Apples vs. Oranges? Core vs. Opportunistic Real Estate Funds

Blog post

October 25, 2018

Real estate investors sometimes treat core and opportunistic funds as if they were different asset classes. They are measured against different benchmarks and comparisons are limited by a lack of consistent data. But a comparison of the two shows that both core and opportunistic funds have similar return profiles — it's the magnitude of their returns that has varied over time.

FROM CORE TO OPPORTUNISTIC

Core funds are primarily invested in stabilized, income-producing assets. The majority of returns are expected to be generated from income rather than capital growth with limited leverage employed. These funds tend to be open-ended, requiring regular valuations to facilitate potential redemptions.

As investors move up the risk spectrum, funds tend to become increasingly exposed to leasing and development risk and have increased leverage. With these riskier funds, a greater proportion of returns are expected to come from capital appreciation. As these investments require a multi-year business plan, the fund structure tends to be closed-ended with capital locked up for the life of the fund. From an operational standpoint, regular valuations are not a common requirement.

BENCHMARKING DIFFERENCES

Core funds are often measured against a relative market benchmark using time-weighted total returns based on regular valuations. This yardstick enables investors to understand the extent to which a portfolio is driven by market risk versus specific risk factors. Moreover, such measurements enable investors to better understand how the real estate portfolio is correlated with the total portfolio.

In contrast, closed-ended, opportunistic funds tend to be evaluated in absolute terms against a fixed-return hurdle over the life of a fund. Returns are measured on an internal rate of return (IRR) basis. Because risk is viewed as more property-specific than related to the real estate market as a whole, correlation analysis is viewed as less relevant. But is this perception justified?

COMPARING LIKE TO LIKE

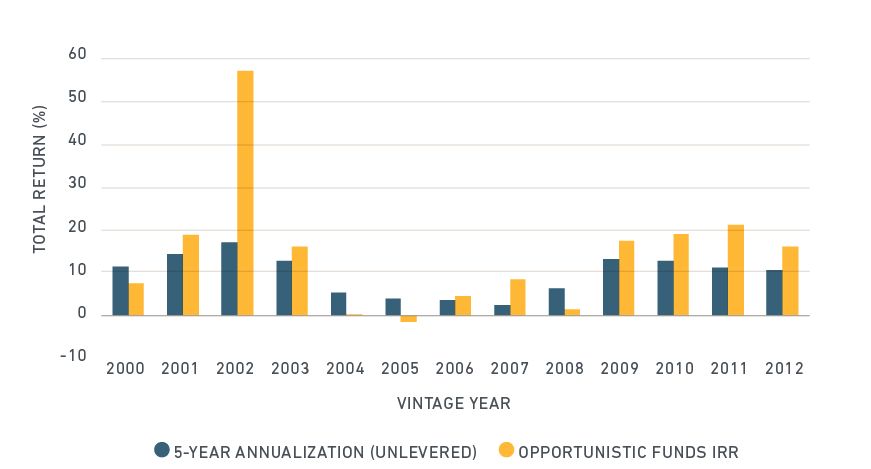

A comparable analysis between core and opportunistic funds is currently limited by a lack of consistent data. The exhibit below compares unlevered asset performance from core open-ended funds in the MSCI database with opportunistic fund performance from Preqin Ltd. The MSCI time-series shows the forward 5-year total return compound annual growth rate (CAGR) at each point in time. The Preqin data shows the realized IRR1 of opportunistic funds by vintage.2

APPLES AND ORANGES?

Source: MSCI Global Intel PLUS (unlevered returns) and Preqin Ltd (opportunistic funds). The 2002 vintage Preqin data is skewed by the performance of one fund with an IRR in excess of 200%. The median IRR for this vintage was 18.8%.

AIMING FOR CONSISTENCY

Although the data is not precisely comparable,3 the analysis illustrates at a very basic level, that both types of real estate risk profiles appeared to follow similar cyclical trends between the vintage years 2000 through to 2012. By improving the sophistication and consistency of risk analysis across the entire spectrum of their holdings, real estate investors may be able to gain valuable insights using relative market analysis for opportunistic strategies.

1 Realized IRR from Preqin is for U.S. opportunistic real estate funds

2 IRR is based on vintage years in which the first capital is called from limited partners for investment.

3 We compare IRR with time-weighted return CAGR. The MSCI data refers to US All Property Types over a fixed 5-year measurement period versus an indeterminate fund life in the Preqin data. MSCI data refers to unlevered asset level performance versus fund level returns in the Preqin data.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.