A reality check for MBS duration risk

Blog post

August 15, 2019

- The U.S. bond-market rally and soaring volatility of mortgage-backed securities (MBS) over the last eight months have posed a steep challenge for risk managers to pin down MBS duration risk, due to prepayment uncertainty.

- Empirical duration data can be used for a reality check on whether MBS models are accurately measuring interest-rate risk.

- Both MSCI's agency prepayment model and empirical-duration data showed significant duration shortening since the end of last year, as MBS risk is now skewed more toward contraction risk.

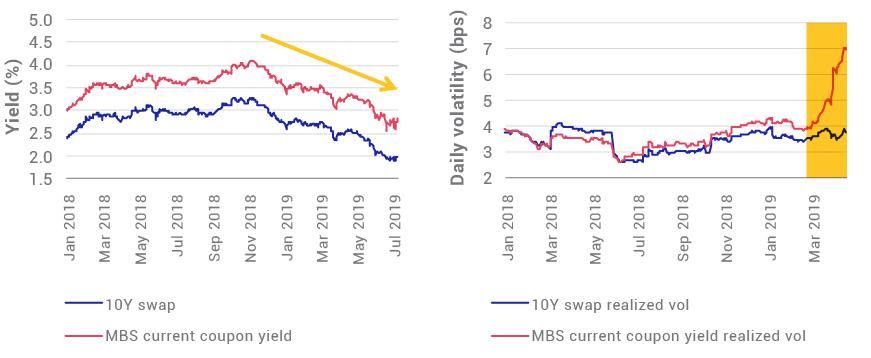

Amid market uncertainty, MBS rallied, swap volatility was flat and MBS yield volatility soared

As Fed reversed course, uncertainty abounded

The Federal Reserve began a series of rate hikes in 2016 and a round of quantitative tightening in 2017 — policies that extended MBS durations, as we discussed before. Partly over concerns about domestic economic growth and ongoing trade tensions, the Fed has since reversed these policies. The linkage between the U.S. and other advanced economies, which have much lower rates,2 also puts downward pressure on U.S. bond yields. As a result, rates have fallen dramatically in the U.S. since the end of 2018.

MBS durations then started to shorten significantly. Amid the high uncertainty over monetary policy and the direction of prepayment trends, volatility of MBS' current coupon yields spiked. Meanwhile, the widening gross-/net-coupon spread injected even more negative convexity into the to-be-announced (TBA) MBS market, causing more duration uncertainty.

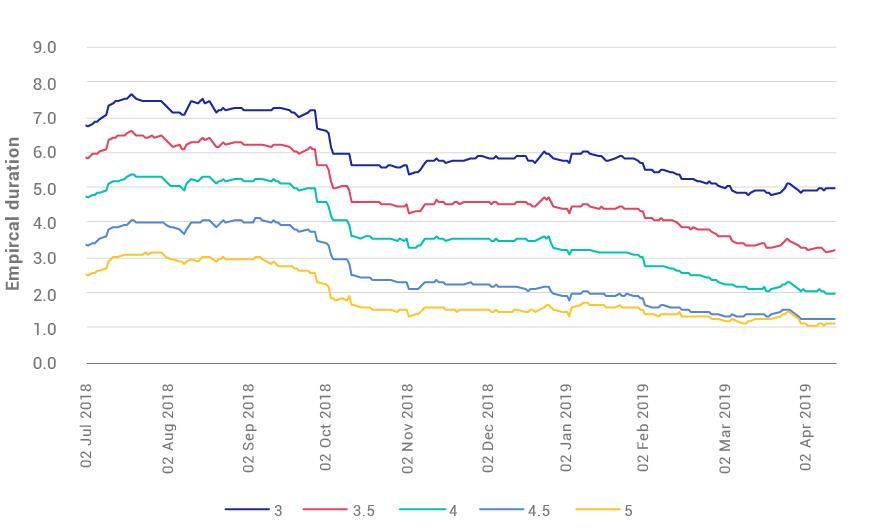

TBA MBS' empirical durations shortened significantly since the end of 2018

Rolling subsequent three-month empirical regression is performed for Fannie Mae's 30-year TBA, 3% to 5% coupons.

Looking backward to assess duration-model performance

Option-adjusted duration (OAD) is the measure of interest-rate risk that market participants commonly rely on. They are often modeled using Monte Carlo simulation with a prepayment model and a stochastic term-structure model for swap rates and mortgage rates. But OADs can differ greatly across models, due to differences in modeling assumptions and techniques. The recent soaring MBS market volatility has drastically increased this difference, posing a great challenge for risk management and hedging practices.

Empirically observed duration measures,3 on the other hand, are an ex-post data-driven measure. We can derive the empirical duration by regressing securities' historical price changes against changes in the rates of swaps and Treasurys. Retrospectively, a hedged portfolio constructed based on empirical duration statistically eliminated the interest-rate risk exposure for the security in question.4

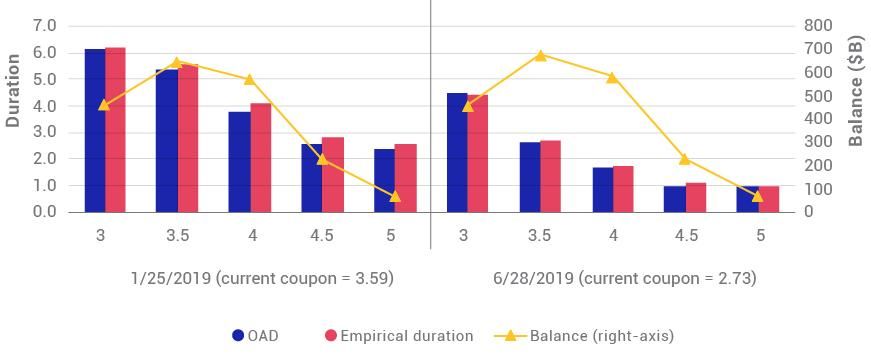

Checking the MSCI MBS model's OAD against ex-post empirical duration

Data is based on a Fannie Mae 30-year TBA, 3% to 5% coupons. Source: MSCI Agency Prepayment Model

The exhibit above demonstrated a reality check on the model OAD based on MSCI's agency prepayment model, against empirical duration. Both measures have shown significant duration shortening across coupon stack from the beginning of the year until now.

In summary, the recent rate rally, worsening negative convexity and soaring MBS volatility have pushed MBS durations significantly lower and increased uncertainty. But ex-post empirical duration has provided a powerful tool in model backtesting. MBS investors and risk managers may want to take a closer look at the risk profile of their portfolio, ensuring model-driven risk measures are in line with reality.

Further Reading

Getting Ahead of the Curve: How Taper 2.0 May Affect Bond Returns

Managing MBS risk in a rising rate environment (Part 1)

Managing MBS risk in a rising rate environment (Part 2)

Is MBS refinance risk increasing?

How mortgage fees affect rates and spreads

Are you ready for uniform MBS (Part 1)

Are you ready for uniform MBS (Part 2)

Subscribe todayto have insights delivered to your inbox.

1 Contraction risk is the risk that borrowers will speed up their principal repayment and diminish expected MBS returns. Extension risk is the risk borrowers may hold onto mortgages longer than previously expected.2 Davies, P. and Kowsmann, P. “Germany’s Longest Bond Goes Negative for First Time.” , Aug. 2, 2019.3 MBS duration measures can be divided into three categories: model-driven (e.g., OAD and Macaulay duration); market-implied (e.g., empirical duration, coupon-swap duration and option-implied duration); or market-consensus (e.g., hedge ratios).4 This report contains analysis of historical data, which may include hypothetical, backtested or simulated performance results. There are frequently material differences between backtested or simulated performance results and actual results subsequently achieved by any investment strategy. The analysis and observations in this report are limited solely to the period of the relevant historical data, backtest or simulation. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. Investors may wish to be cautious when using empirical duration as a forward measure: A more sophisticated algorithm is needed to include swaption volatility, moneyness adjustment, option-adjusted-spread directionality and other independent variables.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.