Does Turkey offer lessons for managing emerging-market currency volatility?

Blog post

August 15, 2018

Battered by high inflation, poor fundamentals and now a bitter dispute with the Trump administration, the Turkish lira has plunged 40% in value so far this year. But Turkey is not alone, as currencies of other emerging markets have also suffered this year. Yet investors do not generally hedge currency risk in their emerging markets equity portfolios, believing that these currencies provide a tailwind to emerging-market equity performance or that the cost of hedging these currencies is too high. However, currency volatility has risen steadily over the last decade. Is it time to rethink this approach?

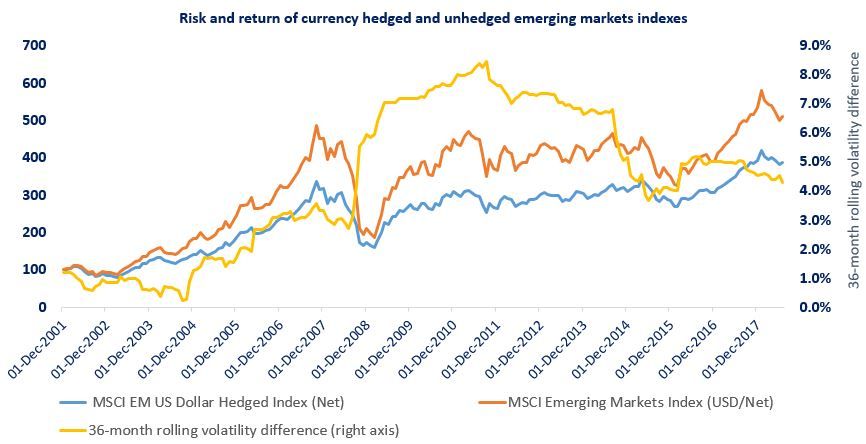

The chart below looks at how emerging-market currency hedged and unhedged indexes have performed over time from the perspective of a U.S.-based investor. While the unhedged index outperformed the hedged index, the difference in risk (measured on a 36-month rolling basis) has increased dramatically. How can investors address these risks? The answer may be to take a dynamic or adaptive hedging approach, using a metric such as the currency volatility factor.

Emerging-market currency volatility has increased over time

One can use the currency volatility factor1 to express a view on risk aversion, such as reducing uncertainty by hedging currency exposure. By subtracting the long-term (six months) average daily volatility from the short-term (one month) average volatility, we can observe when short-term average volatility exceeds long-term average volatility (the result becomes positive), indicating that risk is increasing. This may help the investor decide to hedge currency exposure.

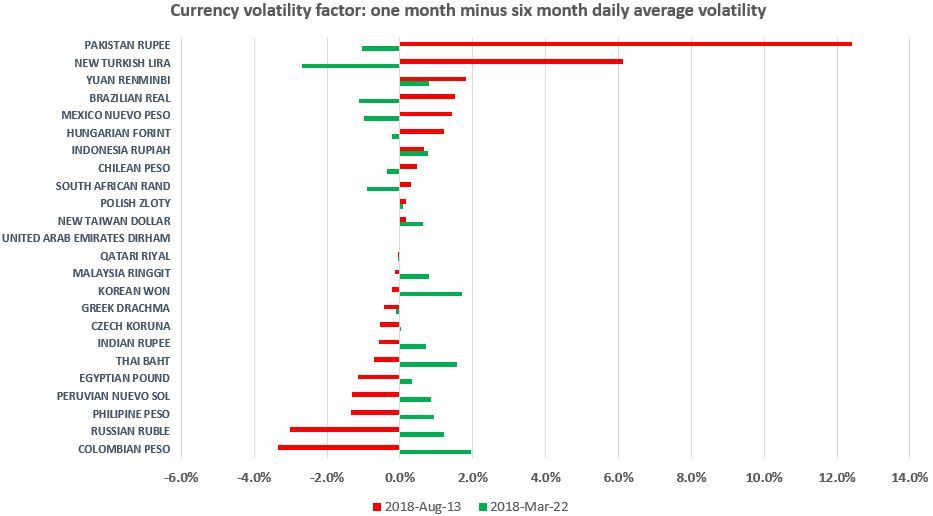

Looking at individual emerging-market currencies, we find the Pakistan rupee and new Turkish lira had substantial positive indicators since March 2018. But these currencies are not alone; this factor has turned positive for many of the emerging markets currencies since the Trump administration proposed tariffs in March, suggesting a possible link between trade wars and currency volatilities.

Currency volatility has risen in key emerging markets since March

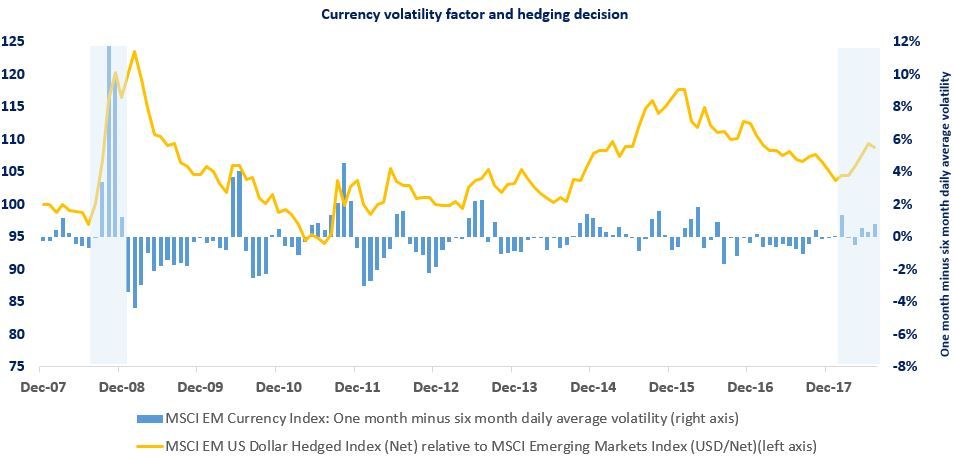

While currency hedging decisions can be applied at the individual currency level, the exhibit below illustrates that one can take a broad view on currency hedging for emerging-market currencies in aggregate. We used the volatility factor derived from the MSCI EM Currency Index as a proxy for currency risk exposure in the MSCI Emerging Markets Index. In the exhibit below, we see that the volatility factor indicator turned positive earlier this year, as uncertainty surrounding global trade wars started to unsettle global equity and currency markets. Currency hedging might have helped to reduce volatility in this instance.

How hedging currencies can affect performance

Whether to hedge or not clearly depends on an investor's risk-return preferences. Most emerging-market equity investors do not hedge their currency exposure. But with currency volatility rising over the past decade, investors may want to reconsider this approach. A dynamic or adaptive hedging approach may help.

The author thanks Anil Rao for his contribution to this post.

1 Currency volatility factor is one of the four factors that is used in the MSCI Adaptive Hedge Indexes to determine the final hedge ratio of each currency

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.