Can China A Share Issuers Adapt to ESG Realities?

Blog post

June 13, 2018

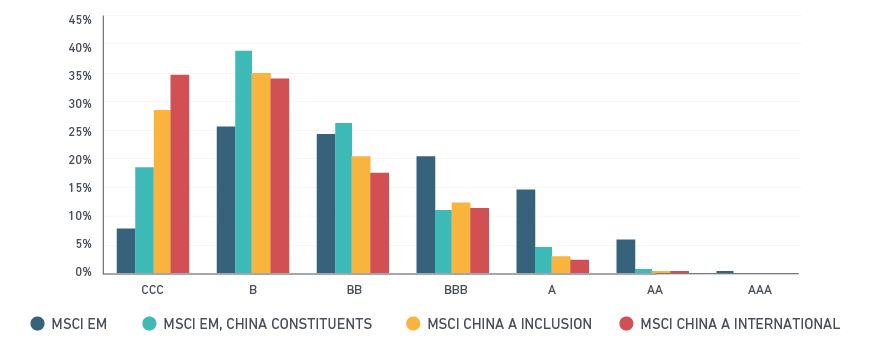

Now that China A shares have partially entered some mainstream MSCI indexes, institutional investors and other stakeholders are raising questions about Chinese constituents' ESG track records and potential risks from these new exposures in their portfolios. And these questions are fair. Of the 423 newly rated constituents of the MSCI China A International Index,1 we find that 86% fall below BBB, the mid-point for MSCI ESG Ratings.

However, investors should keep in mind that a skew towards lower ESG ratings is not unusual for emerging or newly covered markets. While there are challenges ahead for China A share issuers, we see indicators that suggest they may quickly adapt to the new ESG realities.

MSCI ESG Ratings distribution

Data as of May 28, 2018

An adjustment period is common, but in China, pressure from the top may speed progress

We've been here before. Historically, it has taken up to 18 months for newly issued MSCI ESG Ratings to stabilize, as companies conduct internal assessments of ESG risks and focus areas in response to questions from global investors. We observed similar dynamics when we expanded MSCI ESG Ratings coverage to South Africa, Japanese small caps and some Latin American countries.

What makes China's case stand out is that the evolution of ESG awareness among the corporate community is being promoted from the top. The gears have already been set in motion, not just by growing interest from global investors, but by a state-directed transformation from a resource-intensive, heavily industrialized economic structure to a services- and technology-focused economy, which will likely have a much lighter environmental footprint. In fact, a major factor behind the initial low ratings of many Chinese companies has been the lag in response to the higher bar set by recent state policy commitments, as elevated exposure to new compliance risks poses operational challenges for Chinese companies.

Near-term risks are real, but so is the potential for long-term success

The MSCI ESG Ratings distribution of the newly added companies provides a snapshot of the current status of China's transformation, and highlights the risks associated with evolving policy changes. Many companies, and especially the 58% that we classify as state-owned enterprises, find themselves in a tough spot: the targets set by policymakers are aggressive and enforcement can be very strict, while the infrastructure underlying their operations is massive and often outdated. This gap can be daunting, and could lead to heavy near-term capital expenditures, payment of penalties and even suspensions of operations.

The same top-down policy directives that create burdensome near-term compliance risks for companies, however, suggest the potential for a rather positive long-term ESG outlook. We observed something similar in European markets that experienced significant policy shifts towards stronger environmental stewardship in the mid-to-late 2000s. The short-term compliance challenges for European companies went hand-in-hand with policymakers' support for innovations directed at "greener" long-term economic growth.

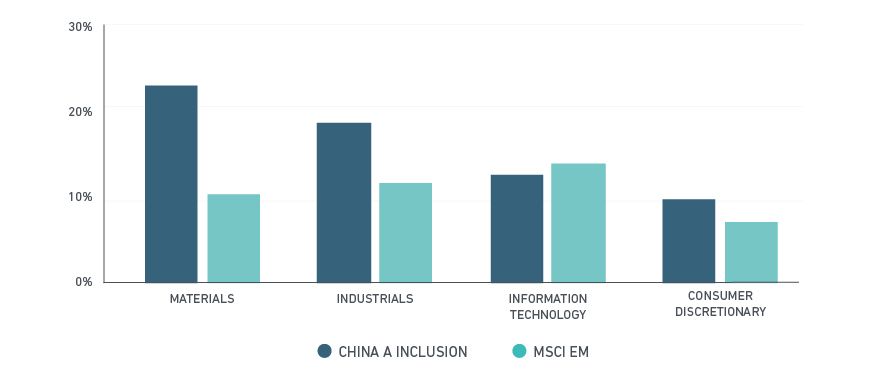

Ten years later, Chinese companies are working through their own transformation powered by sticks of strict mandates and carrots of subsidies and tax benefits. For example, Chinese automakers have already surpassed their global peers in percentage of sales from electric vehicles, and Chinese industrials lead their global sector peers in commercializing clean technology solutions. Both accomplishments can be attributed to state-level policies, such as new emissions reduction mandates and favorable tax structures.

Average percentage of revenue from clean technology by sector

Source: MSCI ESG Research, as of May 28, 2018

Greater transparency is needed, but engagement on ESG issues is growing

A challenge for sustainable investors will be to recognize the point at which companies in China shift from focusing on near-term compliance requirements to a longer-term outlook on sustaining global competitiveness. Meeting this challenge requires greater transparency regarding the key ESG risks that companies face and the strategies they devise to more effectively mitigate those risks in the long-term.

Roughly one-third of the inputs MSCI ESG Ratings rely on to measure companies' resilience to financially relevant ESG risks come from voluntary company disclosure. By our estimate, only 2% of MSCI China A International Index constituents publish sustainability reports and disclose financially relevant ESG metrics, compared to 34% of MSCI ACWI constituents. Hence, Chinese companies may be underutilizing a key communication channel that could help global investors differentiate between the companies that are still playing catch up in achieving compliance and those with robust risk mitigation strategies that position them well vis-à-vis global and domestic peers.

Additionally, MSCI contacts all rated companies to verify the data used in the ESG rating process. For Chinese issuers, the rate of responses providing actionable feedback has been low (only 3% of the MSCI China A International Index constituents), but we are encouraged by the large number of questions about the type of data that is useful to global investors, and that are used in our ratings methodology.

Evidence of an openness to change

MSCI ESG Research recently conducted a number of information and training sessions in China to share our perspective on global ESG investing trends, and to explain the MSCI ESG Ratings process and methodology. These sessions were organized with the support of the China Securities Regulatory Commission and Shanghai Stock Exchange and attracted over 300 corporate representatives. The outpouring of interest in ESG trends among listed companies in China is unprecedented in our experience, and shows a great deal of curiosity about what ESG issues are considered financially relevant for investors.

Further, the new framework for mandatory ESG reporting announced by the Chinese Securities Regulatory Commission, and the shift from "voluntary" ESG reporting to a "comply or explain" requirement by the Hong Kong Stock Exchange and Clearing are signs that addressing financially relevant ESG issues is becoming a new reality for Chinese companies, and an indication that more tools and data could soon become available to better inform investment decisions.

There are legitimate concerns around Chinese companies' transparency of business structure, accounting and business conduct that are likely to remain on investors' radar in the near term. Our research indicates that these issues can weigh on the MSCI ESG Ratings of companies in this market. However, the same regulatory and stakeholder forces that are fueling a transition towards a sustainable economy could also power the transformation towards globally accepted norms and standards in corporate behavior and practices. This includes foreign, as well as local investors, who may play a big part in shaping China's ESG evolution.

The MSCI China A International Index captures large and mid-cap representation and includes the China A share constituents of the MSCI China All Shares Index. It is based on the concept of the integrated MSCI China equity universe with China A-shares included.

The MSCI China A International Index captures large and mid-cap representation and includes the China A share constituents of the MSCI China All Shares Index. It is based on the concept of the integrated MSCI China equity universe with China A-shares included.

FURTHER READING:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.