What’s Driving High-Yield Spreads?

Blog post

June 14, 2018

The recent trend in high-yield market spreads appears to relate more to concern about rising rates than the potential for credit losses. However, investors should be aware that the impressive recent performance of short-dated high yield bonds and floating-rate leveraged loans may be reversed if credit conditions begin to deteriorate.

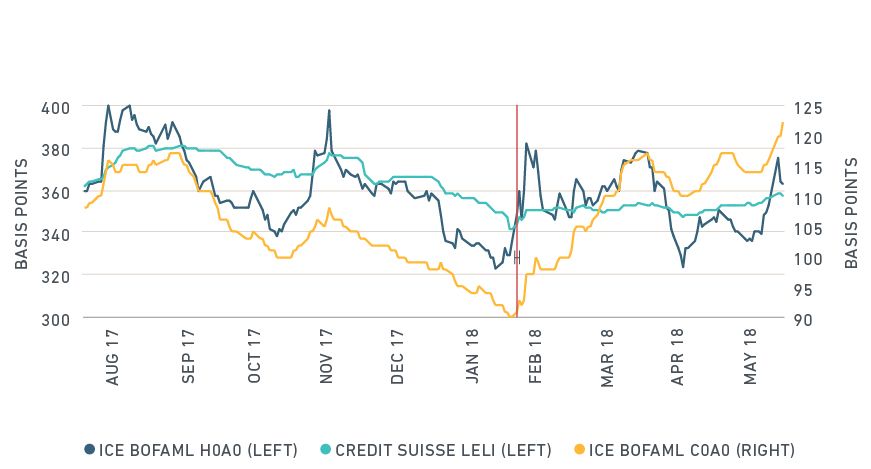

When the CBOE Volatility Index (the VIX) spiked in early February, spreads on corporate bonds and loans (typically low-rated credits) moved sharply higher. Since then, investment-grade spreads have remained above their previous lows, while high-yield spreads have tightened. Given the historic linkages between the equity and credit markets, as well as rising expected default rates from survey data,1 the current asymmetry presents a puzzle.

CORPORATE, HIGH-YIELD AND LEVERAGED LOAN SPREADS

Data for the Credit Suisse LELI index discount margins provided by Credit Suisse, used with permission. Data for the ICE BofAML USD High Yield Index (H0A0) and ICE BofAML USD Corporate Index (C0A0) option-adjusted spreads provided by ICE BofAML Global Research, used with permission.

FITTING THE PIECES TOGETHER

One possible way of reconciling these co-movements is if the current market is compensating duration risk more than default risk. The loan market is characterized by floaters, and the high-yield sector has roughly half the interest rate sensitivity of the investment-grade sector. As a result, investors who want exposure to lower-rated credits but are concerned about the possibility of rising rates may seek lower-rated short-duration bonds. We investigate this possibility by creating hypothetical portfolios from the dollar-denominated, large-issue, B-rated corporate bond universe for illustrative purposes.

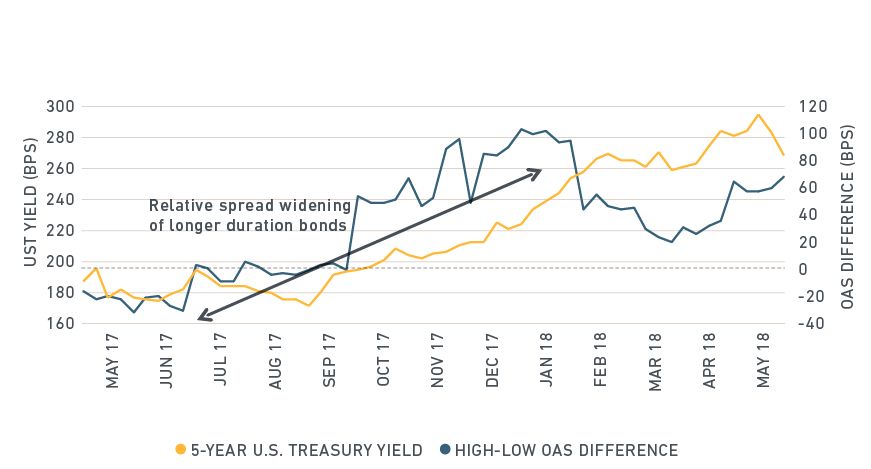

We first filter bonds priced below 95, to avoid selecting assets experiencing distress, and then calculate asset-level effective duration each month. The bonds are subsequently sorted into 10 ascending portfolios according to their durations, and we calculate the spread differences between the long-duration (10th decile) and short-duration (1st decile) portfolios. In a scenario where duration risk is more compensated than default risk, we expect the difference in spreads to expand as rates rise. And, in fact, as shown in the exhibit below, the spread difference moved from negative a year ago to positive as rates began to rise.

OAS DIFFERENCE FOR HIGH-LOW DURATION B-RATED BOND PORTFOLIOS

Option-adjusted spread differences for duration-sorted B-rated corporate bond portfolios (monthly rebalancing for large, fixed-rate assets priced greater than 95)

While our analysis suggests that credit spreads in the current environment may be driven more by rising rates than increasing default expectations, the market also incorporates other uncertainties that could be combining to produce the puzzle we observe. It may simply be that old structural relationships are waning for the time being. Nevertheless, the market's focus could quickly shift if credit conditions deteriorate, leaving the short-duration high-yield sector vulnerable to rapidly widening spreads.

1 Leveraged Loan Experts Hike US Default Rate Expectations, April 18, 2018,

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.