Can Your Investment Strategy Work with China A Shares?

Blog post

June 27, 2018

Many institutional investors have long viewed China A shares as an inefficient market, suggesting that active strategies such as stock-picking can thrive. However, researching a universe of over 3,500 stocks comes with huge challenges, and may lead investors to question whether factor-based systematic strategies could have worked well with China A shares.

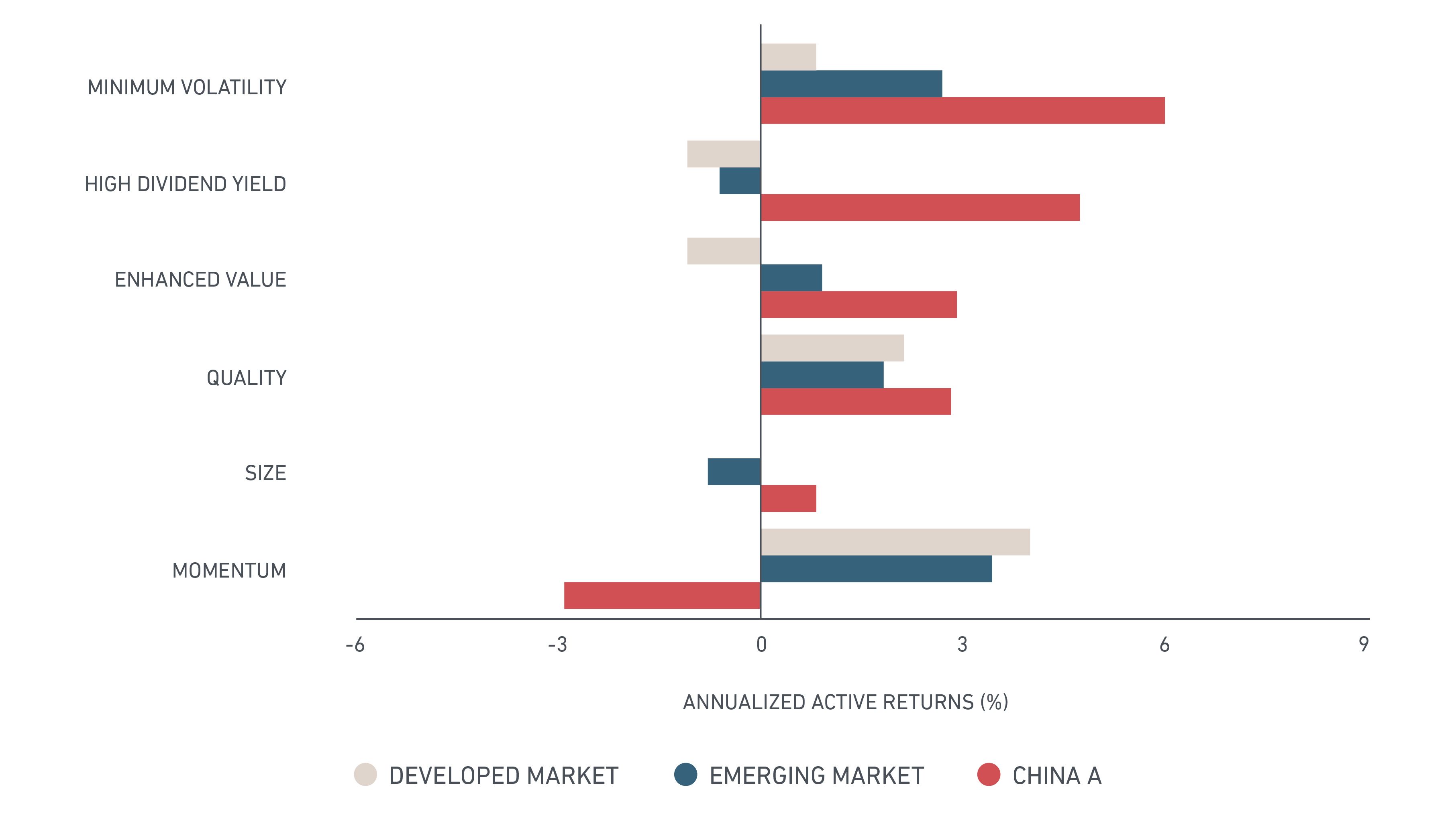

Our research indicates the short answer is "yes." Many of the MSCI China A factor indexes — minimum volatility, high dividend yield, value, quality, size and momentum — historically delivered higher returns than the China A market as a whole. Additionally, as we can see in the exhibit below, nearly all of the indexes delivered higher active returns in China A shares than in emerging and developed markets from November 2009 to March 2018.1

China A factor indexes generally have outperformed those for emerging and developed markets

Shown in annualized active returns, which show how factor indexes performed versus benchmarks for the respective region. Based on simulated performance from November 2009 to March 2018

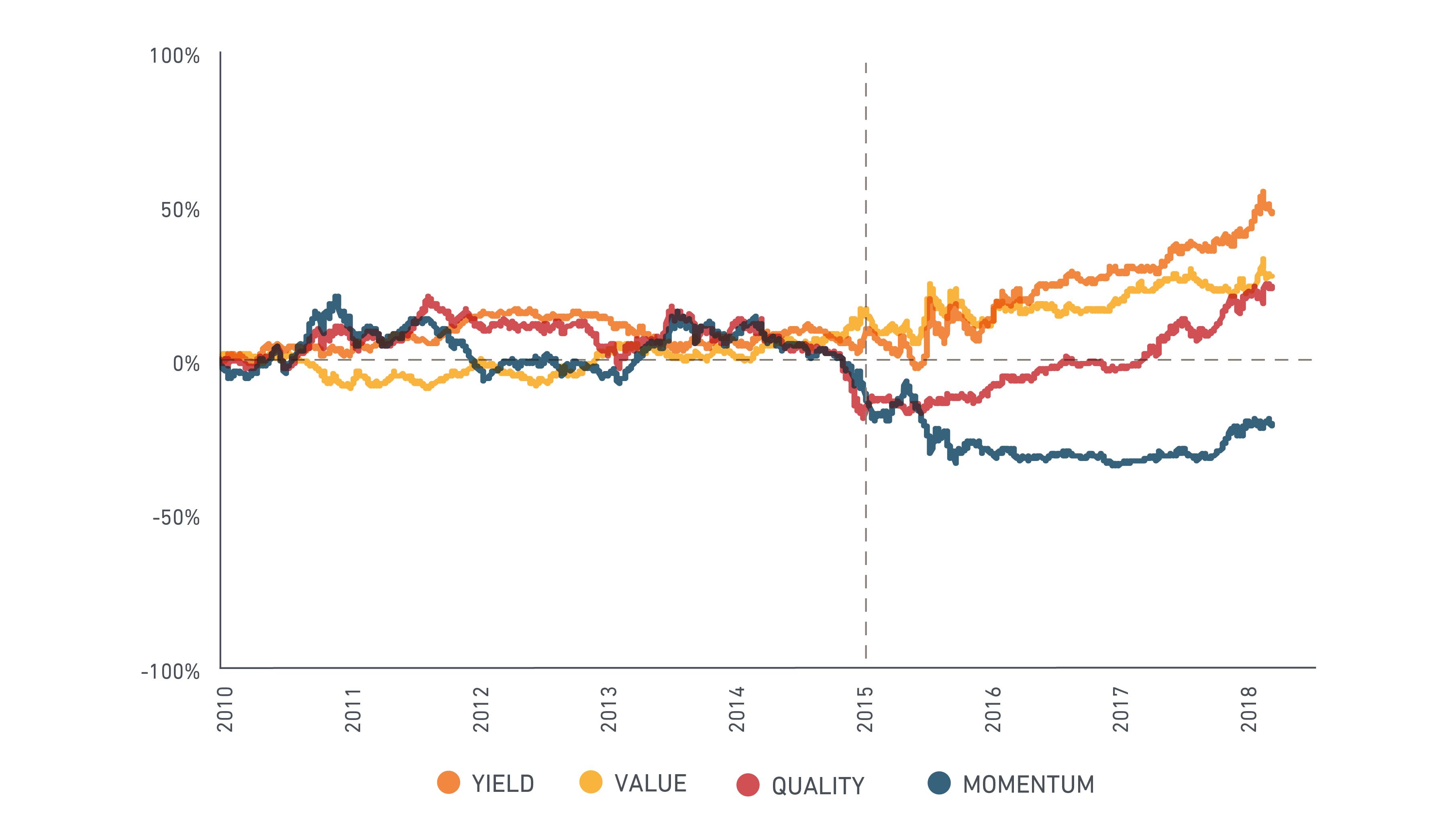

However, various MSCI China A factor indexes exhibited very different behaviors before and after 2015, potentially reflecting the launch of the Shanghai-Hong Kong Connect program. In particular, the value, high dividend yield and quality factors posted much stronger performance after 2015, while the momentum factor had a poor run.

Performance of Selected China A factor indexes diverges post-2015

Yield, value, quality and momentum factor performances above are based on simulated MSCI China A High Dividend Yield, Enhanced Value, Quality and Momentum Indexes respectively.

FIVE REASONS FOR FACTOR RETURNS IN CHINA

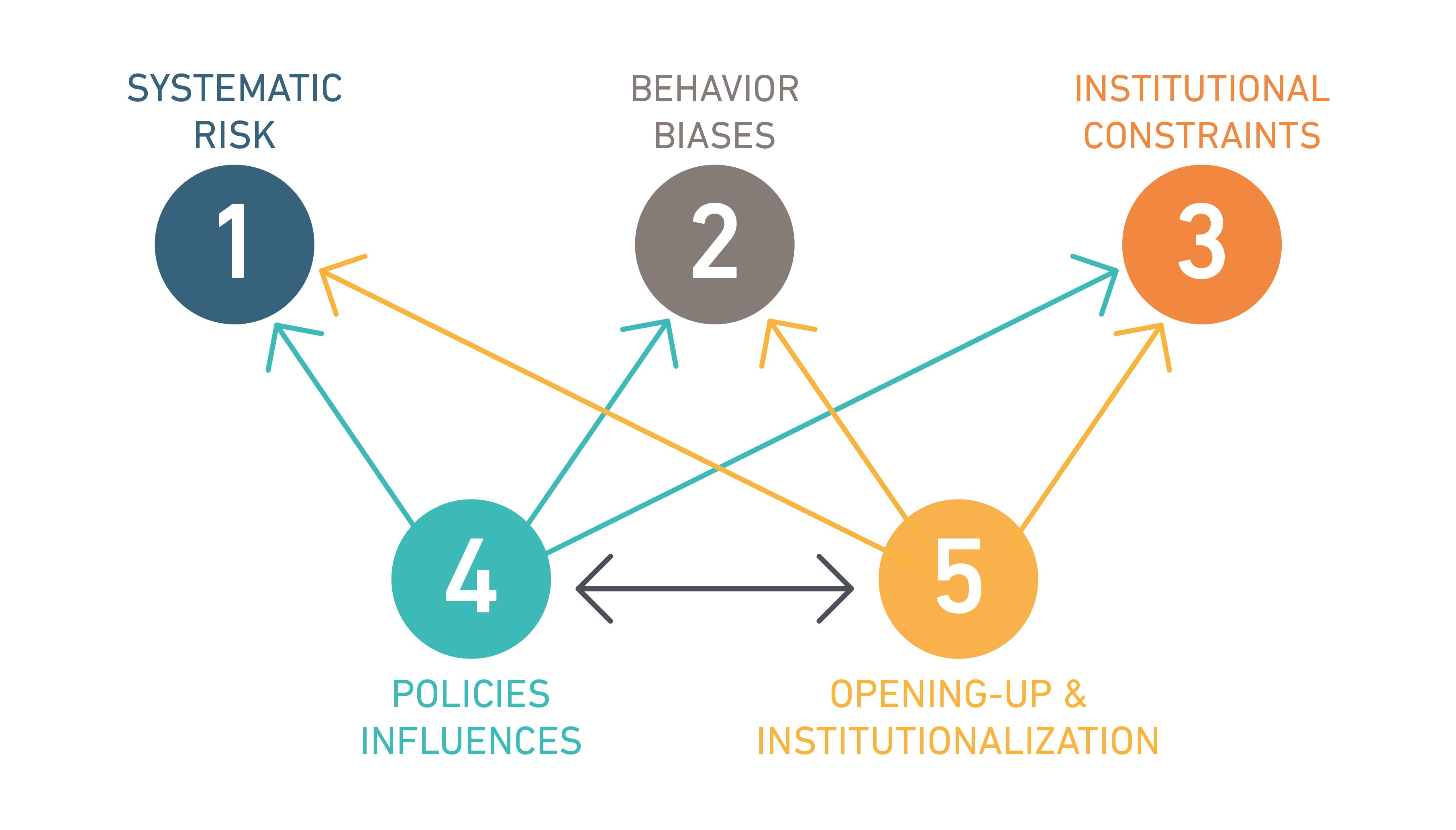

While we have seen evidence that factor-based strategies could have worked with China A shares, a key question is "Why?" Investors can harness the real power of factors only when they understand why factor strategies could demand long-term compensation of returns – and how these reasons apply to China A shares. The first three reasons are more universal in nature, while the last two reflect more specific influences of "China factors" on market behavior.

- Systematic risks: Risks to specific stock traits cannot be diversified away, and factors may have earned excess returns specifically because there was systematic risk attached. For example, the size factor was a case where investors bore higher credit and liquidity risk for the return compensation.

- Behavioral biases: Another reason factors may have earned excess returns is because of investor behaviors, such as chasing winners, overreacting or a preference for "local" securities. In China, retail investors sought short-term gains and overpaid for stocks with unrealistic growth projections, whereas patient investors in value and quality dividend stocks were rewarded over the period we examined.

- Institutional constraints: The third reason China A share factors may have earned excess returns are the frictions and flows that arise from regulatory and industry practices and constraints. For example, many institutions faced short-term pressures, such as monthly performance ranking and quarterly internal asset allocation evaluations. This has led to a preference for higher-risk strategies, creating opportunities for low volatility stocks.

- Influence of government policies: Since 2014, China securities regulators have been actively pushing companies to pay higher dividends to shareholders. This has contributed to a positive return premium on dividend-paying stocks in recent years. On the other hand, the lingering perception of state influence, particularly from the so-called "national team" (a market-stabilization fund established during the 2015 crisis), can distort the price discovery process and make the market less efficient.

- Opening of China A Shares market: One direct consequence of the opening of the China A shares market and their partial inclusion in the MSCI Emerging Markets Index is greater institutional participation in the market. Institutional investors historically have been more attuned to stocks with attractive valuation, dividend payout and stronger fundamentals, which may help explain why yield, value and quality factor indexes performed better during the past two to three years.

How China A shares dynamics may affect factor indexes

While most factor indexes historically outperformed in the China A shares market during our study period, an in-depth understanding of the "Chinese characteristics" of various factors may be helpful to investors — especially as this government's policies and this market continues to evolve.

The author thanks Chin Ping Chia for his contribution to this blog post.

1 The only exception was momentum, which showed strong performance in global markets but underperformed in China A. This article contains analysis of historical data, including backtested performance results. There are frequently material differences between backtested performance results and actual results subsequently achieved by any investment strategy. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance.

Further Reading

Vive la Différence: Active Factor Strategies in China A Shares

The World Comes to China

Are You Ready for China A Shares?

China A-shares: Too big to ignore

What do rising interest rates mean for minimum volatility strategies?

What valuations tell us (and don't tell us) about future factor returns

Seeking defensive yield in emerging markets and Asia

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.