Signals of Distress in Private Credit

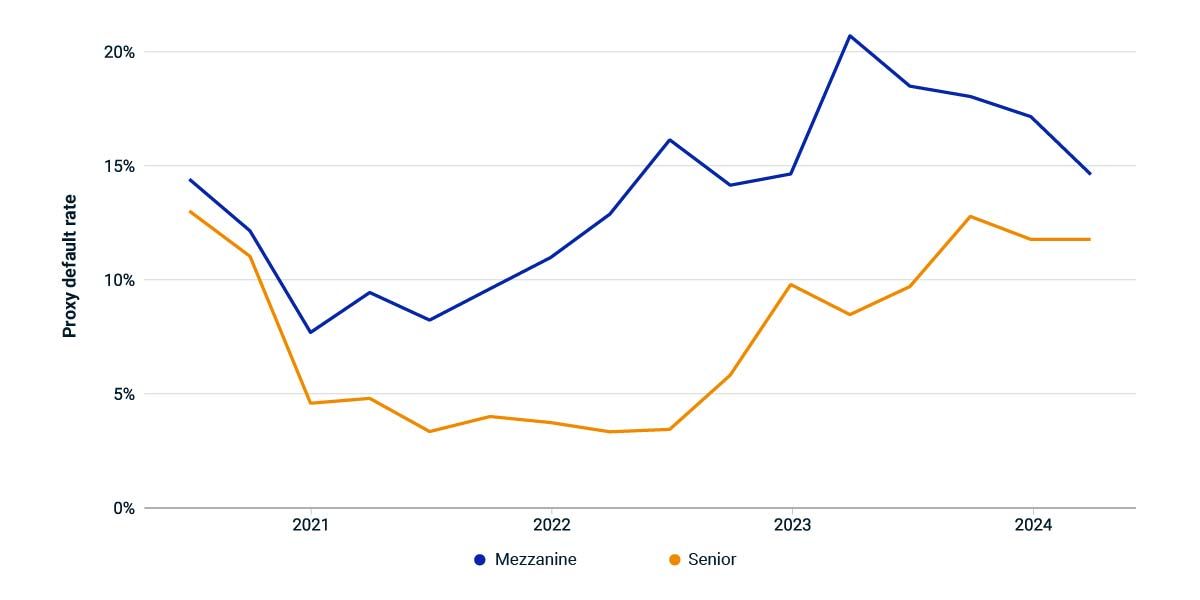

Private credit has grown dramatically in the past decade but funds now face scrutiny over the credit risk of the loans they hold.1 Defaults are challenging to observe in private credit, because general partners (GPs) tend to provide little commentary around loan nonperformance. We can use a loan's valuation and cost basis to signal default, however. In this analysis, based on MSCI Private Capital Transparency Data covering the terms of more than 30,000 loans held by closed-end private funds, we treat loans valued at less than 80% of cost basis as nonperforming.

Rising rates took a toll

Reviewing the trends for mezzanine and senior loans since 2020, two periods stand out. In late 2020, our default signal for both loan types trended sharply downward as pandemic-related concerns subsided. And, since mid-2022, defaults for senior loans have nearly tripled as interest rates lifted off from near-zero levels. Given that private-credit funds predominantly hold floating-rate loans, changing expectations for the path of interest rates can greatly impact a borrowing company's future interest-coverage ratio — and thus likelihood of default.

While we suggested earlier that a loan marked at a discount to cost basis indicated default, the discount could also reflect a rise in spreads. In fact, high-yield spreads have generally been declining since mid-2022, which would artificially depress our default-rate proxy. Thus, the true increase in distress is likely to be even more significant than our proxy implies.

Given GPs' continued reticence to discuss defaults, plus reemerging fears of a recession, it is becoming increasingly important for private-credit investors to proactively monitor default risk in their portfolios.

Default rate for senior loans has nearly tripled since mid-2022

Proxy default rates by calendar quarter. Loans with market value reported at below 80% of cost basis are treated as nonperforming.

Subscribe todayto have insights delivered to your inbox.

Are Private Capital’s Cash Flows Back to Normal?

Private-market investors experienced a sustained slump in distributions across buyout and venture capital and, to a lesser extent, private credit. We look at the recent apparent recovery in private-market cash-flow activity and what that could mean for limited partners.

Private Capital in Focus: Q1 Performance and a Dive into Distributions

We summarize the performance of major asset classes based on the latest update of MSCI’s private-funds data universe and explore trends in distributions — a key concern for asset owners.

Reports of Buyout’s Liquidity Risk Are Greatly Exaggerated

Excess returns in private markets are often attributed to the extra compensation for carrying liquidity risk, but is this perception of risk warranted? We analyzed various buyout-allocation targets to find evidence for the concern.

1 Jodi Xu Klein, “The $1.5 Trillion Private-Credit Market Faces Challenges,” Wall Street Journal, Oct. 16, 2023.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.