Bond ETFs and underlying price uncertainty

Blog post

April 8, 2020

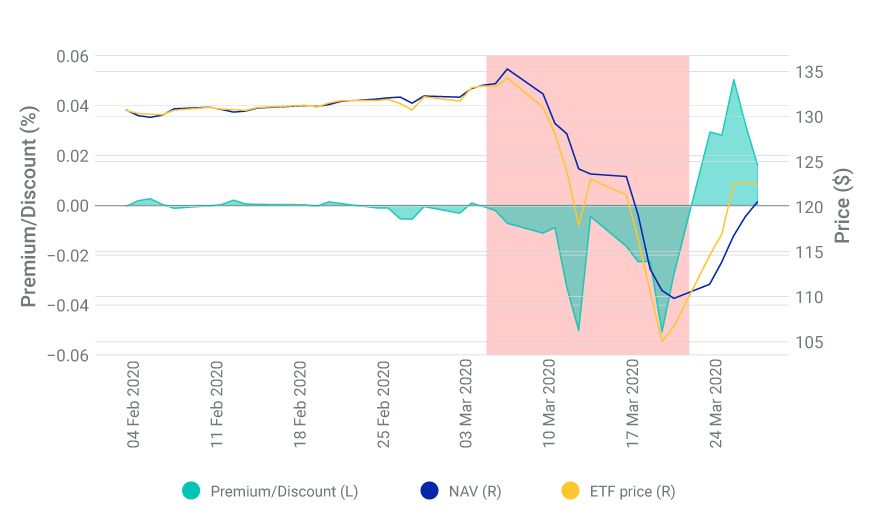

- The recent market meltdown put pressure on bond ETFs. At their March lows, several major investment-grade bond indexes had fallen by more than 15%, while the ETFs tracking them occasionally traded at price discounts to net asset values as high as 6%.1

- Investors may worry that ETF prices can deviate from the value of the underlying basket during market stress, potentially leaving them exposed to NAV losses on top of the falling bond prices.

- A bond ETF's price/NAV dislocation may have been caused by an inaccurate NAV due to weakening liquidity in the investment-grade bond market. But the more likely reason was price uncertainty — not low volume or trading frequency.

Bond ETFs' recent price-NAV divergence

Data compiled on iShares iBoxx $ Investment Grade Corporate Bond ETF Source: Refinitiv Lipper

Price transparency may not explain all

In a market with significant price transparency, an ETF's price on the exchange should generally approximate the value of the underlying bond basket — i.e., its NAV. If the two significantly deviate, designated market makers known as authorized participants (APs) may step in to close the gap, by creating or redeeming baskets of securities in exchange for ETF shares.

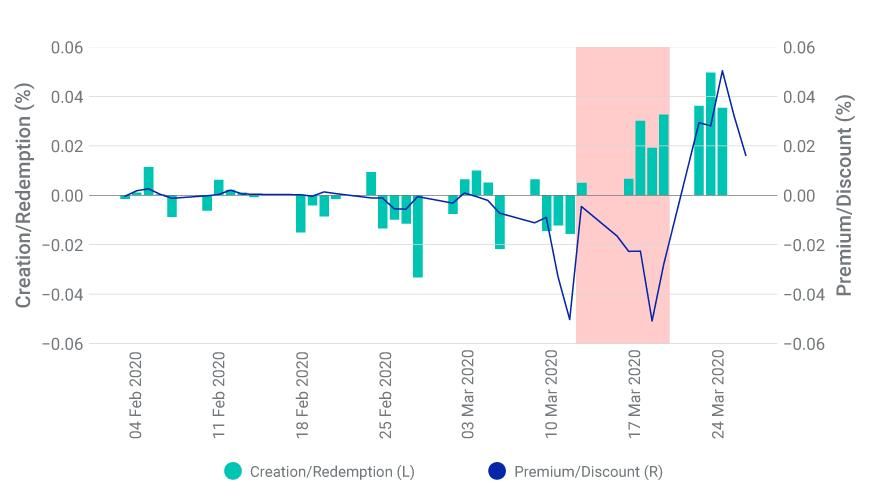

The large dislocations (both positive and negative) observed from March 10 to March 31 may mean that this arbitrage mechanism might have temporarily faltered. Alternatively, the NAV price may not always be a precise measure of the value of the ETF's underlying constituents. For example, we observed there was net creation of iShares iBoxx $ Investment Grade Corporate Bond ETF shares between March 13 and 20. Yet on these dates, the NAV was significantly above the exchange price. The ETF creations on these days suggested that APs were able to source the underlying bonds more cheaply than indicated by the published NAV.

Investment-grade ETF's net creation/redemption vs. premia/discounts

Data compiled on the iShares iBoxx $ Investment Grade Corporate Bond ETF. Source: Refinitiv Lipper

NAV inaccuracy?

It is possible that an ETF's price may at times better reflect the value of the basket than the NAV. In turbulent times, for example, the ETF's trading volume may rise relative to the trading of the individual bonds.3 In this way, the ETF could be a major source of price discovery in the corporate-bond market. But why might the NAV occasionally be inaccurate?

One possible reason is that the underlying bond prices may be stale, sometimes not trading on days when the NAV is calculated. To investigate this possibility, we looked at the time of the last trade before 5:00 p.m. for all bonds held by the iShares investment-grade ETF on March 19, the date with the highest observed discount.

We found that more than 92% of the underlying bonds did trade, and 74% of them had an observable traded price as close as two hours to the close of the market. We found similar percentages throughout January and February 2020. Our analysis, therefore, indicated that significant deviations between an ETF's exchange price and the NAV may exist even when there is trading activity in most of the underlying constituents.

Could price uncertainty explain the anomaly?

An alternative explanation is that a traded price is simply one estimate of a bond's value across the range of active market participants. Market-induced uncertainty among market participants about the value of a bond could lead to a significant dispersion of traded prices for that bond — even on a single day. Market uncertainty may then result in the NAV's deviating significantly above or below the ETF's price on the exchange.

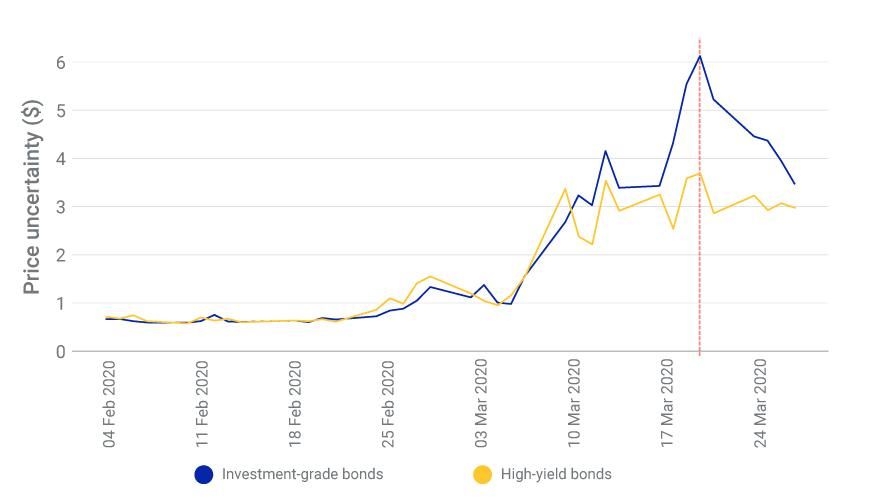

To understand recent price uncertainty in the corporate-bond market, we looked at the daily average price dispersion of constituent bonds of the iShares iBoxx $ Investment Grade Corporate Bond ETF and of the iShares iBoxx $ High Yield Corporate Bond ETF.

For both of these ETFs, our price-uncertainty measure significantly increased over the past two months and peaked on March 19, as shown in the exhibit below.4 On this day, the price-to-NAV discount for the investment-grade ETF was higher, at over 5%. In contrast, price uncertainty was significantly lower for the high-yield ETF, and it traded at a much smaller premium to NAV (0.85%). The lower observed price uncertainty of the high-yield ETF might partly explain why its NAV was closer to its price on the exchange.

Price uncertainty of high-yield vs. investment-grade bonds during sell-off

Source: IHS Markit, MSCI

Price discounts may not reflect underlying fundamentals

In short, fixed-income ETFs' price/NAV discounts may have sometimes reflected uncertainty in the underlying bond prices, rather than a fundamental difference between the values of the ETF and its underlying basket of bonds.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The Markit iBoxx USD Liquid Investment Grade Index fell by 18.9% (from March 6 to 26), and the iShares iBoxx $ Investment Grade Corporate Bond ETF tracking it traded at a 5.08% discount on March 19. The two major total-bond-market ETFs, iShares Core U.S. Aggregate Bond ETF and Vanguard Total Bond Market ETF, traded with 4.4% and 6.2% discounts, respectively.2The cost of the forced selling of USD 10 million of a bond more than tripled in March 2020. “MSCI Liquidity Risk Monitor Special Report.” MSCI, March 31, 2020.3The daily trading volume of the iShares iBoxx $ Investment Grade Corporate Bond ETF more than doubled in March 2020, while trading volume (as reported by TRACE) increased by only around 30% for the constituent bonds.4Price uncertainty is measured as the difference between the maximum and minimum observed traded price on the same day.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.