Bank Loans: Will Crisis Follow the Search for Yield?

Blog post

June 27, 2019

- In the post-2008 search for yield, investors have taken on considerable exposure to leveraged bank loans. We assess whether these loans pose systemic risk in the way subprime mortgages did during the last crisis.

- One key difference with the crisis-era subprime market is the leveraged-loan market experienced substantial market turbulence in the fourth quarter of 2018 — and recovered.

- Our analysis considers a potential drop in recovery rates, the preponderance of cov-lite issues and changing prepayment speeds. We find that fears about the bank-loan market may be overblown.

A rapidly expanded market

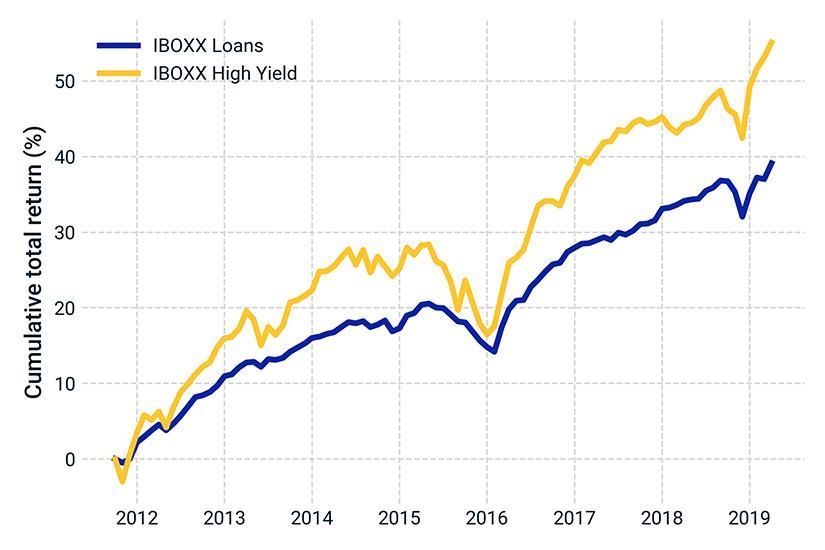

The leveraged-loan market now rivals the high-yield-bond market in notional outstanding value,2 buoyed by investor demand, a record-long economic expansion and a formerly rising-rate environment that boosted the yield on these loans. Whether the attractiveness of the asset class, and the pace of loan growth, can be sustained in a potentially declining-rate environment beset by recessionary anxiety is unclear.

Leveraged loans and high-yield bonds through the expansion

U.S. high-yield bonds represented by IHS Markit's iBoxx USD Liquid High-Yield Index; U.S. leveraged loans represented by IHS Markit's iBoxx USD Liquid Leveraged Loan Index.

Experience matters

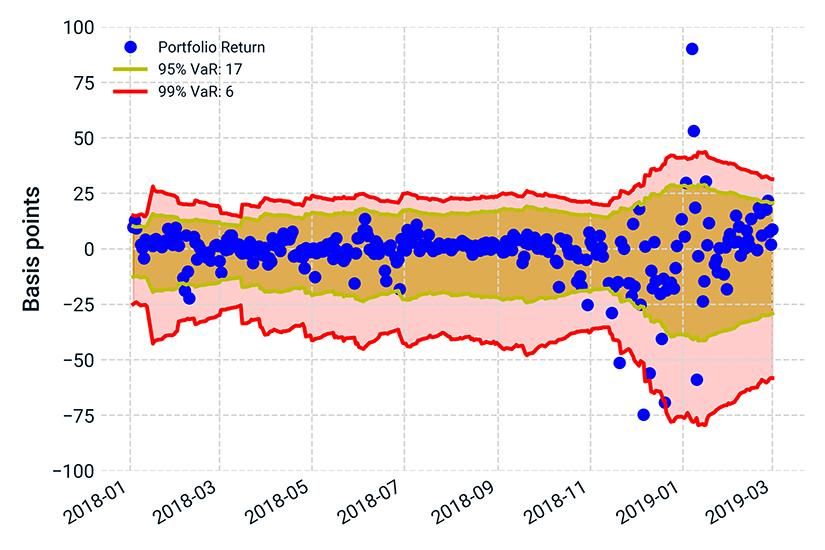

The fourth quarter of 2018 provided a real-world stress test of the leveraged-loan market — and of the RiskManager VaR model itself. The exhibit below illustrates how VaR measures responded to the substantial sell-off and subsequent rally. Note that the model's dynamics mirror the market turbulence and that the VaR violations for both the 95th and 99th percentiles are within the bounds of statistical confidence. One key difference with the crisis-era subprime market is the leveraged-loan market has experienced — and weathered — this sort of substantial market turbulence.

Q4 market turbulence and recovery showed the robustness of the asset class and model

U.S. leveraged loans are represented by IHS Markit's iBoxx USD Liquid Leveraged Loan Index. VaR backtest estimated in RiskManager using the MSCI Leveraged Loans model.

Effect of recovery rates on losses

One possible scenario that could undermine the market, according to our testing, is a drop in recovery rates — i.e., the rate at which investors recover principal and interest in the event of a borrower company's bankruptcy or default — following the next cyclical rise in corporate defaults.3 Some market participants may be contemplating a scenario in which recovery rates depart drastically from historical averages — for second-lien term loans, in particular. By stress testing recovery rates, and evaluating a range of recovery scenarios, investors can gain a fuller picture of the distribution of their potential losses.

Cov-lite can still taste great

Another scenario considers the resilience of a loan market so densely composed of so-called covenant-lite paper. This scenario, unlike the former, has attracted a great deal of regulatory interest.4 We've previously explored how cov-lite loans might react to a backup in spreads and found their losses could be magnified relative to their more strongly covenanted counterparts.

It's important to note, however, that cov-lite paper's increasing share of the loan market reflects a new investor-issuer dynamic: Before, when loan issues often had only one investor (usually a bank), including strict covenants was cheaper and easier, because the investor could monitor the issuer directly. But as the market has grown and each asset now tends to have multiple investors (frequently nonbanks), it became too costly for the investors to monitor the issue.5 Despite agreeing to weaker covenants, the new investor base represents a much more stable funding source than the crisis-era banks that held subprime mortgages; as a result, the market may be more resilient than it seems.

Slower prepayment speeds, fewer originations

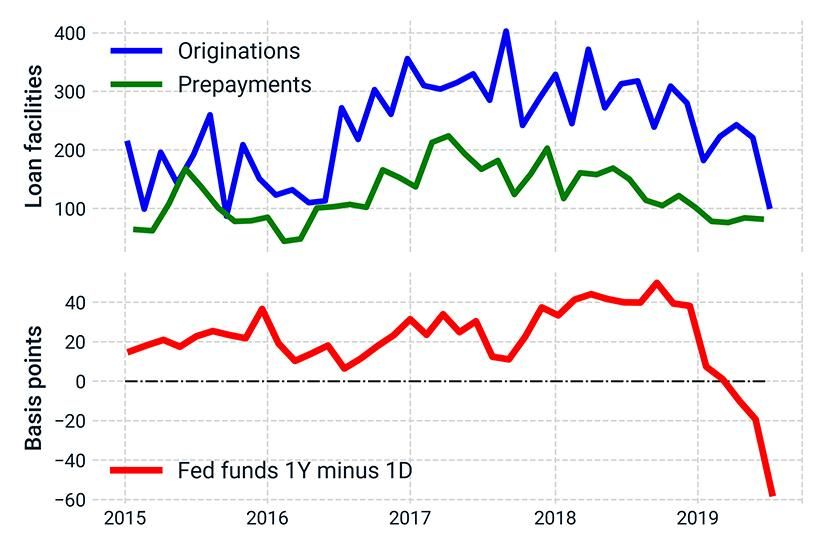

Finally, in the past year, prepayment speeds for the broad market have moderated from the prior year. Both prepayments and originations contracted substantially at the end of 2018 and beginning of 2019. The exhibit below illustrates these trends.

The bottom panel is a market-based forecast of monetary policy. A positive slope for the fed-funds rate's swap curve suggests the market expects rates to rise in the future and vice versa. The end of 2018 led to a rapid decline in expectations for future rate increases, so much so that the market appears to believe there will be a rate cut within a year. It remains to be seen whether the expansion and performance of the loan market can continue if the floating-rate advantage reverses (i.e., when rates go down).

The paths of leveraged loans and rates

Source: IHS Markit. The bottom panel is a measure of the expected path of monetary policy, while the top panel illustrates the number of facilities prepaid and originated in the leveraged-loan market. Market participants are concerned that the recent dovish turn by the Federal Reserve will undermine the attractiveness of floating-rate loans relative to fixed-rate high-yield bonds.

The end of the search for yield?

The post-crisis market environment has been defined by the search for yield, so the appeal and rise of leveraged lending should come as no surprise to market participants. But this rising market is also a very different market from before: While displaying strength, it contains new and more subtle risks. Investors are left to decide whether loan yields offer adequate compensation for those risks.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Chappatta, B. “Leveraged Loan Lovefest Will End in Heartbreak.” Bloomberg, Aug. 22, 2018.2 “It’s Official: US Leveraged Loans are a $1 Trillion Market.” S&P Global Market Intelligence. April 30, 2018.3 Op. cit. “Leveraged Loan Lovefest Will End in Heartbreak.4 See, for example: “Semiannual Risk Perspective.” Office of the Comptroller of the Currency, Dec. 3, 2018.5 Becker, B. and Ivashina, V. “Covenant-light Contracts and Creditor Coordination.” Swedish House of Finance, March 2016.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.