EU Taxonomy Reporting Has Perplexed Issuers

Key findings

- The reporting templates for EU Taxonomy are complex and financial market participants may require guidance on interpretation and usage to ensure that data is disclosed in the correct format.

- This has been especially true for Non-Financial Reporting Directive (NFRD), where EU Taxonomy regulations mandate the use of reported data and timelines for disclosures related to NFRD.

- MSCI’s EU Taxonomy Reported Data User Guide emphasizes the importance of granular data disclosures and offers insights into the use cases for reported and estimated EU Taxonomy data.

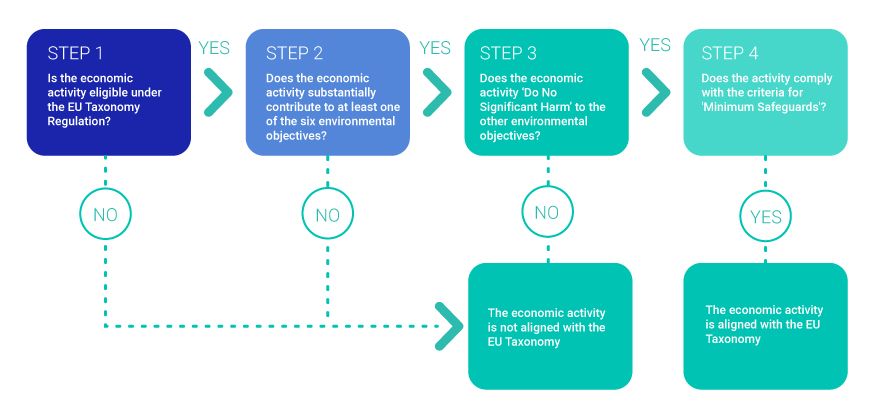

The EU Taxonomy aims to establish criteria to determine the environmental sustainability of economic activities, aiding investment decisions in environmentally sustainable ventures. It defines four overarching conditions that an economic activity must meet to qualify as environmentally sustainable. These conditions, outlined in Article 3, encompass activities that substantially contribute to at least one environmental objective, avoid significant harm to the other environmental objectives, adhere to minimum safeguards and comply with technical screening criteria (see exhibit below).

Many issuers have faced challenges interpreting the reporting templates and requirements outlined in Commission Delegated Regulation (EU) 2021/2178, which supplements Article 8 of the EU Taxonomy Regulation, particularly those related to Non-Financial Reporting Disclosure (NFRD). They require clarity and guidance.

Steps for classification of an economic activity as EU Taxonomy-aligned

Source: MSCI ESG Research as of Aug. 31, 2023.

Non-financial company requirements

Companies are required to provide details on what proportion of assets are eligible for alignment with the EU Taxonomy, i.e., the EUR value or percentage that is in scope or has the potential to be sustainable, as well as the value or percentage that is actually aligned, i.e., is sustainable.

As an example, we can look at vehicle manufacturing, one of the areas detailed in MSCI's EU Taxonomy Reported Data User Guide. Since this activity falls within the scope of the EU Taxonomy, all vehicle manufacturing is considered eligible. However, only electric vehicles, and in some cases, hybrid vehicles are aligned with the sustainable criteria. If a vehicle manufacturing company generates 100% turnover from vehicle sales but only 20% turnover from electric vehicles, then EU Taxonomy-eligible turnover would be 100%, and EU Taxonomy-aligned turnover would be 20%.

With the adoption of the remaining four environmental objectives, the reporting timelines for issuers subject to NFRD are shown in the exhibit below.

Reporting timelines for EU Taxonomy Regulation

Source: MSCI ESG Research as of Aug. 31, 2023.

The EU Taxonomy Regulation, with its robust criteria for assessing environmental sustainability in economic activities, stands as a pivotal framework for guiding responsible investment decisions. Its correct interpretation will be key to ensure that data is disclosed in the correct format and reporting obligations met.

Disclaimer: It is important to note that the information in this blog and the associated user guide is provided "as is" and does not constitute legal advice or any binding interpretation. Any approach to comply with legal, regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.