Can Alpha be Captured by Risk Premia?

Blog post

June 16, 2015

Traditional investment thinking posits that alpha depends on the active decisions of portfolio managers. The search for alpha is daunting, however, because even the best analysis can be upended if the market draws a different conclusion. In addition, geopolitical and macroeconomic events can change the market environment without warning.

As a result, the cost of looking for alpha is predictable, but the results of the search are not. Most active managers have not achieved outperformance, and studies show that the outperformance of successful managers has lasted an average of just 36 months.

A study published in The Journal of Portfolio Management examines a two-prong approach that some institutional investors now use to capture alpha. In an example that allocates 30% of the equity portfolio to two risk premia and 70% to top-performing active managers, we showed that this sample portfolio would have produced superior performance while reducing costs. (Risk-premia refers to the potential benefit associated with exposure to systematic risk factors that explain securities' performance. Value, size and momentum are among the widely recognized factors for equities.)

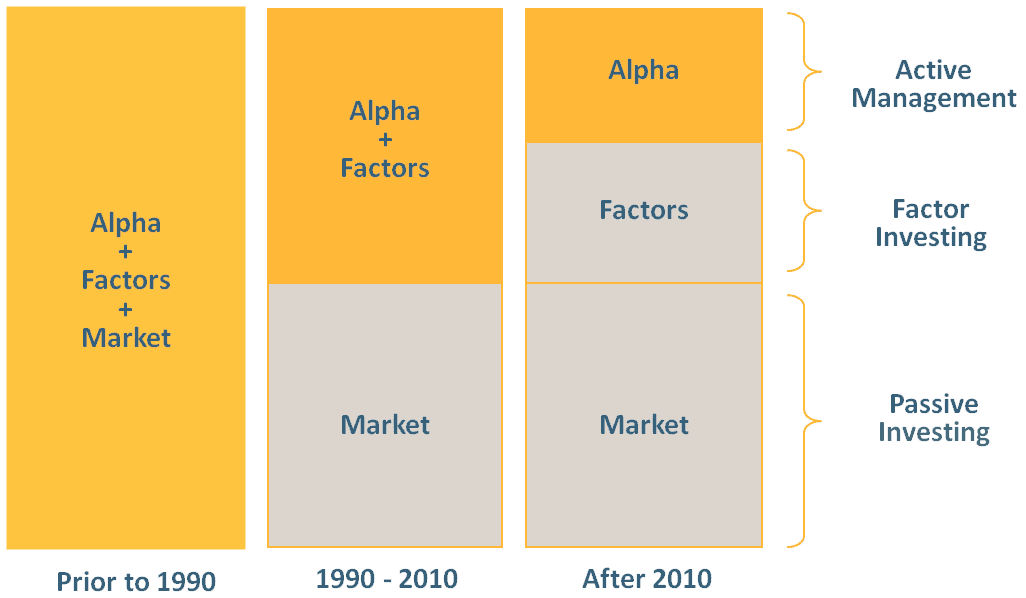

The Rise of Factor Investing

How consistently did exposure to risk-premia boost returns? For the period June 1988 to March 2012, the Risk Weighted, Minimum Volatility, Equal Weighted and Value Weighted indexes — all of which are drawn from the MSCI World Index — each outpaced the parent index and provided higher Sharpe ratios.

Using data from eVestment, the study compared the returns of 1,450 managers (representing a mix of core, value and growth portfolios), during a more recent period: January 2002 to March 2012. It found that the median manager's excess return before expenses was 110 basis points per year.

During that decade, the excess returns of the MSCI Risk Weighted and Equal Weighted indexes exceeded that of the median manager. The Minimum Volatility Index was slightly lower; only the Value Weighted Index lagged significantly. Furthermore, those managers who consistently outperformed their peers showed greater correlation with the risk-premia indexes than the overall manager sample.

The study then used a regression-based analysis, based on the four factors identified by Fama, French and Carhart to quantify how much of the alpha during the stated period can be attributed to risk premia. (Those factors are market capitalization, size, book-to-price and momentum.) It concluded that a select group of risk premia would have generated 80% of the alpha produced during that time. However, the study also showed that only active management could have found the remaining alpha. Most of that additional outperformance relied on various forms of successful timing:

- Market timing (either in the choice of asset classes or sectors)

- Risk premia timing (also known as "factor timing")

- Stock selection (timing individual stocks)

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.