Climate Indexes' Year in Review: The Journey Toward a Low-Carbon Transition

- MSCI Climate Indexes underperformed relative to their parent indexes in developed markets, but they demonstrated greater resilience in emerging markets.

- An energy sector rally as well as the relative outperformance of companies with low valuations contributed to the underperformance.

- While the climate indexes underperformed, long-term decarbonization commitments from major energy-consuming nations may support the low-carbon transition going forward.

The performance of Climate Indexes across regions

Loading chart...

Please wait.

The table shows performance of the regional variations of the MSCI Low Carbon Leaders, MSCI Low Carbon Target, MSCI Climate Action, MSCI Climate Change and MSCI Climate Paris Aligned Indexes in 2022. The bar chart shows the active returns of the of the same indexes, by region/country, in 2022 as well as for each quarter in 2022.

Strong outperformance of the energy sector in developed markets

Higher energy prices with greater volatility characterized the year for the energy markets. The energy sector, which is represented by the MSCI ACWI Energy Index, outperformed the MSCI ACWI Index by 52.4% in 2022. The outperformance of energy-sector companies contributed to the underperformance of the MSCI Climate Indexes as they usually have relatively lower allocations to the energy sector (as shown below). This contrasted with the underperformance of energy sector between Nov. 30, 2018, to Dec. 31, 2021, by 16.6% on an annualized basis, which contributed to the outperformance of the MSCI Climate Indexes over that period.

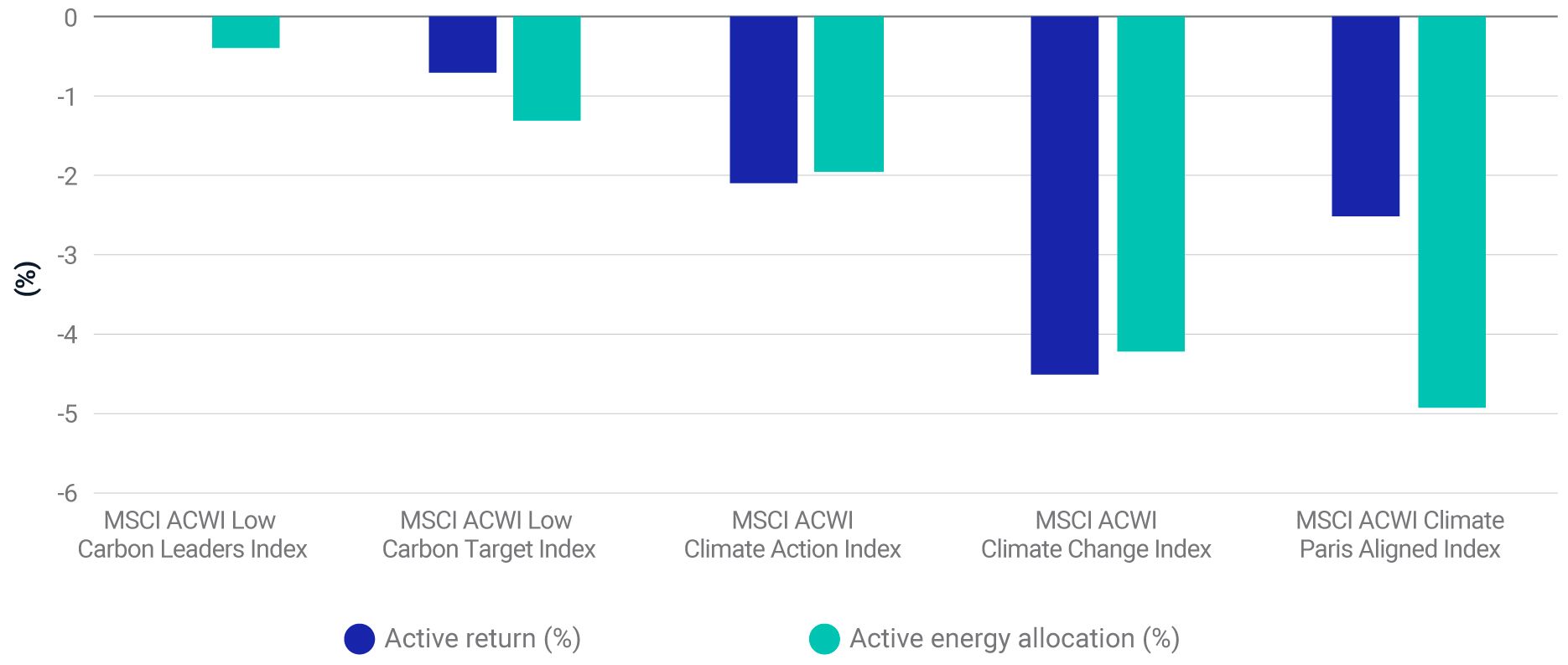

Relative performance vs. active allocation to the energy sector

The chart shows active return vs. the average active allocation to the energy sector for respective MSCI ACWI Climate Indexes in 2022.

Nonetheless, the MSCI Climate Indexes demonstrated varied performance. We observed that the MSCI Climate Indexes that had tighter controls over sector exposures, such as the MSCI ACWI Low Carbon Leaders and ACWI Low Carbon Target, outperformed other MSCI Climate Indexes that had larger underweights for energy-sector companies.

In contrast, the emerging markets (EM) climate indexes showed more resilience relative to the developed-market indexes. This was interestingly driven by the underperformance of the energy sector in EM compared to the MSCI Emerging Markets index by 4.1%. The underperformance of the MSCI EM Climate Change and EM Climate Paris Aligned indexes was contributed primarily by the relative outperformance of companies with low valuations.

The performance reversal of other industries also played a role

While the performance of the energy sector played an important role in the performance of MSCI Climate Indexes in 2022 (shown below), the story for the year wasn't just about energy-sector performance. Since the MSCI Climate Indexes are generally overweight on the information technology sector, this has historically aided their performance given the outperformance of the sector in the past. A macroeconomic scenario occurred last year that was more conducive for cheaper companies, which led to a correction for growth stocks and the information technology sector.

In addition, a rise in geopolitical tensions translated into positive momentum for aerospace and defense companies. As the MSCI Climate Indexes exclude controversial-weapons companies, the outperformance of aerospace and defense companies adversely impacted their performance.

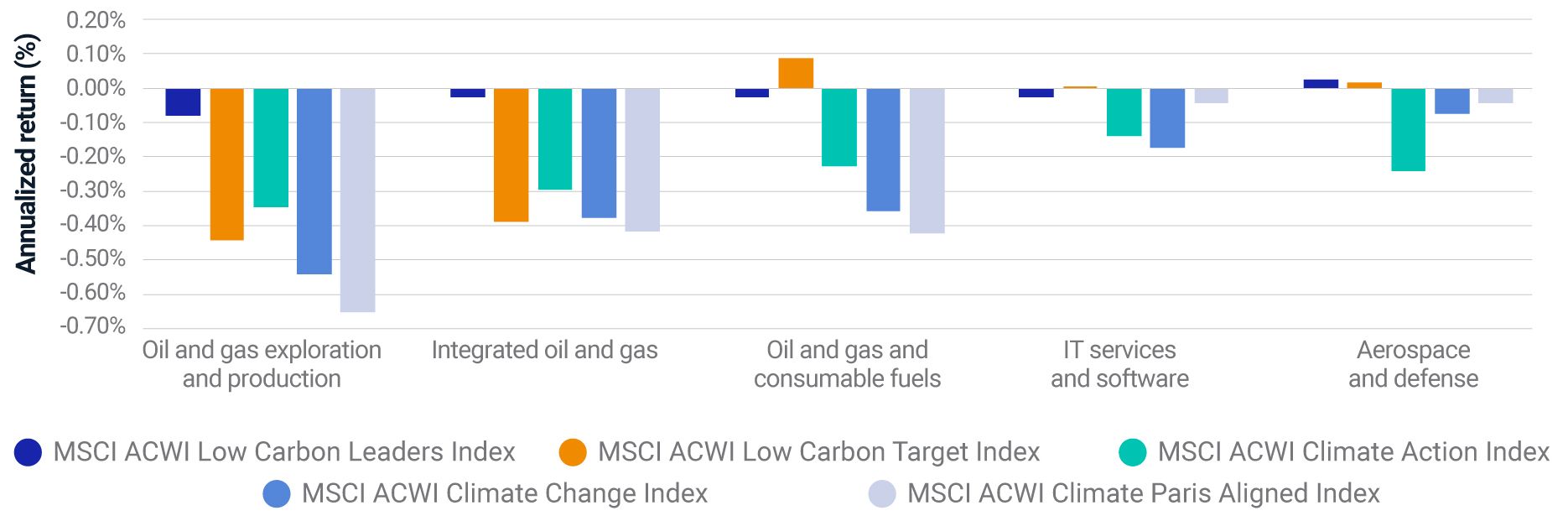

Industry performance reversal in 2022 impacted climate indexes

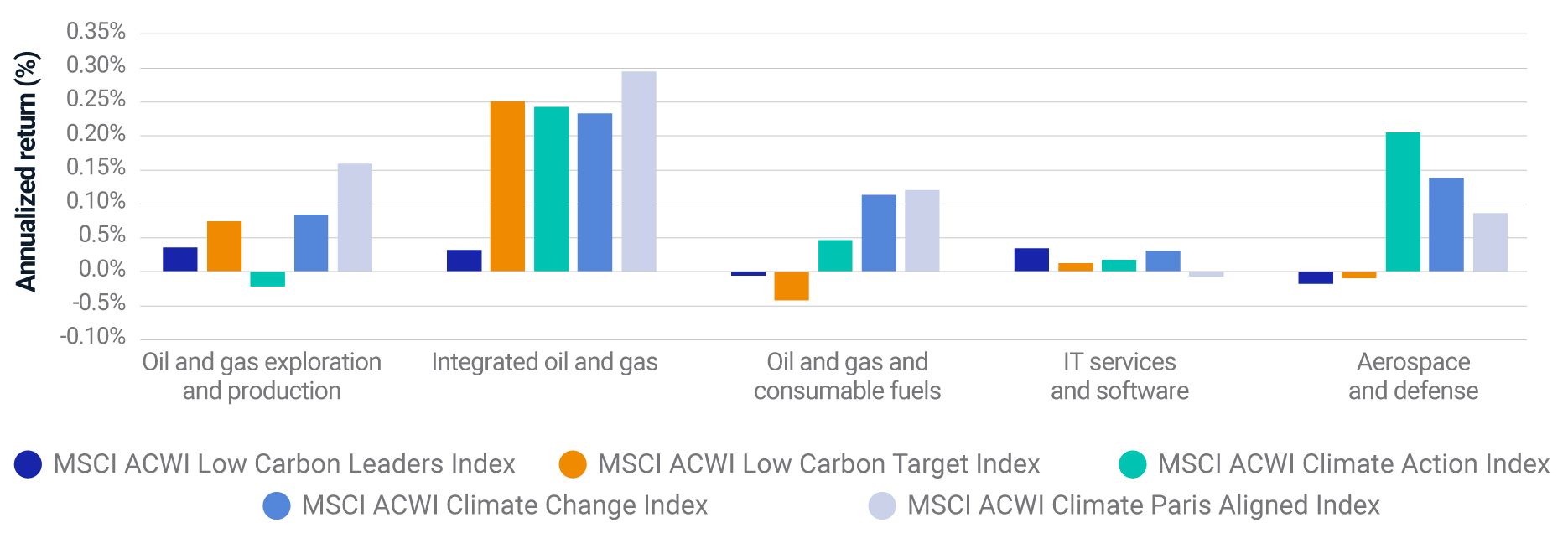

The same industries contributed to performance (Nov. 30, 2018, to Dec. 31, 2021)

The charts show the performance contribution of select top industries using the MSCI Global Equity Factor Model risk model (EFMGEMLT). The upper chart shows the performance contribution in 2022 and the lower chart shows the performance contribution for the same industries between Nov. 30, 2018, to Dec. 31, 2021.

Factor allocations were also impactful

In addition to the industry allocations, factor allocations (especially value and carbon efficiency) also were key contributors to the performance of climate indexes. Value was a relative outperformer in 2022, primarily driven by the inflationary environment and higher interest rates, an environment that has generally been favorable for value stocks over growth stocks. Value's outperformance contributed to the underperformance of the MSCI Climate Indexes (shown below), which had smaller allocations to stocks with lower valuations. However, the MSCI Low Carbon Leaders and Low Carbon Target indexes were less impacted by the value outperformance due to their strict controls on tracking error, which produced a lower active allocations to companies with low valuations.

Value outperformance detracted from the climate indexes' performance

The chart shows the aggregate performance contribution of value factors using the MSCI Global Equity Factor Model risk model in 2022.

MSCI ACWI Climate Indexes aim to achieve a lower carbon footprint than the broader MSCI ACWI Index, which led to higher allocations to carbon-efficient companies within each sector. Their performance was also supported by the relative outperformance of both intra-sector, carbon-efficient companies, as well as better-rated ESG companies.

A recap of decarbonization

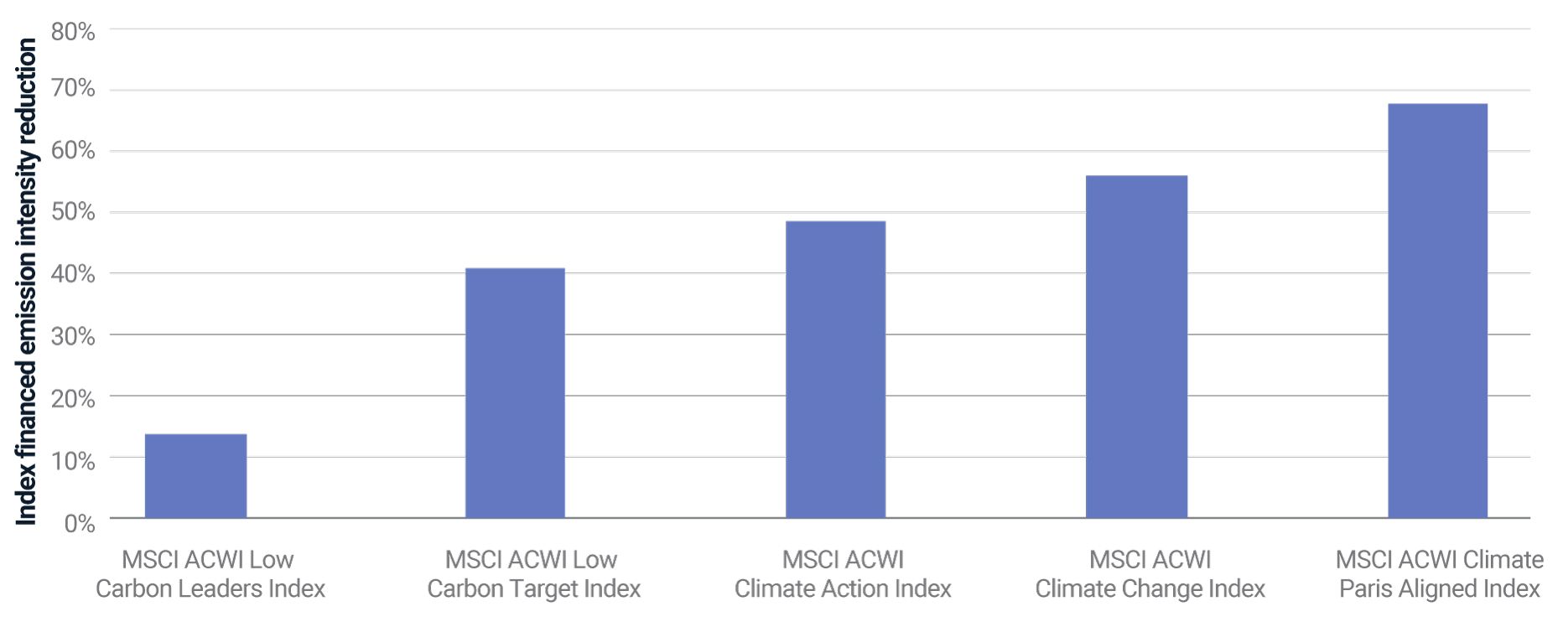

Institutional investors need to be mindful of the risk-adjusted return characteristics of their allocations in accordance with their fiduciary responsibilities. This would hold true for their climate allocations as well, but an important criterion for assessing the climate indexes would be their success in meeting respective climate objectives (especially decarbonization relative to the broad market-cap allocations). In 2022, the MSCI ACWI Climate Indexes had a significantly lower carbon footprint compared to the MSCI ACWI Index.

The decarbonization of climate indexes

Average % reduction in Index financed emission intensity (tCO2/$ million EVIC) for ACWI climate indexes relative to MSCI ACWI for 2022. The average is computed based on the month end Index financed emission intensities.

The road toward the low-carbon transition

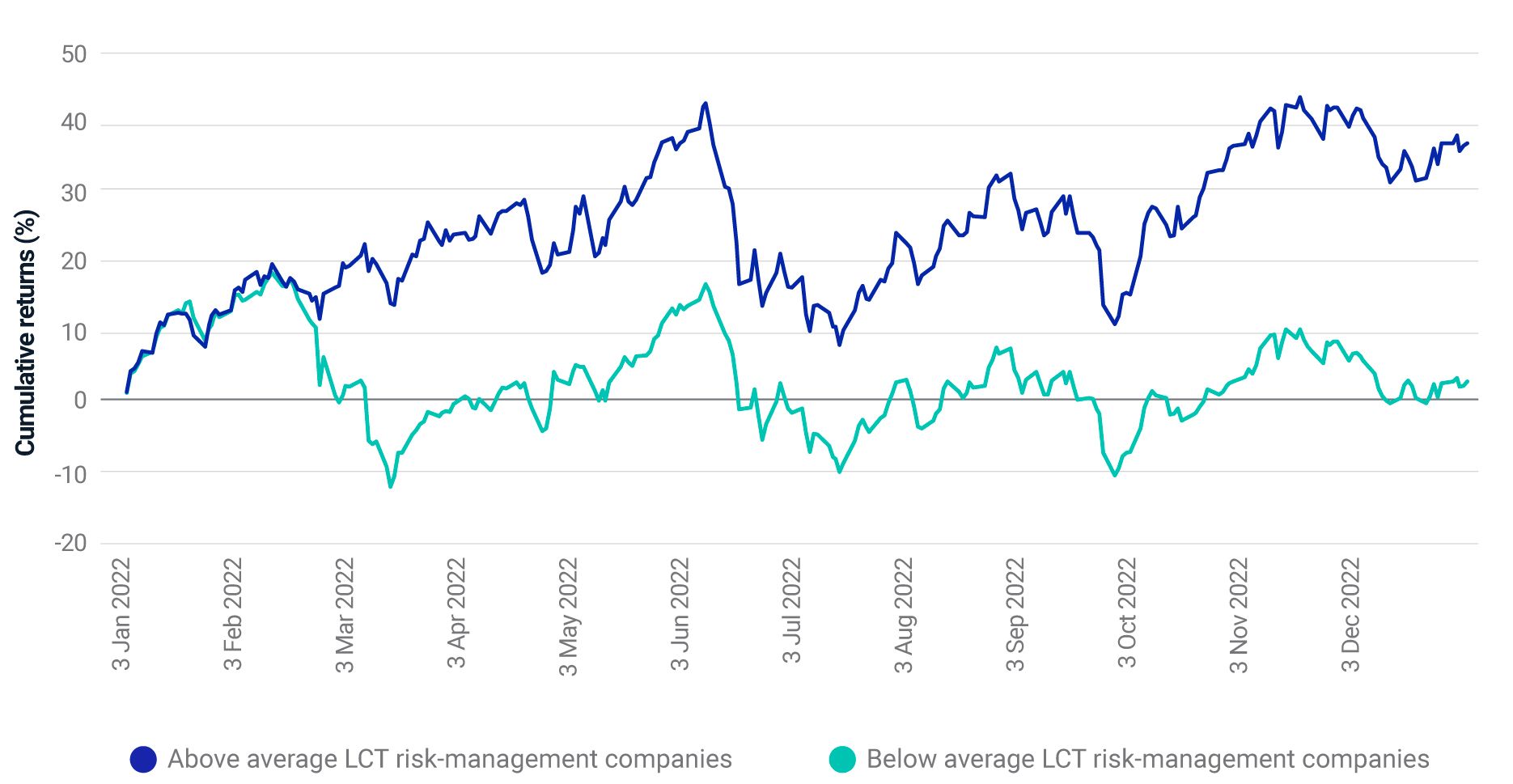

We have previously established that the MSCI Climate Indexes' underperformance relative to the MSCI ACWI Index was largely driven by the outperformance of the energy sector. It is important to note that even within the energy sector, companies demonstrating greater emphasis on the low-carbon transition (LCT) outperformed their sector peers having weaker management of low-carbon transition risks (shown below) thus highlighting the importance of managing low-carbon transition risks.

Performance of energy-sector companies

Cumulative returns for above average and below average LCT risk-management companies. Dec. 31, 2021, to Dec. 30, 2022.

With major energy-consuming nations such as China, the U.S., European Union (EU) and India, among others, remaining firm on their long-term decarbonization commitments, we believe that a focus on the low-carbon transition will continue. For instance, the EU's "Fit for 55" and "REPowerEU," the U.S. Inflation Reduction Act, and China's 14th five-year plan, combine legislative and fiscal stimulus to accelerate the long-term low-carbon transition towards the net-zero world. A continuance of the higher level of energy prices may incentivize the adoption of clean and efficient energy technologies at greater pace, which will also be supportive of the low-carbon transition. Although it remains to be seen how these factors may impact the performance of energy stocks as well as of climate indexes going forward.

The authors would like to thank Xinxin Wang for her contribution to this blog.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.