Are you Ready for China A shares?

Blog post

June 29, 2017

MSCI's recent announcement that it will add 222 China A shares to its key benchmarks raises practical questions for global and emerging market investors: How does it affect their investment policy? How can they implement these exposures (whether or not they already have China A shares in their portfolios)? While inclusion of China A shares is a year away, institutional investors may want to start planning for how this change may affect their portfolios.

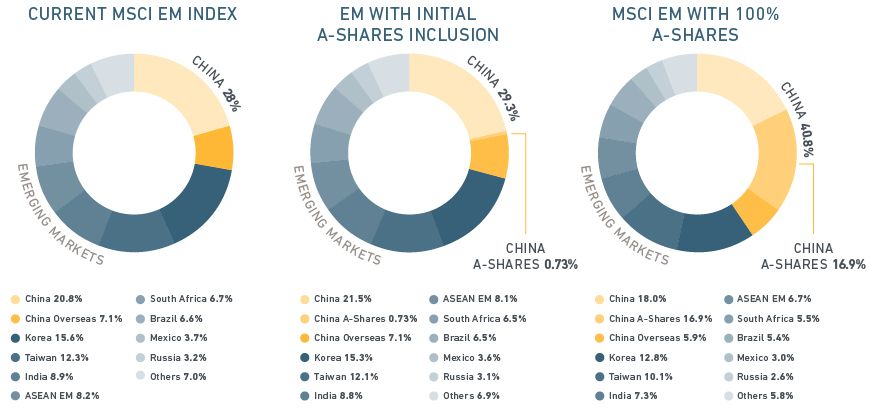

Longer term, if China continues to liberalize the A shares market and MSCI were to fully include them, China's weight in the MSCI Emerging Markets Index could rise to 40.8% from 28% currently, as we see in the exhibit below.

China A shares Index Weight

Based on data as of June 19, 2017

How to respond to A shares benchmark inclusion may depend on whether investors already have exposure to A shares. For global institutional investors without current A shares exposure, the key is to address their policy allocation to emerging markets, including China. Such a reevaluation can help reflect their long-term risk and return preferences more accurately.

Global institutional investors who already have an off-benchmark allocation to China A shares face potential benchmark misalignment with their existing A shares allocations. In addition, they may want to consider whether to retain or switch their A shares specialist allocation to a generalist emerging market or global manager. In this process, China A shares specialist managers may have an advantage because of their longer track records and because not all emerging market and global managers may be ready to manage China A shares.

The challenge for A shares specialist managers, however, will be to demonstrate that their investment processes are aligned with investor beliefs and that they can demonstrate stability and persistency in performance. While generalist managers may have less experience investing in China A shares, they may be able to point to better conformity with asset owner beliefs and benchmarks, and less volatility in their ability to deliver excess returns over time.

With or without a current A shares exposure, global institutional investors may want to examine how ready their current emerging market and global equity managers are to handle the inclusion of A shares in their benchmarks. In particular, it helps to understand if managers have a clear insight on the pros and cons of different access paths, sources of risk and return (including differing sector compositions), macro drivers, the premium or discount between A shares and H shares, style factors and other idiosyncratic drivers of China A stocks.

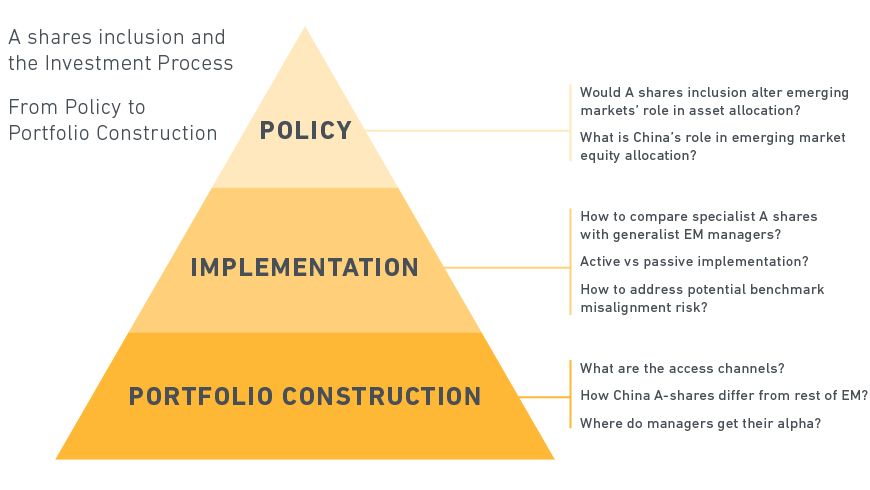

A shares Inclusion: A framework for institutional investors

The author thanks Chin Ping Chia for his contributions to this post.

Further reading:

Are You Ready for China A Shares? Implications of Including A Shares in Benchmark Indexes

2017 Country Classification Review Results

China A-shares: Too Big to Ignore

A look at MSCI's Emerging Market Index and China A-shares

Built to Last: Two Decades of Wisdom on Emerging Markets Allocations

Emerging Markets: a 20-Year Perspective

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.