- The default rate for Chinese auto loans in asset-backed securities (ABS) increased rapidly in recent months — possibly due, in part, to an economic slowdown in China.

- The first cases of personal-bankruptcy settlement have spurred discussions of a potential personal-bankruptcy law in China — which could in turn lead to higher default rates if the economic difficulty continues.

- Investors in Chinese consumer ABS may wish to monitor the acceleration of consumer-loan default speeds and increase vigilance ahead of a potentially more borrower-friendly environment for bankruptcy.

The rapid rise of Chinese consumer ABS

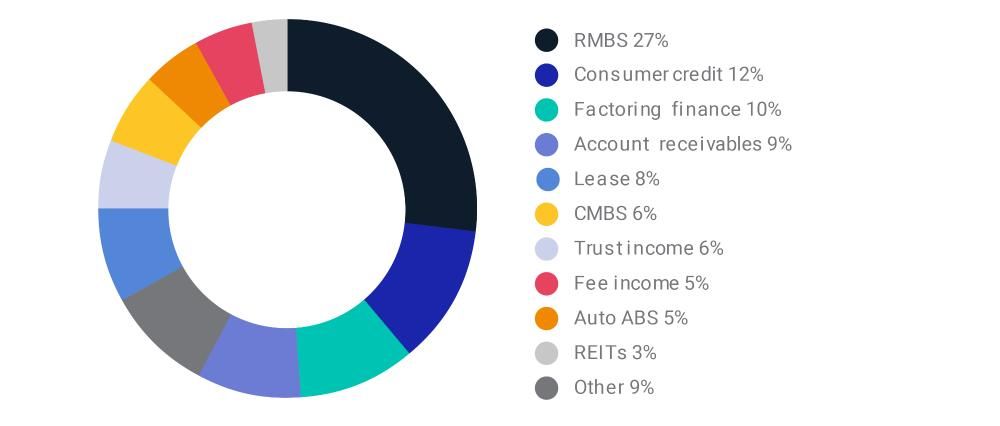

ABS consisting of consumer loans grew dramatically during the last few years. Three asset classes — residential mortgage-backed securities (RMBS), consumer loans and auto loans — accounted for 44% of the Chinese ABS market's total outstanding volume, as of Aug. 13, 2019, according to data from CNABS. Adding other asset deals, such as account receivables and trust income (which are often backed by consumer credit), the total share of consumer credit is well above 50% of total Chinese ABS, as the exhibit below shows.

Chinese ABS by asset type

Source: CNABS, MSCI

Given the large amount of outstanding Chinese consumer credit, and the current uptick in consumer-loan default rates, assessing whether the emerging consumer-bankruptcy regime could lead to an acceleration in default rates may be warranted.

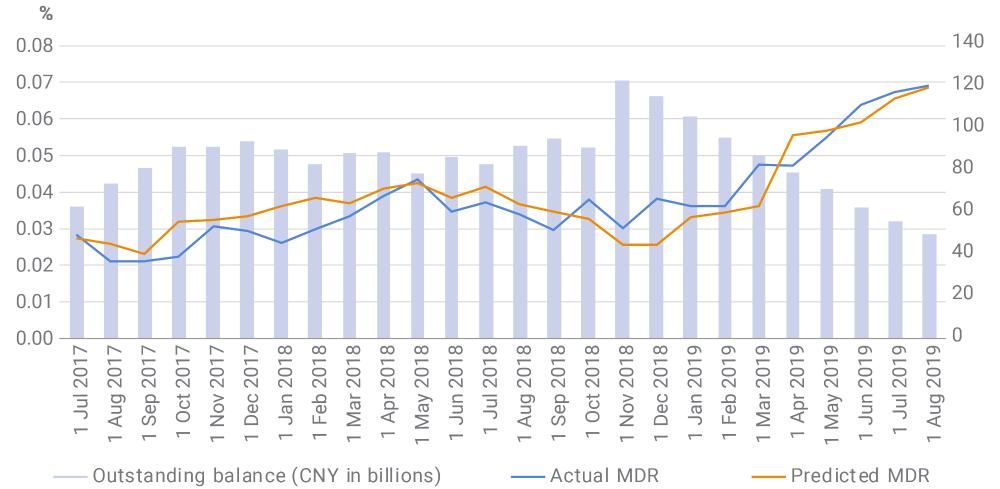

The monthly default rate (MDR) of Chinese auto ABS (for pre-2018 vintages) more than doubled (0.03% to 0.07%) from September 2018 to August 2019, as shown in the exhibit below. According to the National Bureau of Statistics of China, the third quarter's annualized GDP growth rate is 6.0% — the lowest number since 1992.5 This rapidly increasing default rate might be related, at least in part, to the ongoing economic slowdown.

Actual vs. predicted default rates for Chinese auto ABS

Source: CNABS, MSCI

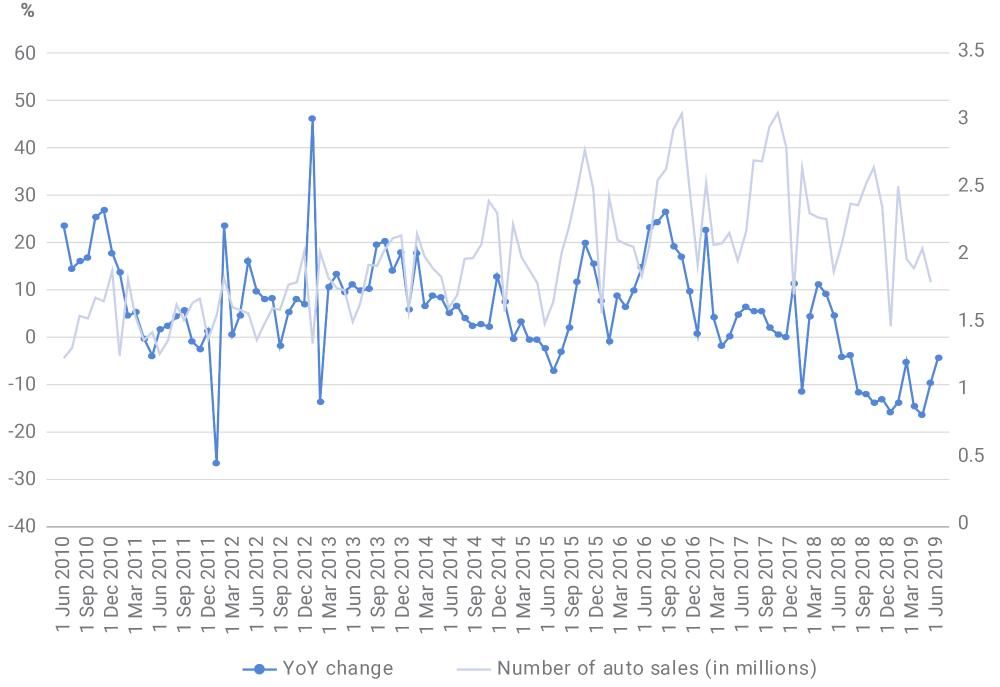

Borrowers' ability to pay, which is viewed as a key default driver, is generally proxied by the unemployment rate and credit tightness: MSCI's model for U.S. auto ABS draws on the unemployment rate, and on indexes for credit availability and used-car prices, to quantify this risk factor.6 In the Chinese market, however, credit-availability and car-price indexes don't yet exist, and the two official unemployment rates are not consistent, due to different survey methods.7 But auto-sales volume, which has declined year over year since September 2018,8 signals stress on the Chinese economy and consumer spending, which could further dampen GDP growth.

China's auto sales and year-over-year change

Source: Caixin, CEIC

What effect could looser personal-bankruptcy laws have on Chinese ABS?

Changes in personal-bankruptcy laws have historically affected borrowers' willingness to pay, another key default driver for consumer ABS. For example, the U.S. 2005 Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) made filing for Chapter 7 personal bankruptcy more difficult and encouraged the more stringent Chapter 13 filings. Before BAPCPA went into effect, there was a sharp increase in consumer bankruptcy filings, as people rushed into the more lenient Chapter 7 filings.9

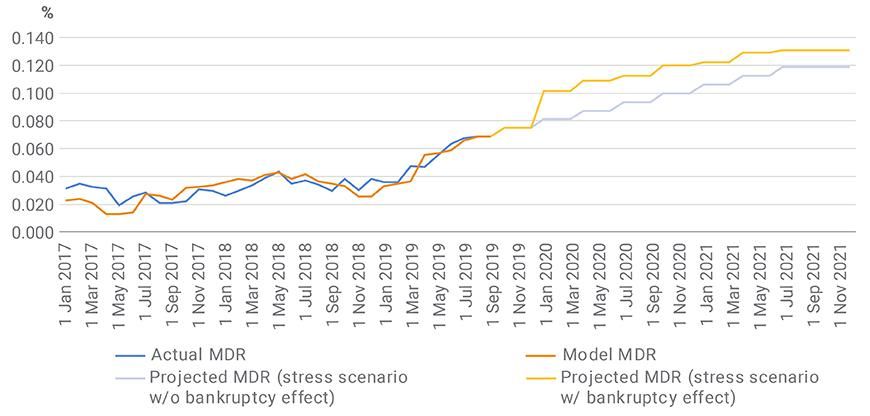

Similarly, if China's economic difficulty continues, default rates could move higher — and potentially accelerate if the bankruptcy regime generally becomes more borrower-friendly, as shown in the two scenarios in the exhibit below.

Predicted MDR under stress scenarios with (and without) bankruptcy law's effect

Source: CNABS, MSCI

Given the relatively conservative consumer credit culture in China, the effect of any change in bankruptcy law may be less severe than it was in the U.S. over the last decade. The exhibit above shows our model's projection of a 75% increase in default rates for a stress scenario in which GDP growth gradually declines to 4.4% over two years, combined with a hypothetical full implementation of a new Chinese consumer bankruptcy regime. In the scenario that leaves out the effect of a change in bankruptcy law, default rates will increase by 59%, according to our model.

In sum, Chinese ABS investors may wish to remain vigilant about consumer-loan default speeds — and consider the effects that potential changes in China's personal-bankruptcy laws may have on those default speeds.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Zhu, L. “Exploring personal bankruptcy: Wenzhou’s first settlement case.” , Oct. 10, 2019.2Wen, Q. and Shan, Y. “Individual Bankruptcy: Legislation to encourage entrepreneurship and fight against debt.” , Aug. 26, 2019.3Consumer bankruptcy is not addressed in the 2006 Enterprise Bankruptcy Law of the People’s Republic of China.4Chen, J. and Yang, Y. 2019. “MSCI China Auto Loan ABS Collateral Model.” MSCI Model Insight. Client access only.5He, L. “China’s economic growth drops to lowest level since 1992.” CNN, Oct. 18, 2019.6Yang, Y. and Zhang, J. 2019. “MSCI US Auto Loan Collateral Model.” MSCI Model Insight. Client access only.7The two unemployment rates currently available — the urban survey unemployment rate from the National Bureau of Statistics of China and urban registered unemployment rate from the Ministry of Human Resources and Social Security — moved in different directions during the period of our analysis.8“The decline of sales narrowed yearly.” China Association of Automobile Manufacturers, Oct. 16, 2019.9Sather, S.W. “The Great Bankruptcy Rush of 2005 and its Aftermath: The View from Texas.” American Bankruptcy Institute, Sept. 1, 2006.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.