China A Shares: The Journey Continues

Blog post

October 10, 2018

As China continues to open its capital markets to global investors and accessibility standards have improved, MSCI recently launched a consultation to explore increasing the weight of A shares in the MSCI Emerging Markets Index. Ultimately, we seek to reflect the full investable opportunity set — all of China accessible to global investors — in the benchmark, as we do in all MSCI Global Investable Market Indexes.

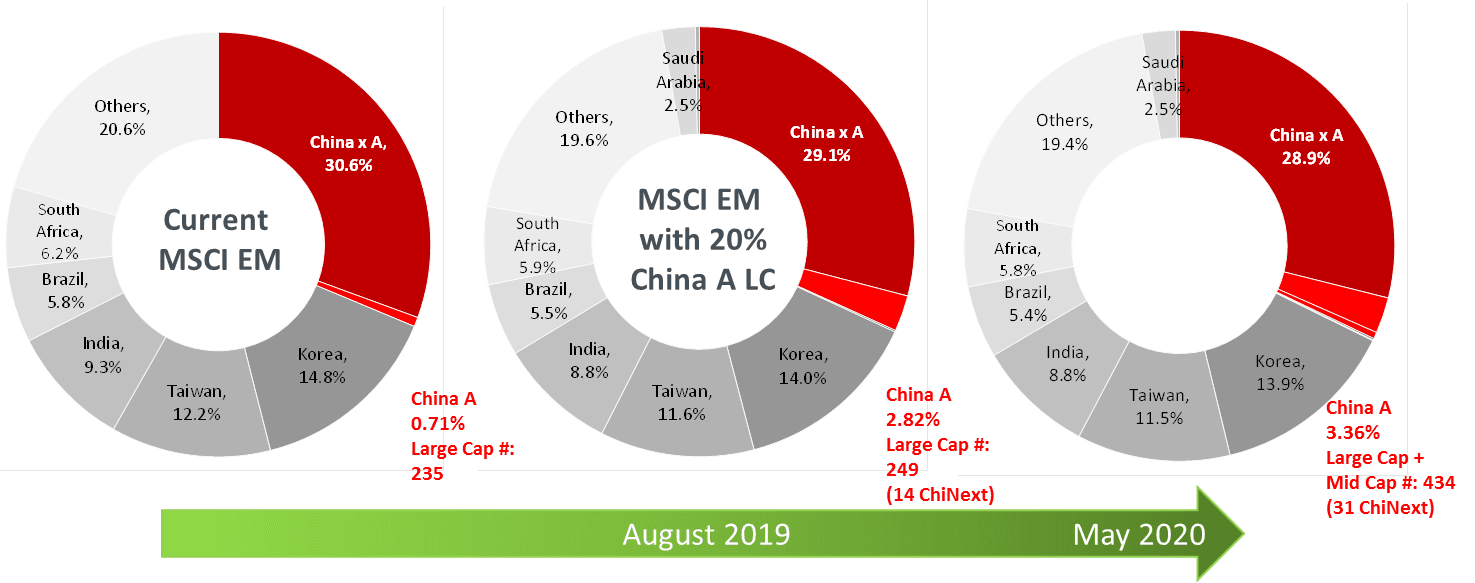

CURRENT AND PROPOSED CHINA A SHARES INCLUSION

MAPPING THE NEXT PART OF THE JOURNEY

This new consultation, explored in more detail in our new paper, Proposed: Increasing China A shares weighting in MSCI indexes, was primarily motivated by strong validation for the Stock Connect trading channel, which allows international and Mainland Chinese investors to trade securities in each other's markets, and continued improvements on overall market accessibility. There are three core proposals:

1) Increase the inclusion factor of the 235 China A large-cap shares from 5% to 20%

The successful initial inclusion provided strong evidence that Stock Connect has the capacity to absorb a much larger capital flow. Only 3% to 7% of the daily limit was consumed during the inclusion days this summer, suggesting there is still ample capacity to channel capital into A shares on a daily basis. Additionally, access to offshore Renminbi (CNH) for trade settlements during inclusion was smooth, as the Hong Kong Monetary Authority worked closely with banks and other financial intermediaries to provide adequate CNH liquidity to market participants.

2) Bring 168 China A mid-cap shares into the index at a 20% inclusion factor

The initial inclusion of 235 China A large-cap shares into the MSCI Emerging Markets Index was a special transition measure to help first time A shares investors cope with such a large number of additions. The inclusion of mid-cap shares would align the China A shares component methodologically to the rest of the markets included in the MSCI Global Investable Market Index, which includes both large- and mid-cap representation.

3) Admit the ChiNext board in Shenzhen to the list of eligible stock exchange segments

Since launching in 2009, the Shenzhen-based ChiNext board has grown to include 732 stocks, mainly technology companies. It represents about one-fifth of the market capitalization and the number of listings in the A shares market. ChiNext has become an increasingly large segment of the China A opportunity set.

POTENTIAL SPEEDBUMPS

Despite significant steps, we believe further progress could be made to align market accessibility standards with the rest of the emerging markets. Among the key issues to be discussed include:

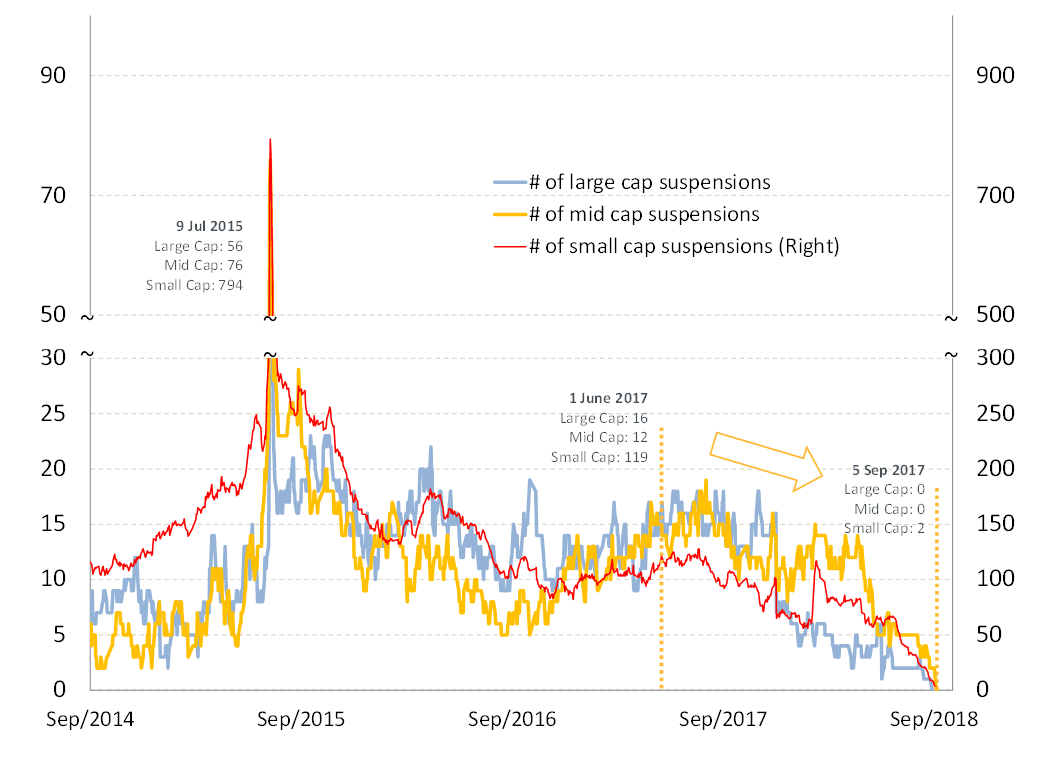

Progress on trading suspensions. Trading suspensions became a huge concern for international institutional investors after the 2015 market sell down; it was a large stumbling block during the 2016 index inclusion discussion. Currently, there are no trading suspensions in the MSCI China A Large Cap and MSCI China A Mid Cap indexes and only two in the MSCI China A Small Cap Index.

CHINA A TRADING SUSPENSIONS HAVE TRENDED DOWNWARDS

However, investors have expressed the most concern about sustainability and irreversibility of improvements. Additionally, trading suspension characteristics in China remained unique compared to other emerging markets. Suspensions happened across size segments and most lasted more than one day, with some lasting more than three months.

Alignment of settlement cycles. China's short settlement cycle is misaligned with other markets and could pose operational challenges and risk to global investors. Stock Connect provides market solutions for buy trades. However, the short cycle leaves very little time to validate sell orders, especially for those based outside Asian time zones.

Access to hedging and derivatives. Exchange restrictions on A shares index licensing of certain listed futures, options, and leveraged and inverse financial products, both onshore and offshore, have hampered investors' ability to manage risk and gain exposure beyond the cash market. Increasing A shares' weight could make this issue even more pronounced.

Access to onshore Renminbi (CNY) for stock settlement. Based on our assessment, the current pool of offshore CNH liquidity seems sufficient to address the current inclusion multiple. However, providing direct access to CNY for stock settlement could represent a more efficient foreign exchange option for international institutional investors and financial intermediaries were the weighting to increase.

MILES TO GO BEFORE WE SLEEP

Over the next several months, we will engage with global investors. We also will monitor the progress of the relevant authorities and other stakeholders to address these and other issues as the inclusion journey takes us down a long road toward a more open and integrated Chinese capital market.

Further Reading

Proposed: Increasing China A shares weighting in MSCI indexes

Consultation on further weight increase of China A shares in the MSCI indexes

Can your investment strategy work with China A shares?

The World Comes to China

Are You Ready for China A Shares?

China A-shares: Too big to ignore

Making China Simple Again

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.