Cues from Public Markets for Private-Credit Distress

Private credit as a strategy is experiencing its first real rate cycle, and investors who hoped those loans would be light on credit risk may be disappointed.1 Using the MSCI private-credit security-terms dataset and leveraged loan prices, we find that write-downs in private credit have closely tracked trends in leveraged-loan markets, with rates of distress surging as interest rates lifted off from zero.

Rising rates sink all boats

Since mid-2022, senior-loan distress rates have nearly tripled, as our earlier research found. As signs of distress in private-credit senior-loan markets have followed trends in leveraged loans, monthly data and faster reporting for leveraged loans may provide a glimpse into the future for private credit.

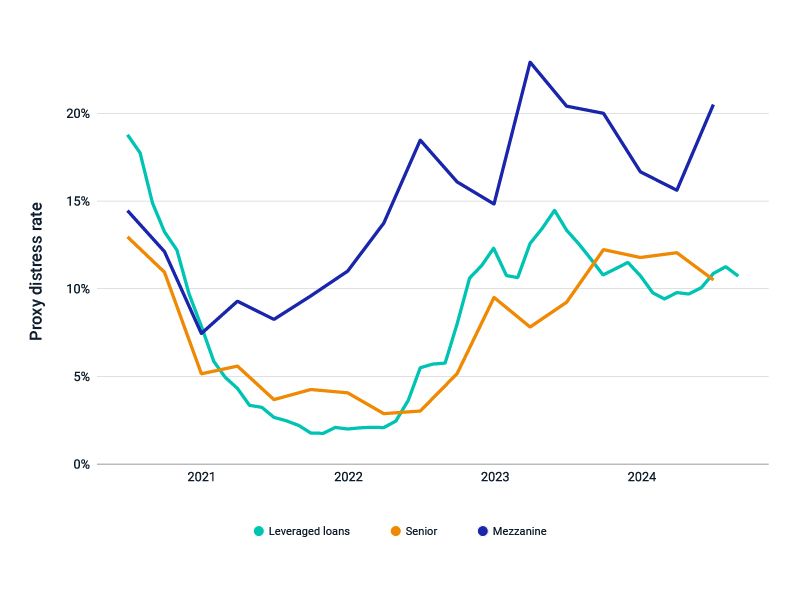

Distress rates among leveraged loans have come down from their peak of 14.5% in May 2023 and stabilized around 11% since late 2023, as interest-rate uncertainty has receded. We see similar stabilization in senior private-credit loans, with around 12% of loans exhibiting signs of distress over the four quarters ending in June 2024. In contrast, rates of distress for mezzanine private-credit loans have been persistently higher and much more volatile. Data from the second quarter of 2024 showed an apparent jump in mezzanine distress, but this could be a false alarm given previous volatility.

Investors concerned about credit risk in their private-capital portfolios should proactively monitor the loans held by their private-capital funds — and keep a close eye on the leveraged-loan markets.

Distress rates stabilized for leveraged and private-credit senior loans

Proxy distress rates for Markit iBoxx USD Leveraged Loan Index and senior and mezzanine private-credit loans. We treat private-credit loans marked at least 20% below cost and leveraged loans trading at least 20% below par as distressed. Leveraged-loan data through August 2024; private-credit loan data through June 2024. Source: MSCI, S&P Dow Jones

Subscribe todayto have insights delivered to your inbox.

Signals of Distress in Private Credit

Private-credit funds are in the spotlight because of their growth — and the opaque credit risk of the loans they hold. We use a signal of nonperformance to examine the trends in defaults for the asset class.

When Spreads Meet: A Changing Picture on Private-Credit Loans

Spreads on corporate mezzanine loans in private-credit funds have fallen dramatically since 2022, changing the picture on the loans that are normally deemed higher-risk than senior loans. Funds treated real-estate borrowers differently, however.

1 Robin Wigglesworth, “How is private credit weathering its first big rate hiking cycle?” Financial Times, Nov. 21, 2024.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.