Would Integrating ESG in Chinese Equities Have Worked?

Blog post

July 7, 2020

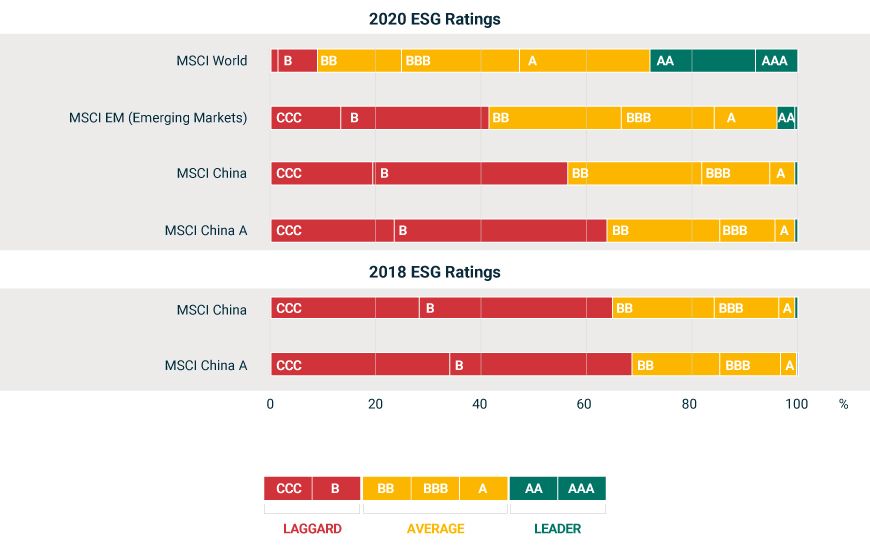

- ESG ratings of Chinese companies improved significantly over the past two years.

- Chinese companies with better ESG performance tended to exhibit lower systematic risk than low ESG-rated Chinese companies, implying potentially lower funding costs.

- Excluding low ESG-ranked stocks could have aided the risk and return characteristics of a sample of China-focused active funds over a 5 ½ years period.

ESG Ratings Among Developed-Market, Emerging-Market and Chinese Companies

Data as of May 29, 2020, based on the MSCI World Index, MSCI EM Index, MSCI China Index and the MSCI China A Index. "2018 ESG Ratings" were calculated using constituents as of May 29, 2020 and ESG ratings as of May 31, 2018. MSCI ESG Ratings use a rules-based methodology to identify industry leaders and laggards. We rate companies on a "AAA to CCC" scale according to their exposure to ESG risks and how well they manage those risks relative to peers. The MSCI China Index corresponds to Chinese equities listed around the world and it is a subset of the MSCI Emerging Markets Index. The MSCI China A Index includes Chinese stocks listed in mainland China, which have been included in MSCI Emerging Markets at a 20% inclusion factor.

But has ESG performance in China been related to financial risks and returns?

ESG and Financial Performance in China

In our previous research, based on developed-market stocks, we identified three transmission channels through which ESG ratings may reflect financial risk and returns: the cash-flow channel, idiosyncratic-risk channel and the valuation channel.4

- The cash-flow channel, whereby companies better at managing intangible capital (such as employees) may have been more competitive and hence more profitable over time

- The idiosyncratic-risk channel, whereby companies with stronger risk management practices may have experienced fewer incidents, such as accidents, that triggered unanticipated costs

- The valuation channel, whereby companies that used resources more efficiently may have been less susceptible to market shocks, such as fluctuations in energy prices. Lower systematic risk may lead to lower funding costs (cost of capital). In a discounted cash-flow framework, lower funding costs may imply higher valuations

Average Z-Scores of Financial Variables for China ESG Quintiles

Data from May 2010 to May 2020, based on MSCI China Index constituents. Bars represent average monthly z-scores for each ESG quintile. Q1 represents the quintile with the lowest MSCI ESG scores and Q5 the quintile of companies with the highest ESG scores. Gross profitability is computed as the most recently reported sales less cost of goods sold, divided by most recently reported company total assets. Trailing dividend yield is computed by dividing the trailing 12-month dividend per share by the price at the last month end. Systematic risk is calculated as the volatility predicted by all the factors of MSCI's Barra® All China Equity Model (ACH1), and specific risk is the volatility that is not explained by any factors of ACH1.

We found that the relationship between ESG and the cash-flow channel and idiosyncratic-risk channel was less clear than in our previous studies focused on global equities. On the other hand, high China ESG-score quintiles (Q4 and Q5) generally had lower systematic risks than low ESG-score quintiles over our study period, which supports our thesis that these stocks historically have had lower funding costs.

Regarding Chinese stock performance, the top ESG quintile outperformed the bottom ESG quintile over the last 10 years, although this was not always the case in shorter time periods.

We conducted a similar review of MSCI China A Index constituents. Here too the top ESG quintile outperformed the bottom quintile for China A shares over the last two years. However, the short history of MSCI ESG scores for the index constituents means we have far less confidence in these results than we have for the MSCI China Index.8

Financial Performance of Top and Bottom ESG Quintiles

Data from May 2010 to May 2020 for MSCI China Index constituents and from May 2018 to May 2020 for MSCI China A Index constituents. Monthly data based on end-of-month dates. Relative performance shows the cumulative return of the top ESG quintile (Q5) divided by the cumulative return of the bottom ESG quintile (Q1).

Applying an ESG Overlay on Active Funds

In our previous study, we found that applying an ESG overlay to active fund holdings using ESG ratings and ESG momentum could have led to an improvement in risk and risk-adjusted-return characteristics.9 We applied the same ESG-overlay method to China-focused active funds to see if excluding companies with lower ESG ratings could have improved the investment outcome.

In this analysis, we studied 54 China-focused active funds, from July 2014 to December 2019.10 If these funds had excluded the worst 10% ESG performers, their simulated returns would have been enhanced by 33 to 133 basis points (bps) per year.

Excluding the lowest-rated 30% of companies could have helped returns for second- and third-quartile managers, but would have had less of an impact for the top- and bottom-quartile managers.

We saw a reduction in volatility across all quartiles except Q3 when we excluded the lowest-rated 30%.

We did not find a significant difference in average factor exposures of active funds after excluding the worst 10% and 30% companies.

Effect of Integrating ESG on Simulated China Active Funds

Annualized return and volatility of active China funds versus the MSCI China Index, from July 2014 to December 2019. The active fund data is based on MSCI Peer Analytics Database. We grouped the funds into quartiles based on historical performance: Q1 denotes the worst-performing group of funds, whereas Q4 denotes the best-performing group of funds. Two levels of ESG-laggard exclusion were tested: 10% and 30%, where the ESG scores were neutralized for size biases.

ESG investing in Chinese stocks is still in its infancy. Our analysis, however, showed that ESG was associated with the level of systematic risk and stock performance in China. As ESG becomes widely integrated in China, equity managers may want to scrutinize these characteristics more closely.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1See, for example: “ESG and alpha in China.” Principles for Responsible Investing, March 18, 2020.2MSCI ESG Research data and information provided by MSCI ESG Research LLC. MSCI Equity Indexes are products of MSCI Inc. and are administered by MSCI UK Limited.3Acosta, F. N. “Chinese company ESG scores inching upward: MSCI.” Fund Selector Asia, Jan. 6, 2020.4Giese, G., et al. 2019. “Foundations of ESG Investing: How ESG Affects Equity Valuation, Risk and Performance.” .5Seretis, P., et al. 2020. “ESG investing in emerging markets.” MSCI Research Insight.6This report contains analysis of historical data, which may include hypothetical, backtested or simulated performance results. There are frequently material differences between backtested or simulated performance results and actual results subsequently achieved by any investment strategy.

The analysis and observations in this report are limited solely to the period of the relevant historical data, backtest or simulation. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. None of the information or analysis herein is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision or asset allocation and should not be relied on as such.7Specifically, we created size-adjusted ESG scores as the residuals from regressing standard MSCI ESG scores on the log market capitalization and an intercept variable.8MSCI ESG Research began the ESG Rating assessment of MSCI China A Index constituents on May 28, 2018.9For an introduction to this methodology, see: Guise, G., et al. 2018. “Foundations of ESG investing Part 4: Integrating ESG into Factor Strategies and Active Portfolios.” MSCI Research Insight.

For a discussion of integrating ESG into investing in emerging markets and Asia, see: Wei, Z. “Integrating ESG in emerging markets and Asia.” MSCI Blog, March 18, 2020.10We limited the study period from June 2014 to December 2019 because there are relatively few China-focused active equity funds with consecutive and complete constituent disclosure prior to June 2014, and because lack of availability of mutual-fund data after December2019.

The analysis and observations in this report are limited solely to the period of the relevant historical data, backtest or simulation. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. None of the information or analysis herein is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision or asset allocation and should not be relied on as such.7Specifically, we created size-adjusted ESG scores as the residuals from regressing standard MSCI ESG scores on the log market capitalization and an intercept variable.8MSCI ESG Research began the ESG Rating assessment of MSCI China A Index constituents on May 28, 2018.9For an introduction to this methodology, see: Guise, G., et al. 2018. “Foundations of ESG investing Part 4: Integrating ESG into Factor Strategies and Active Portfolios.” MSCI Research Insight.

For a discussion of integrating ESG into investing in emerging markets and Asia, see: Wei, Z. “Integrating ESG in emerging markets and Asia.” MSCI Blog, March 18, 2020.10We limited the study period from June 2014 to December 2019 because there are relatively few China-focused active equity funds with consecutive and complete constituent disclosure prior to June 2014, and because lack of availability of mutual-fund data after December2019.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.