Which ESG Issues Mattered Most? Defining Event and Erosion Risks

- Very different ESG issues can be material for different industries. Our research suggests that risks can be divided into two main types: "event" risks and "erosion" risks to companies' long-term competitiveness.

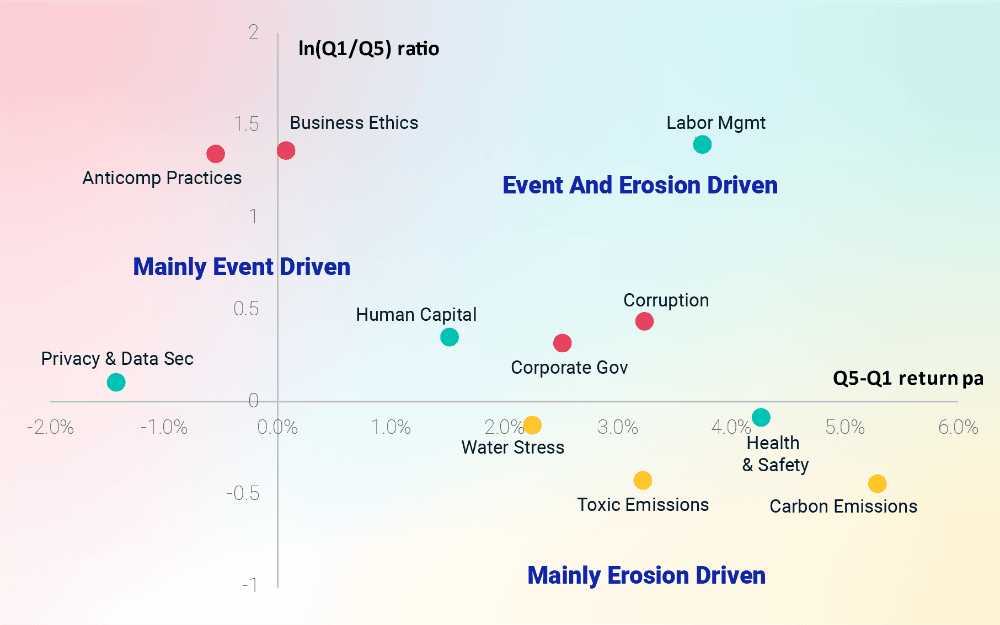

- Environmental Key Issues were purely erosion-driven (they unfolded over time). Social Key Issues showed a mix of event-driven and erosion-driven characteristics, while Governance issues had the highest share of event risks.

- Highly active portfolio managers may want to focus on mitigating short-term event risks. In comparison, portfolio managers building diversified portfolios with long investment horizons may be more focused on long-term erosion risks.

('GICS Sector', 'GICS Sector') | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') | ('Environmental', 'Carbon Emissions') | ('Environmental', 'Product Carbon Footprint') | ('Environmental', 'Climate Change Vulnerability') | ('Environmental', 'Water Stress') | ('Environmental', 'Biodiversity Land Use') | ('Environmental', 'Raw Material Sourcing') | ('Environmental', 'Financing Environmental Impact') | ('Environmental', 'Toxic Emissions & Waste') | ('Environmental', 'Packaging Material Waste') | ('Environmental', 'Electronic Waste') | ('Environmental', 'Opportunities in Clean Tech') | ('Environmental', 'Opportunities in Green Building') | ('Environmental', 'Opportunities in Renewable Energy') | ('Social', 'Labor Management') | ('Social', 'Health & Safety') | ('Social', 'Human Capital Development') | ('Social', 'Supply Chain Labor Standards') | ('Social', 'Product Safety & Quality') | ('Social', 'Chemical Safety') | ('Social', 'Financial Product Safety') | ('Social', 'Privacy & Data Security') | ('Social', 'Insuring Health & Demographic Risk') | ('Social', 'Responsible Investment') | ('Social', 'Controversial Sourcing') | ('Social', 'Access to Communications') | ('Social', 'Access to Finance') | ('Social', 'Access to Health Care') | ('Social', 'Opportunities in Nutrition & Health') | ('Governance', 'Corporate Governance') | ('Governance', 'Corruption & Instability') | ('Governance', 'Financial System Instability') |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

('GICS Sector', 'GICS Sector') Energy | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 10101010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Oil & Gas Drilling | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Energy | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 10101020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Oil & Gas Equipment & Services | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Energy | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 10102010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Integrated Oil & Gas | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Energy | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 10102020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Oil & Gas Exploration & Production | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Energy | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 10102030 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Oil & Gas Refining & Marketing | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Energy | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 10102040 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Oil & Gas Storage & Transportation | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Energy | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 10102050 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Coal & Consumable Fuels | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15101010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Commodity Chemicals | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15101020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Diversified Chemicals | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15101030 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Fertilizers & Agricultural Chemicals | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15101040 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Industrial Gases | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15101050 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Specialty Chemicals | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15102010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Construction Materials | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15103010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Metal & Glass Containers | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15103020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Paper Packaging | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15104010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Aluminum | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15104020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Diversified Metals & Mining | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15104025 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Copper | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15104030 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Gold | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15104040 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Precious Metals & Minerals | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15104045 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Silver | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15104050 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Steel | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15105010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Forest Products | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Materials | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 15105020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Paper Products | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35101020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Health Care Supplies | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35102010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Health Care Distributors | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35102015 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Health Care Services | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35102020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Health Care Facilities | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35102030 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Managed Health Care | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35103010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Health Care Technology | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35201010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Biotechnology | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35202010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Pharmaceuticals | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Health Care | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 35203010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Life Sciences Tools & Services | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Utilities | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 55101010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Electric Utilities | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Utilities | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 55102010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Gas Utilities | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Utilities | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 55103010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Multi-Utilities | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Utilities | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 55104010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Water Utilities | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Utilities | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 55105010 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Independent Power Producers & Energy Traders | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

('GICS Sector', 'GICS Sector') Utilities | ('GICS Sub-Industry Code', 'GICS Sub-Industry Code') 55105020 | ('GICS Sub-Industry Name', 'GICS Sub-Industry Name') Renewable Electricity | ('Environmental', 'Carbon Emissions') None | ('Environmental', 'Product Carbon Footprint') None | ('Environmental', 'Climate Change Vulnerability') None | ('Environmental', 'Water Stress') None | ('Environmental', 'Biodiversity Land Use') None | ('Environmental', 'Raw Material Sourcing') None | ('Environmental', 'Financing Environmental Impact') None | ('Environmental', 'Toxic Emissions & Waste') None | ('Environmental', 'Packaging Material Waste') None | ('Environmental', 'Electronic Waste') None | ('Environmental', 'Opportunities in Clean Tech') None | ('Environmental', 'Opportunities in Green Building') None | ('Environmental', 'Opportunities in Renewable Energy') None | ('Social', 'Labor Management') None | ('Social', 'Health & Safety') None | ('Social', 'Human Capital Development') None | ('Social', 'Supply Chain Labor Standards') None | ('Social', 'Product Safety & Quality') None | ('Social', 'Chemical Safety') None | ('Social', 'Financial Product Safety') None | ('Social', 'Privacy & Data Security') None | ('Social', 'Insuring Health & Demographic Risk') None | ('Social', 'Responsible Investment') None | ('Social', 'Controversial Sourcing') None | ('Social', 'Access to Communications') None | ('Social', 'Access to Finance') None | ('Social', 'Access to Health Care') None | ('Social', 'Opportunities in Nutrition & Health') None | ('Governance', 'Corporate Governance') None | ('Governance', 'Corruption & Instability') None | ('Governance', 'Financial System Instability') None |

- Environmental ("E pillar"): Carbon emissions, water stress, toxic emissions and waste

- Social ("S pillar"): Labor management, health and safety, human-capital management and privacy and data security

- Governance ("G pillar"): Corporate governance, business ethics, corruption and instability and anticompetitive practices

- The cash-flow channel, whereby companies better at managing intangible capital (such as employees) may have been more competitive and hence more profitable over time

- Idiosyncratic risk, whereby companies with stronger risk management practices may have experienced fewer incidents that triggered unanticipated costs, such as accidents

- Systematic risk, whereby companies that used resources more efficiently may have been less susceptible to market shocks such as fluctuations in energy price

- Environmental Key Issues:

- The three environmental Key Issues — carbon emissions, water stress and toxic emissions — were driven by erosion risk. They showed positive long-term differences between the top- and bottom-scoring companies. However, both top- and bottom-scoring companies showed negligible differences in propensity to event risks.

- Social Key Issues:

- The Key Issues under the Social pillar showed more balanced results, with differences in labor management (e.g., mitigating labor conflicts) showing strong event- and erosion-risk characteristics. In fact, top-scoring companies on labor management not only outperformed bottom-scoring companies by an average of 3.7% per year, but also showed significant reductions in event risks — i.e., the top-scoring companies experienced severe stock-price losses only one-fifth as frequently as the low scorers.

- Health and safety showed equally strong positive long-term performance differences; however, it showed minimal differentiation on event risk between high- and low-scoring companies.

- Interestingly, though high-profile cases such as Equifax and Facebook might have suggested otherwise, differences in companies' management of privacy and data security have not historically contributed to positive performance during this period, nor have the top-scoring companies avoided more negative events than low-scoring companies.

- Governance Key Issues:

- Governance-related Key Issues as a whole showed the strongest results along both risk dimensions. However, business ethics and anticompetitive practices showed much stronger event-risk characteristics with minimal erosion risk. The bottom-scoring companies on business ethics were approximately four times more likely than top-scoring companies to experience a severe stock-price loss during this period, while the bottom-scoring companies on corruption were only about 1 1/2 times more likely than the top-scoring companies to do so.

- In contrast, corporate governance — and especially the corruption Key Issue — showed positive long-term differences, with stronger erosion-risk characteristics and less event-driven risk differentiation.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.