What If Bond Issuers Meet Their Emissions-Reduction Targets?

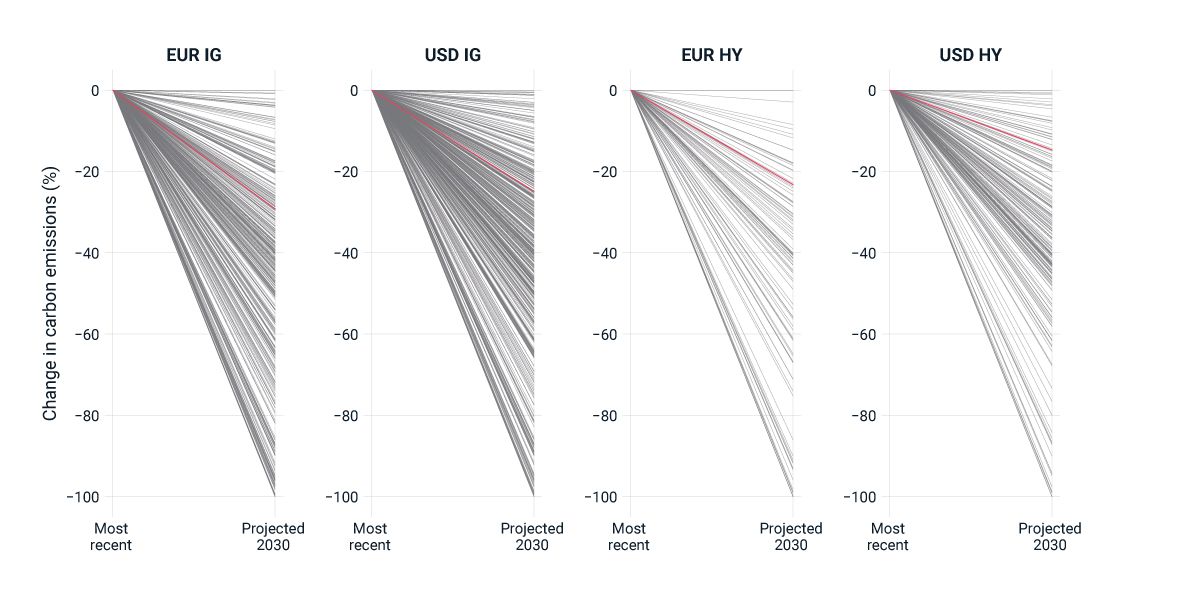

For fixed-income investors with a climate mandate, what could it mean if the issuers in their portfolio meet their emissions-reduction targets? Looking at the emissions targets of companies in the MSCI Corporate Bond Indexes, we found that a notable degree of emission reduction (around 20%) could be achieved at the portfolio level by 2030, assuming the composition of the indexes remains largely unchanged.

We compared the most recent Scope 1 and 2 (S1+2) greenhouse-gas (GHG) emissions of these issuers with their 2030 projected S1+2 emissions, taking the issuers' reduction targets at face value.1 On average, these companies would reduce their emissions by around 20% relative to the most recent levels in our database.

Companies in energy, utilities and materials — the sectors commonly with the highest S1+2 emissions intensities — targeted carbon-emissions reductions of 20% to 40% in the investment-grade indexes by 2030. In contrast, projected emissions reductions for high-yield issuers in these sectors are lower, averaging 10% to 20%. Notably, the EUR-denominated high-yield index projected a larger reduction among utilities companies, driven by issuers in the electric-utilities sub-industry.

What if companies do not meet their targets, however? We'll explore additional scenarios in an upcoming blog post.

S1+2 emissions’ change where issuers meet their stated targets

Each gray line in the plot above represents the carbon emissions at issuer level. The red line represents the average. Data from the constituents of the EUR- and USD-denominated MSCI Investment Grade (IG) Corporate Bond Indexes and MSCI High Yield (HY) Corporate Bond Indexes.

Subscribe todayto have insights delivered to your inbox.

Net-Zerio Glidepaths for Fixed-Income Portfolios

A bond portfolio generates cash flows over time that include coupon payments and the face value of matured bonds, assuming no defaults. With controlled and systematic reinvestment of this cash flow, investors can gradually decarbonize their portfolios on a glidepath.

Corporate Bonds and Climate Change Risk

In this paper, we highlight to investors and portfolio managers the significance of climate-change risk for the value of corporate bonds, as well as provide a framework for further research in this area.

Green Bonds and Climate: Towards a Quantitative Method

While examining use of proceeds remains a key element of analyzing green bonds, we highlight four additional metrics to assess these bonds and their issuers in a more quantitative way. They offer a new set of lenses with which to tackle the analysis.

1 We used the “2030 Projected S1+2 Emissions with Targets at Face Value [tCO2e/yr]” dataset from the MSCI Implied Temperature Rise Model. This data represents a company's projected S1+2 GHG emissions in tonnes of CO2 equivalent for the specific year, taking any considered climate target with sufficient details (contributing targets) at face value. These emissions are projected by taking into account the latest S1+2 emissions data (reported, if available, or estimated, if not) and the company's pledged climate targets to reduce S1+2 emissions, if available. For companies without targets, constant emissions were assumed relative to the most recent data. For bonds that are not covered by the carbon-emissions dataset, the average by sub-industry of the most recently reported or estimated data is assumed.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.