Bonds and Equities: Still Happy Together?

Blog post

June 25, 2018

For many years now, stock and bond returns have consistently moved in opposite directions. But the timing of selloffs earlier this year in the bond and equity markets combined with inflation concerns and higher interest rates have market participants asking whether the relationship has changed.1 Rather than returns being negatively correlated (when stock prices come down, bond prices go up), it seems possible they may now move in the same direction. If true, bonds would be less useful as protection against equity tail risk. Investors accustomed to bonds anchoring their portfolios during stormy equity markets may seek to reevaluate their portfolio strategies.

Our view is that these concerns are overblown. And even if the correlation has increased, volatilities are also important. We find that the increase in risk on a common 60/40 investment strategy from a rise in correlations would likely be modest without an increase in bond volatility.2

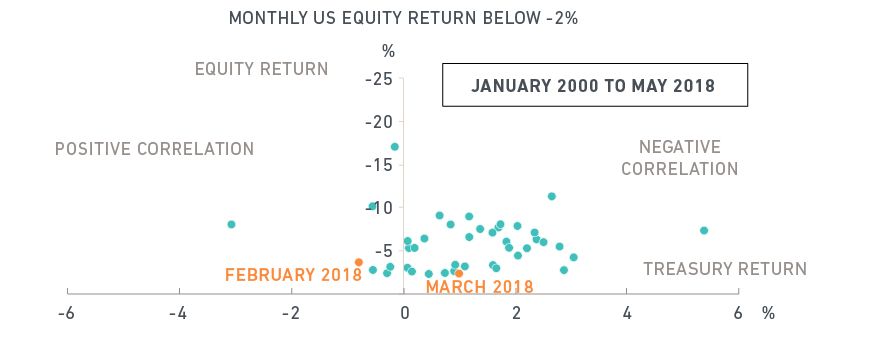

ONE MONTH DOES NOT REFLECT A TREND

February's selloff in both the equity and bond markets fueled concern that the correlation may have changed. While stocks continued to sell off in March, U.S. Treasurys rallied strongly. And then there's the deeper historical evidence. Since 2000, we find that significant downdraughts (declines of 2% or greater) in equities were consistently (about 84% of the time) accompanied by positive returns in the U.S. Treasury market, as we show in the exhibit below.3

When stocks have declined sharply, bonds usually have gone up

Source: Treasury returns are from the ICE BofAML US Treasury Index (G0Q0), used with permission. Equity returns are from the MSCI USA Index.

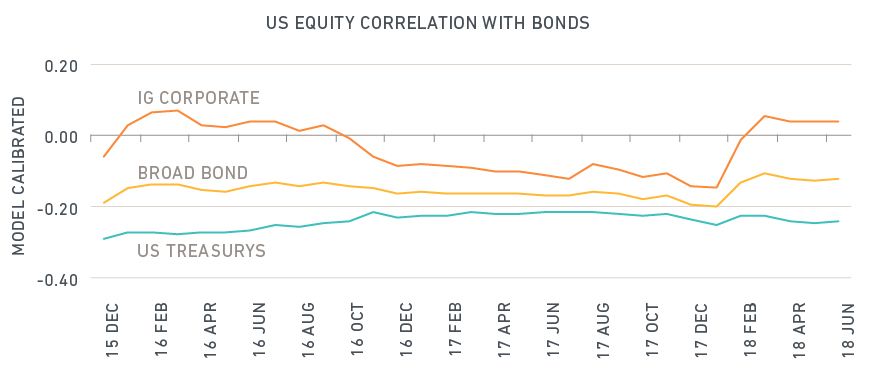

There are some differences in correlation trends across different sectors of the bond market. Our model-estimated correlation between equities and U.S. Treasurys has moved within a narrow band over the past several years; it stands at -.24 as of this writing. We interpret this as strong evidence that concerns about rising inflation and the recent increase in interest rates have not yet affected the bond-equity correlation. A broader measure of the U.S. bond market — including governments, corporates and mortgage-backed securities — showed a small increase in the correlation but it continued to be negative (at -.12). An increase in the correlation of equities and corporate bonds drove this change as corporate spread volatility rose and spreads widened during the equity selloff.

Correlation between equities and bonds has remained relatively constant

Source: Bond market sectors are represented by ICE BofAML indexes, used with permission: US Treasury Index (G0Q0), US Corporate Index (C0A0), and the ICE BofAML US Corporate, Government & Mortgage Index (D0A0). The U.S. equity market is represented by the MSCI USA Index. Our analysis uses the short version of the MSCI Integrated Model (MIM.s) for estimated correlations.

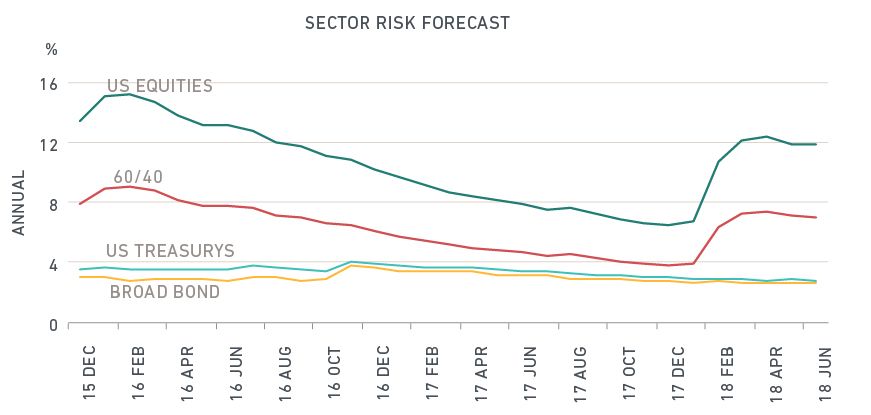

We find that equity volatility still dominates as the primary driver of risk for the widely employed investment strategy of 60% equities and 40% bonds. Almost all of the recent increase in forecasted risk for a 60/40 portfolio — from 4% as of Jan. 31 to 7.1% as of June 14, 2018 — can be attributed to the significant spike in equity volatility (from 6.7% to 11.8%).

EQUITIES ARE PRIMARY DRIVERS OF FORECASTED VOLATILITY FOR A 60/40 PORTFOLIO

Source: Bond market sectors are represented by ICE BofAML indexes, used with permission: US Treasury Index (G0Q0), US Corporate Index (C0A0), and the ICE BofAML US Corporate, Government & Mortgage Index (D0A0). The U.S. equity market is represented by the MSCI USA Index. Our analysis uses the short version of the MSCI Integrated Model (MIM.s) for forecasted risk.

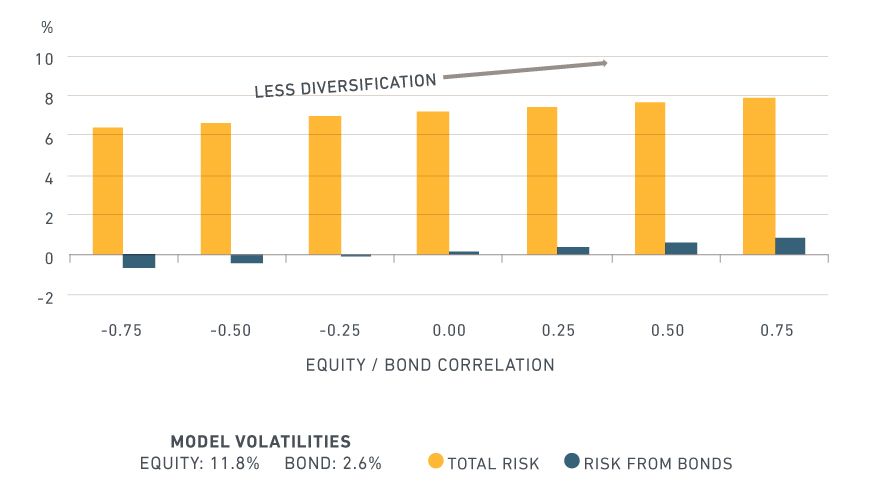

What if we are wrong, and the future correlation turns out to be much higher than that expected by our model? Even then, we estimate that portfolio risk would rise only modestly. For example, our risk forecast would increase to only 7.7% from 7.1% now if the bond-equity correlation increased to .50. Why would there be only a relatively small increase? Because current bond market volatility is much lower than equity volatility (2.6% versus 11.8%, respectively). Bonds indeed still act as an anchor to the portfolio: The low volatility in bonds dampens the impact of a change in correlations on portfolio volatility.

Risk forecast for 60/40 portfolio of equities and bonds

Source: The bond market is represented by the ICE BofAML US Corporate, Government & Mortgage Index (D0A0), used with permission. The U.S. equity market is represented by the MSCI USA Index. Our analysis uses the short version of the MSCI Integrated Model (MIM.s) for forecasted risk.

The impact on portfolio risk would have been greater if bond market volatility had also increased. Stated otherwise, the better question to ask is whether volatility in the bond market may significantly pick up at the same time that the bond-equity correlation increases. How might this happen? One plausible scenario: if U.S. inflation (currently near 2%) rose significantly above the Fed's target of 2%, the Fed might then be forced to more aggressively tighten monetary policy. The result could be a selloff in equities at the same time that inflation causes bond returns to fall and exhibit greater volatility.

The author thanks Juan Sampieri and Aniko Maraz for their contributions to this post.

1 See "New correlations spell concern for bond and equity investors." Financial Times, April 30, 2018.

2 Other types of strategies including risk parity may be much more impacted

3 The earlier history from 1977-2000 shows the correlation was generally positive. Important structural changes have occurred since then which may have influenced the correlation. Examples include a U.S. economy more insulated from oil shocks and a lower and more stable rate of inflation.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.