and year-to-date, but an analysis shows outperformance from style factors year-to-date; in June, style factors impaired performance only slightly. Industry factors were the main detractors year-to-date, driven by an underweight in internet retail and internet software and an overweight in the auto and semiconductor industries. In June, underperformance was driven largely by the stock-specific component of individual stock returns.

Industry and stock-specific risks also contributed to negative performance

July performance is month-to-date through July 13.

It depends on what your definition of "value" is

The last exhibit uses the MSCI U.S. Total Market Equity Model's factors to provide additional insight into the underperformance of the value factor group.2 While the earnings yield factor had a negative return in June (and was the worst-performing factor year to date), the value factor based primarily on book-to-price ratio was positive in June – and for every month except January, as well as year to date.

Different subsets of the value factor group performed differently

Data from the MSCI Barra® US Total Market Equity Model (Long-Term) investors. July performance is through July 13.

Thus, we find that the simultaneous June underperformance of value and momentum was not unusual. Additionally, different definitions of "value" could lead to conflicting conclusions about factor performance. In short, worries about value and momentum moving in the same direction longer term might be premature.

1 For example, see "Stocks Quants are Reeling from the Worst Run in 8 Years." Bloomberg, July 11, 2018.

FURTHER READING:

Subscribe todayto have insights delivered to your inbox.

2 The value investment style characteristics for the MSCI Enhanced Value index construction are defined using book value to price, forward earnings yield and cash flow from operations-to-enterprise value.book value to price, forward earnings yield and cash flow from operations-to-enterprise value.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.