Are convertible bonds more like equities?

Blog post

March 2, 2017

Convertible bonds have "bonds" in their name but in reality they are complicated corporate securities with risk characteristics that often have little to do with straight bonds. Are they more like stocks or bonds? And how can investors evaluate and model them?

In today's convertible bond market, the key driver of returns relates to the value of the underlying equity. In contrast, bond market exposure (in the form of yield curve and spread risk) has played a relatively minor role in driving convertible bond risk and return in the recent past and seems likely to play a minor role in the year ahead, based on our model.

Drivers of return historically

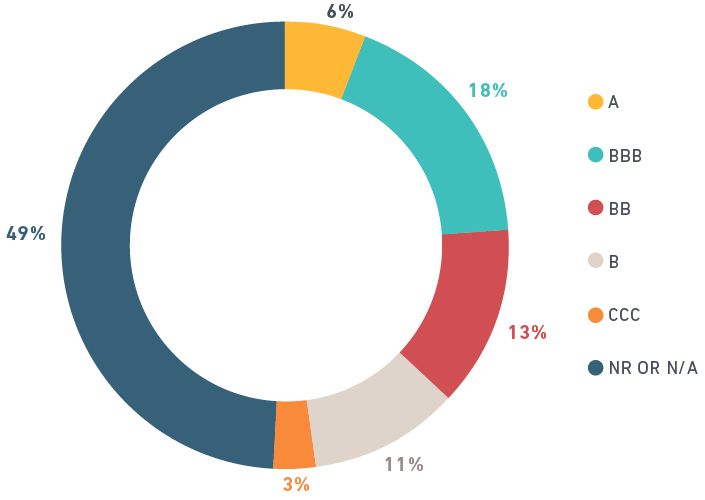

Convertible bonds are hybrid securities sold to investors who want to enjoy the upside of equities while still benefiting from the downside protection of bonds. A common feature of convertibles is that they can be converted into equities at the bondholder's discretion. Gergely Szalka of MSCI's Valuation Research Group and I studied all U.S. convertible bonds outstanding over the two-year period ending December 31, 2016 for which the MSCI database had a rating from Standard & Poor's¹ and a continuous price history.² About 37% of the 129 convertible bonds surveyed were rated below investment grade. Information Technology constituted the largest sector.³

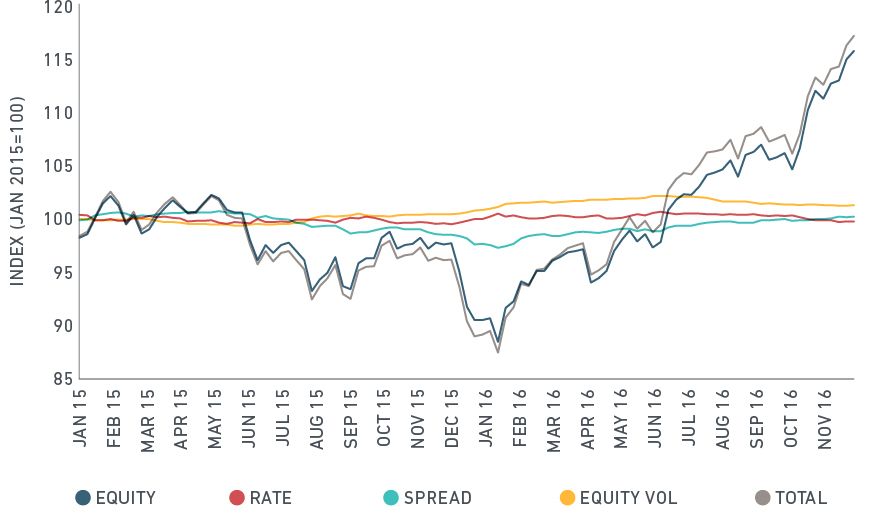

Looking over the two-year period, we see that realized price returns have been driven almost exclusively by changes in equity prices (below chart). In the 13 months through January 2016, bond prices in the sample fell 11% on average, which corresponds to a falloff of 6% in prices in the U.S. equity market. Since then, returns of convertibles have rebounded as U.S. equities have climbed.

Convertible Bonds

Cumulative Price Return

Looking ahead

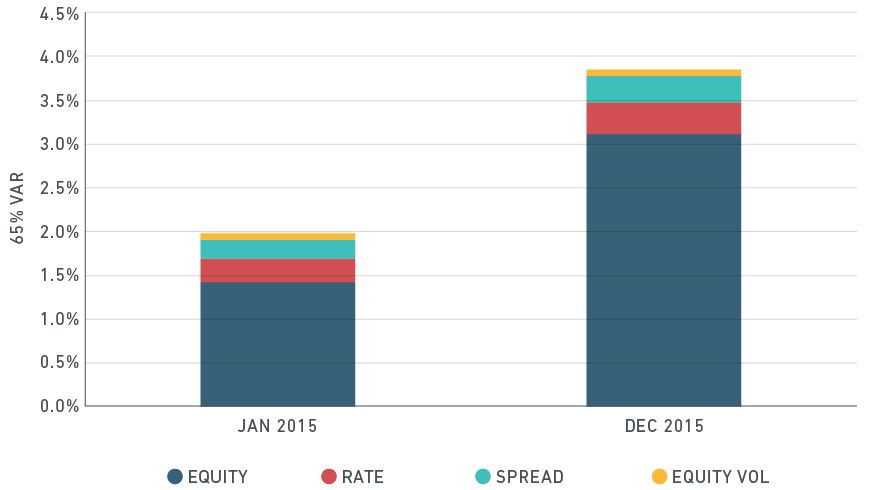

We use MSCI's recently updated model for convertibles to assess likely sources of risk over the next year. We first backtest the model to examine how well it predicted actual past returns. Our measure of ex-ante risk is 65% Value at Risk (VaR). As confirmed in the next chart, our model correctly identified equity risk as being the likely primary driver of returns for both 2015 and 2016.

Forecasted 1-Year Risk

(as of Jan. 2015 and Dec. 2015)

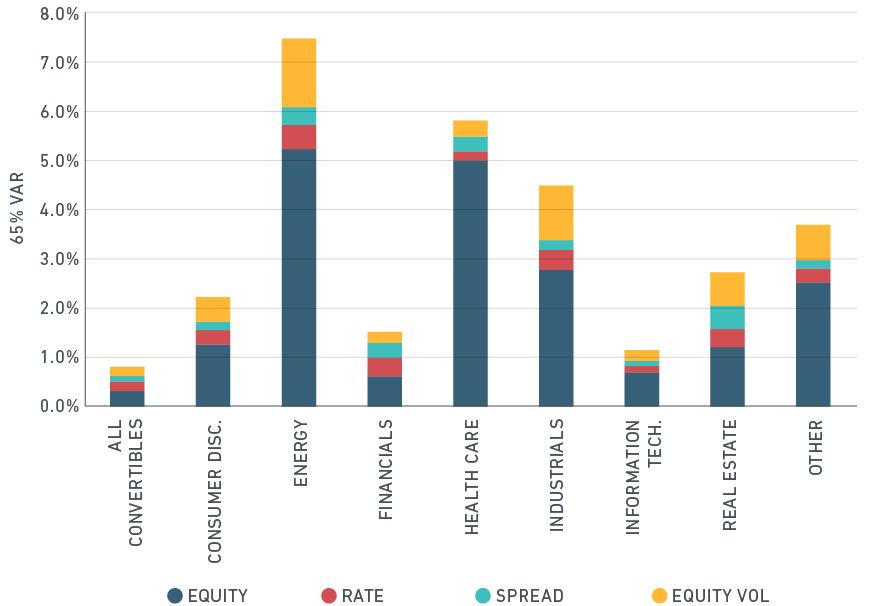

We now look at U.S. convertible bonds outstanding as of January 31, 2017. This is a much larger sample of 577 bonds than was used for the historical analysis and includes many unrated bonds. Across sectors, we see that equity risk is projected to be the primary driver of returns (below chart). Two exceptions include the Financials and Real Estate sectors where bond factors are projected to play a more significant role. The sectors with the highest projected risk are Energy and Health Care.

Forecasted 1-Year Risk

(as of Jan. 31, 2017)

Convertible bonds: Creditworthiness and sector distribution

(as of Jan 31, 2017)

Ratings Distribution

The model matters

In the aggregate, our analysis indicates that convertible bonds currently share many more risk characteristics with equities than with fixed income. But our results for the Financials and Real Estate sectors highlight the potential for fixed income exposures also playing an important role. Ultimately there is no substitute for having a model that can identify with precision the factors likely to be drivers of future returns.

The authors thank Aniko Maraz for her assistance in preparing this note.

¹Standard & Poor's Financial Services LLC (together with its affiliates, "S&P")

²Thomson Reuter's EJV Fixed Income

³GICS®, the global industry classification standard jointly developed by MSCI and Standard & Poor's

Further Reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.