Are You Ready for Uniform MBS? (Part 2)

Blog post

April 26, 2019

ALIGNING PREPAYMENT SPEEDS

Aligning prepayment speeds of Fannie Mae and Freddie Mac securities presents a major challenge to the success of uniform mortgage-backed securities (UMBS), which the two government-sponsored enterprises will launch on June 3.1 Historical analysis shows that relatively small prepayment differences could cause large pricing differentials between the two agencies' securities. The current rule2 by the Federal Housing Finance Agency (FHFA) regarding this concern may not be adequate to ensure the success of UMBS.A TWO-SPEED MARKET

As is commonly observed, MBS with faster prepayment speeds are penalized by the market and have been a fundamental cause of liquidity issues in the Freddie Mac to-be-announced (TBA) market. The potential speed divergence between Fannie Mae and Freddie Mac securities may lead to two consequences:

- The "faster" agency security might end up trading in the UMBS market, while the "slower" security might be traded in the specified market.

- There might be a race to the bottom; the market could price the combined TBA market to align with the "faster" agency security.

FHFA Rules | Cohort | Worst Quartile |

|---|---|---|

FHFA Rules Misalignment | Cohort 2% CPR | Worst Quartile 5% CPR |

FHFA Rules Material misalignment | Cohort 3% CPR | Worst Quartile 8% CPR |

"Cohort" includes all loans originated with same net coupon and vintage year; "Worst Quartile" includes the top 25% securities with fastest prepayment speed within a cohort. Source: FHFA

THE STORY OVER THE PAST TWO DECADES

We analyzed nearly two decades of prepayment data and looked closely at the most prevalent cohorts — i.e., all loans aggregated with a particular coupon and vintage, excluding those held by the Federal Reserve or locked up in collateralized mortgage obligations (CMOs) — revealing the evolution of market pricing with respect to changes in prepayment behavior.

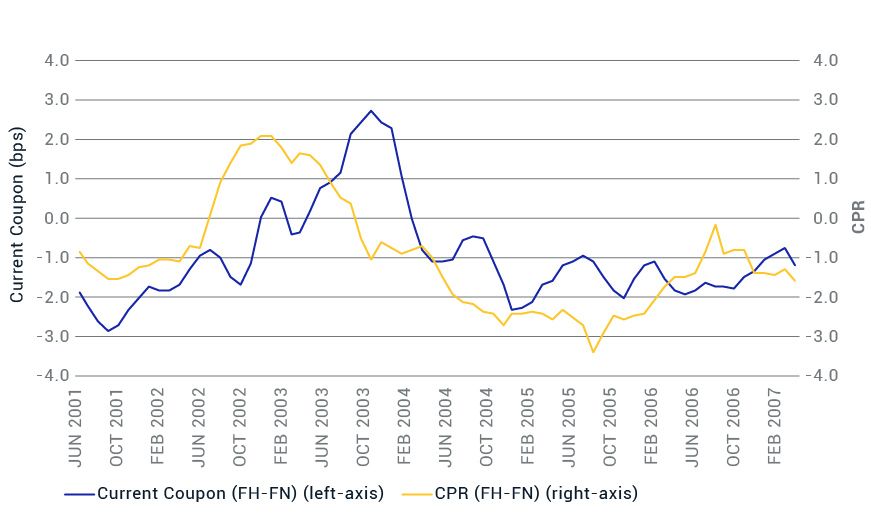

PREPAYMENT DIFFERENCE PRECEDED MARKET REPRICING BEFORE FINANCIAL CRSIS

Cohort: 6.5% coupon/2001 vintage. Source: Freddie Mac, Fannie Mae, MSCI, Recursion

The exhibit above shows the differences between Fannie Mae's and Freddie Mac's securities, in terms of current coupon yield and CPR. A higher current coupon yield3 means a lower price. Before the global financial crisis, the extraordinary refinance waves at times exceeded 70% CPR in 2002 and 2003. Freddie Mac's 2001-vintage security experienced a mere 2%-CPR faster prepayment speed than Fannie Mae's comparable MBS, but Freddie Mac's performance suffered by almost 3 basis points (bps), after a delay. After 2003, however, Fannie Mae's comparable MBS started to experience faster prepayment (due to looser standards for cash-out refinancing, among other things), which later led to almost 2 bps in better pricing for the Freddie Mac MBS.

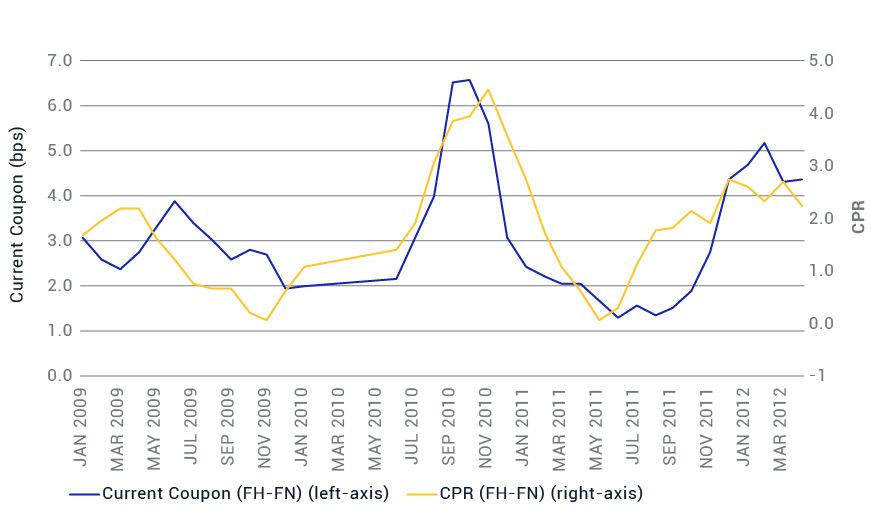

PREPAYMENT DIFFERENCE IN SYNC WITH MARKET PRICING AFTER FINANCIAL CRISIS

Cohort: 5% coupon/2008 vintage. Source: Freddie Mac, Fannie Mae, MSCI, Recursion

After the financial crisis, there was a relatively large prepayment divergence in 2010. The Freddie Mac MBS traded more than 6 bps lower relative to the comparable Fannie Mae security, in sync with the 3%-CPR prepayment differential.

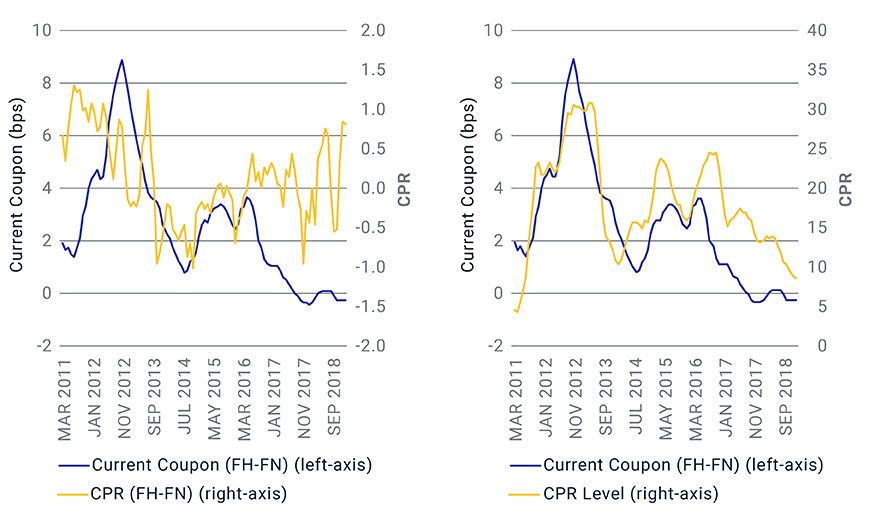

MARKET PRICING NOT DRIVEN BY ACTUAL PREPAYMENT DIFFERENCE (LEFT), BUT BY FEAR OF WHAT MIGHT HAPPEN (RIGHT), SINCE 2012

Cohort: 4.5% coupon/2010 vintage. Source: Freddie Mac, Fannie Mae, MSCI, Recursion

Since 2012, the relationship between prepayment difference and pricing difference seems to have disappeared. Instead, the relative pricing between the two agencies' MBS has likely been driven by fears of refinancing by borrowers. As soon as refinancing levels picked up with the rates rally of 2016, the market immediately started to price Freddie Mac MBS as much as 8 bps lower relative to Fannie Mae MBS, ignoring the actual prepayment difference, as the above exhibit's underlying data shows.

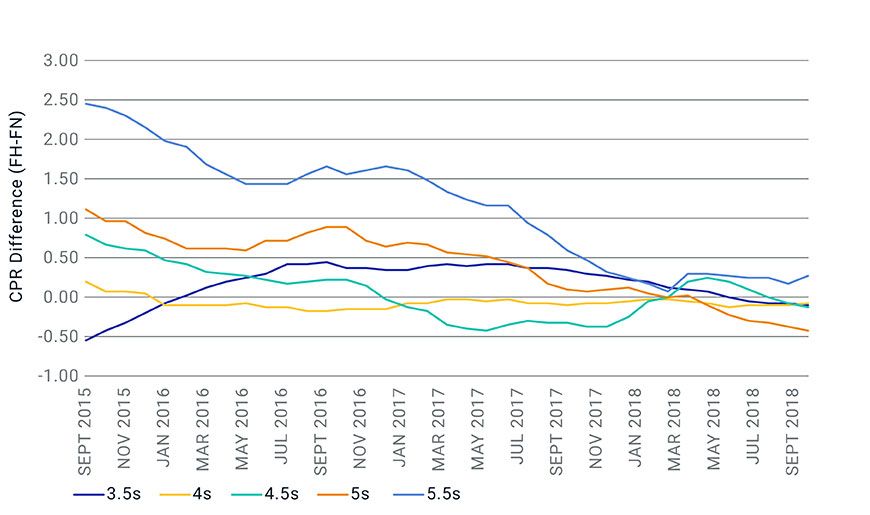

PREPAYMENT SPEEDS HAVE CONVERGED, LIKELY DUE TO HIGHER RATES IN RECENT YEARS

Source: Freddie Mac, Fannie Mae, MSCI, Recursion

Historical prepayment divergence was mainly due to differences in the refinancing rate. The exhibit above shows the current convergence of prepayment speeds, as the overall prepayment speed has decreased to roughly 8% CPR, dominated by base prepayment with higher mortgage rates.4, 5 But the recent convergence hasn't experienced a substantial test of a lower-rate environment, which has historically tended to increase prepayment speeds and create Fannie-Freddie misalignment.

Our analysis of Fannie Mae and Freddie Mac securities data showed that a cohort-level prepayment-speed differential of 2% to 3% CPR has historically led to very substantial pricing differences between the two agencies' securities. The two agencies are supposed to compete on mortgage-origination efficiency, especially with the imminent emergence of the digital mortgage.6 Additionally, some prepayment differences could be due to choices made by mortgage originators/servicers and CMO lockups by securitization firms — circumstances beyond the agencies' control. Meaningful prepayment divergence is not unlikely.

It's a very tough job for the FHFA to maintain prepayment-speed alignment, and enforce remedies if misalignment occurs, potentially jeopardizing a successful UMBS effort. Investors will face the challenge of staying ahead of the market.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Yu, Y. (2019). “Are You Ready for Uniform MBS? (Part 1): Freddie Mac securities exchange.” MSCI Blog.2“Uniform Mortgage-Backed Security Final Rule.” Federal Housing Finance Agency.3Zhang, D. (2017) “Agency MBS Current Coupon Calculation from TBA Prices.” MSCI Model Insight. (Client access only)4Yu, Y. (2018). “Managing MBS risk in a rising rate environment (Part 1).” MSCI Blog.5Yu, Y. (2018). “Managing MBS risk in a rising rate environment (Part 2).” MSCI Blog.6Yu, Y. (2019). “How mortgage fees affect rates and spreads.” MSCI Blog.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.