What it may mean for Japanese stocks if easy money ends

Blog post

November 22, 2018

Some observers are concerned that when the Bank of Japan (BOJ) eventually ends its ultra-easy monetary policy,1 it could hurt the Japanese stock market. Part of this concern stems from the fact that the BOJ's unconventional monetary policy involves purchasing Japanese exchange-traded funds (ETFs). Recently, Bloomberg cited analysts' views that unwinding the ETF purchase program "would trigger a large decline in the market."2

If we applied shocks to the system, our stress tests showed that the defensive nature of the minimum volatility factor, as proxied by the MSCI Japan Minimum Volatility Index,3 would provide downside protection in a bearish scenario, a small return shortfall in a bullish scenario and lower volatility in both.

IS THE BEST OFFENSE A GOOD DEFENSE?

One objective of the minimum volatility factor is to seek exposure to the broad equity premium while reducing risk relative to the market. The exhibit below illustrates how the MSCI Japan Minimum Volatility Index has performed over the last 30 years.

ACTIVE RETURN OF MINIMUM VOLATILITY VS. BROAD MARKET RETURN IN JAPAN

Data from May 1988 to September 2018

STRESS TESTING TWO SCENARIOS

In this blog post, we review the results of modeling two hypothetical scenarios as the BOJ ends its monetary easing.

For both scenarios, we assume that Japanese government bond yields rise to the level of November 2012, a month before Prime Minister Abe won a landslide victory in the general election and called for easier monetary policy. We also assume the U.S. dollar/Japanese yen (USD-JPY) rate falls to 99, the purchasing power parity (PPP) rate for 2018 estimated by the International Monetary Fund (IMF).4

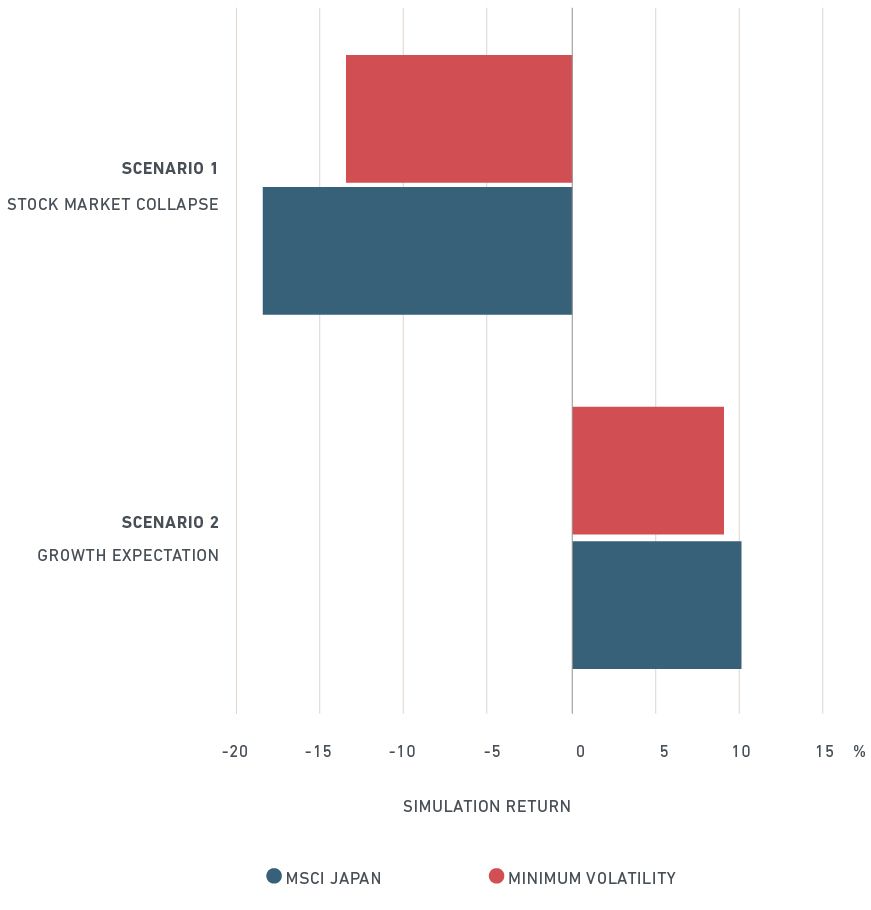

SCENARIO 1: STOCK MARKET COLLAPSES

In this scenario, investors lose confidence in Japan, as they believe that easy monetary policy is vital to keep the Japanese stock market near its current level. The Japanese stock market declines by 18%.5

SCENARIO 2: STOCK MARKET RISES ON GROWTH EXPECTATIONS

In this scenario, investors expect positive news for Japanese economic growth and inflation prospects. The Japanese stock market goes up by 10% despite the appreciation of the yen and the shock on the Japanese government bond market.

The exhibit below illustrates the simulated impact of our two scenarios.6 Low volatility stocks, as proxied by the MSCI Japan Minimum Volatility Index, showed a lower variation compared to the Japanese stock market as a whole, proxied by the MSCI Japan Index, in both the bear- and bull-market scenarios. Additionally, our testing showed Japanese minimum volatility stocks outperforming in the bearish scenario and slightly underperforming in the bullish one.

SIMULATED IMPACT OF STRESS SCENARIOS

Data as of Sept. 28, 2018. The impact of the shocks on portfolios was estimated using the correlated stress testing functionality of BarraOne and the BIM303L model.

Despite the belief of some investors that minimum volatility tends to exhibit bond-like behavior, it has not necessarily underperformed the broad market when there has been a significant negative shock of higher interest rates on the bond market.7 Instead, the performance has been partly determined by the overall economic and market environment that coincides with the interest rate rise. What is revealed by our stress tests is that the defensive nature of minimum volatility may help mitigate a decline in Japanese equities in the scenarios we tested.

1 Fujioka, T. "Kuroda Hints at Policy Normalization as Prices, Economy Improve." Bloomberg, Nov. 4, 2018.

2 Hoenig, H. and C. Whiteaker, "The Bank of Japan's High-Wire Act." Bloomberg, Sept. 18, 2018.

3 Some Japanese institutional investors prefer the MSCI Nihonkabu (Japan ex. REIT) Minimum Volatility Index due to their investment constraints. An analysis based on that index provided similar results as the analysis in this blog post.

4 International Monetary Fund, World Economic Outlook Database, April 2018

5 Assuming stock beta on bonds is 1.6, as in Ruban, O. (2013). "Stress Scenarios for Japanese Government Bond Yields: Insights from the Barra Integrated Model." MSCI Research Insight, p. 8.

6 This report contains analysis of historical data, which includes hypothetical, backtested or simulated performance results. There are frequently material differences between backtested or simulated performance results and actual results subsequently achieved by any investment strategy. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. None of the information or analysis herein is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision or asset allocation and should not be relied on as such.

7 Wei, Z. (2017). "What do rising interest rates mean for minimum volatility strategies?" MSCI Research Insight.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.