SEC Liquidity Proposal: A Better Warning Signal?

The Securities and Exchange Commission's proposed liquidity-rule amendments aim to better prepare managers of open-end investment funds for stressed conditions.1 They would standardize equities-liquidity classifications and prescribe volume-based bucketing, replacing the current approach based on transaction costs.2 But does increasing trading volume always signal better liquidity?

While the proposal simplifies liquidity classifications, our research suggests it may also produce unintended, counterintuitive results during volatile periods, without explicitly accounting for transaction costs.

Differing measures of liquidity

The proposal indicates that asset managers may assume they can trade 20% of the average daily volume (ADV) in one day. Liquidity buckets are assigned based on how quickly 10% of the holdings could be sold; assuming higher ADVs indicate faster selling. However, in volatile markets trading volumes may increase while other liquidity measures — e.g., bid-ask spread and market impact — deteriorate.

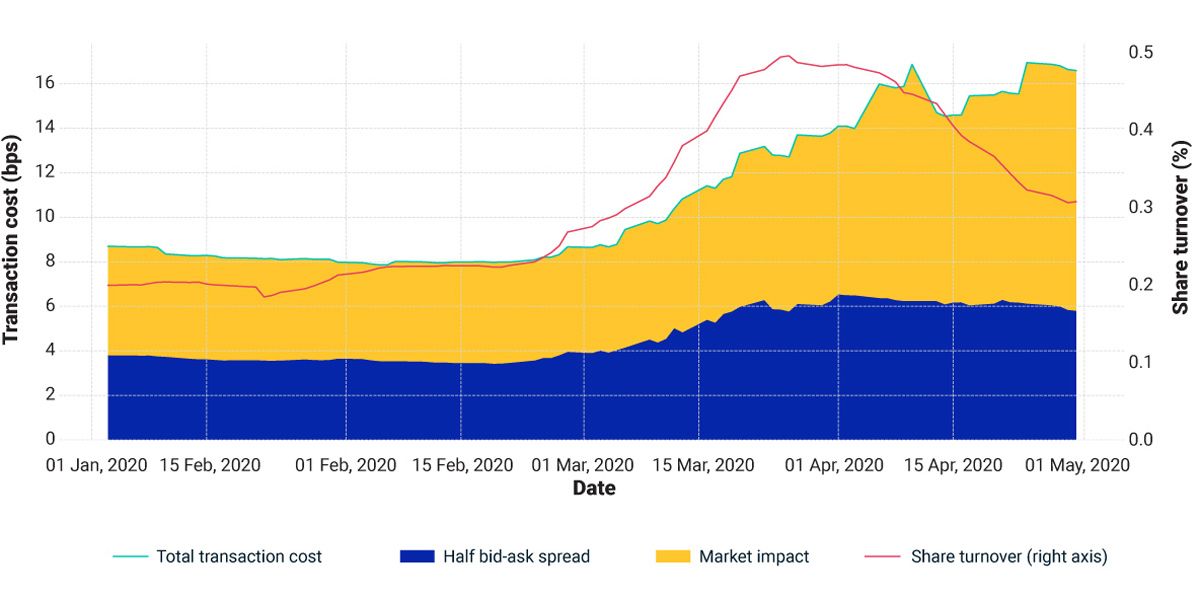

For example, equity trading volume more than doubled during the March 2020 COVID-19 market crisis, while observed bid-ask spreads and modeled transaction costs significantly increased for constituents of the MSCI ACWI Index.3 Applying the proposed amendments, equity funds may have seen their share of illiquid positions decrease in March and positions qualified as highly liquid increase. The liquidity profile may have worsened in April as markets recovered and trading volumes fell.

Transaction costs spiked with higher trading volume

The share turnover is defined as the average daily volume divided by the number of shares outstanding. For aggregation, we used index weights. Source: Refinitiv, Virtu Financial, MSCI

The authors thank Sankruti Mehta for her contribution to this quick take.

Subscribe todayto have insights delivered to your inbox.

What Can Liquidity Tell Us About ETF Prices?

The gap between an ETF’s price and the net asset value (NAV) of the fund can be an important source of risk for investors.

Is There Another Woodford Waiting to Happen?

After the Woodford Equity Income Fund had to gate redemptions, institutional investors may worry that other European UCITS funds could have a similar liquidity mismatch.

Liquidity Risk Monitor Reports

Investment-grade bond transaction costs reached their highest levels since the March 2020 peak during the COVID-19 crisis and transaction costs for bank loans have increased steeply in the last...

1 “Open-End Fund Liquidity Risk Management Programs and Swing Pricing; Form N-PORT.” Securities and Exchange Commission, Nov. 2, 2022.', 'Following the proposal, asset managers would assign their portfolio holdings into one of three liquidity buckets based on how long it takes to convert 10% of the holdings into U.S. dollars. If the time of conversion takes less than three days, the holding is highly liquid. If it takes less than a week, the holding is moderately liquid. Otherwise, the holding is illiquid. ', 'Transaction costs were calculated for an index-replicating portfolio of USD 1 billion. The holdings were kept fixed throughout the analysis period.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.