Don’t Let CoCo Bond Risk Sneak Up On You

Blog post

September 18, 2017

Convertible contingent securities — known as "CoCo bonds"-- are a popular form of hybrid debt, but they can be hard to value when issuers head into troubled waters. These securities are a form of risky debt (typically issued by European financial institutions) that convert to equity when a predetermined trigger is met, such as when the issuer's capital or balance sheet plunges in value. Institutional investors have been attracted to the 5%-7% yields paid by these securities.

But figuring out when a CoCo bond is at risk of being converted to equity — effectively eradicating the value of the bond — can be tricky. When Spain's Banco Popular collapsed in June, the value of its CoCos was completely wiped out, as depositors withdrew their money en masse. (The bank was acquired by Banco Santander for €1.) How can investors spot indications of a potential collapse, especially in a bull market? The answer may lie in having a dedicated risk model that picks up on early warning signs.

One of the key problems in valuing CoCos is that they do not have a long history. These hybrid securities, which became a popular way of financing European banks after the 2008 financial crisis, haven't been tested in any major market downturn. Plus, how they convert to equity from debt can be somewhat opaque. And, when a collapse occurs it can happen very quickly, as negative headlines may lead to a run on the bank, with swift and hard implications for CoCo bonds.

Picking up on tail risk

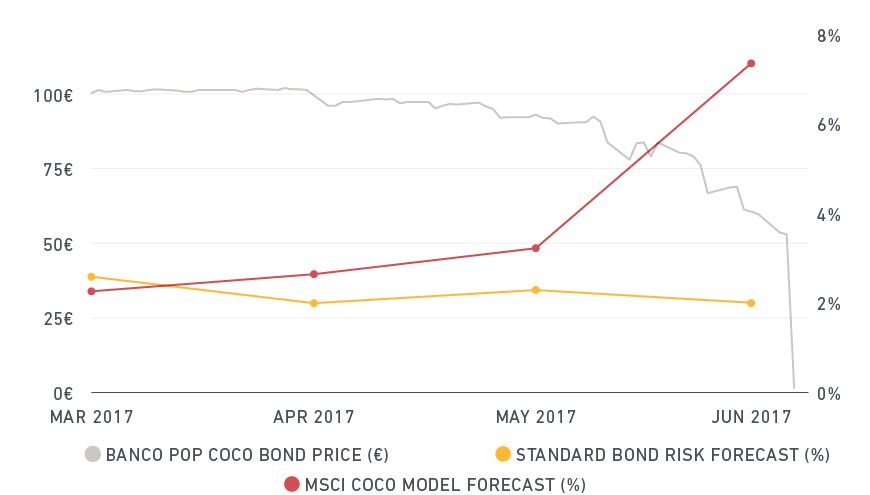

Standard fixed-income models tend to ignore the conversion feature of CoCo bonds and thus can paint a misleading picture of risk. In our analysis, we studied the risk of Banco Popular-issued CoCo bonds failing using MSCI's Contingent Convertible model. Our post-event measure of this ex-ante risk is 95% Value at Risk for a one-day horizon, as a percentage of market value.

MSCI's model detected rising risk of Banco Popular's CoCo bond

Source: Thomson Reuters, used with permission

The CoCo model and the MSCI Generic Bond model provided very different indications of forecasted risk. As shown above, the CoCo model successfully forecast rising expectations of conversion, resulting in declining valuations and growing risk to the investor. The standard bond model's risk forecast failed to pick up the growing expectation of a tail event, providing a misleading insight.

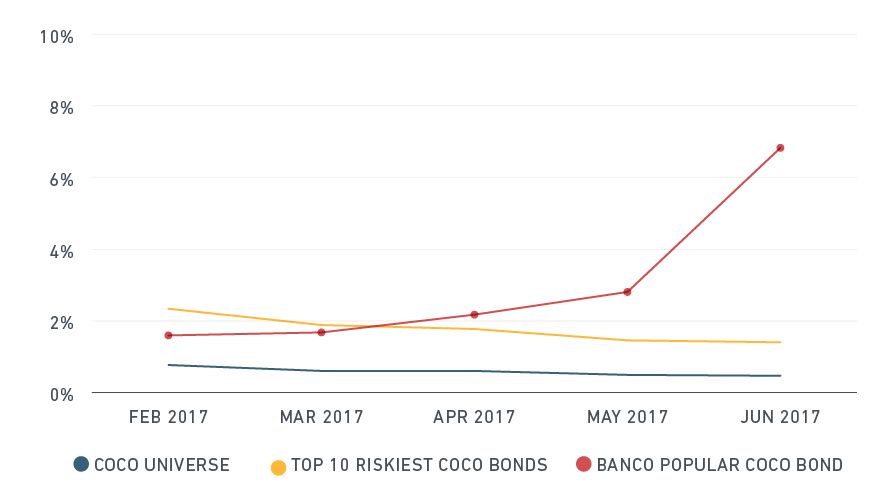

Using our risk model, we can readily see (below) a steep increase in the risk of Banco Popular CoCo bonds failing relative to the average risk forecast across the universe and to the average forecast of the top 10 riskiest bonds. While the risk of Banco Popular CoCo bond was always higher than the average of the entire universe, in February and March it was lower than the top 10 average. In April and May, however, the risk of the Banco Popular CoCo bond escalated, and by June was going through the roof, far surpassing the rest of the universe.

MSCI Risk Forecasts for Banco Popular CoCo Risk vs. CoCo Bonds

Source: MSCI

CoCos are here to stay

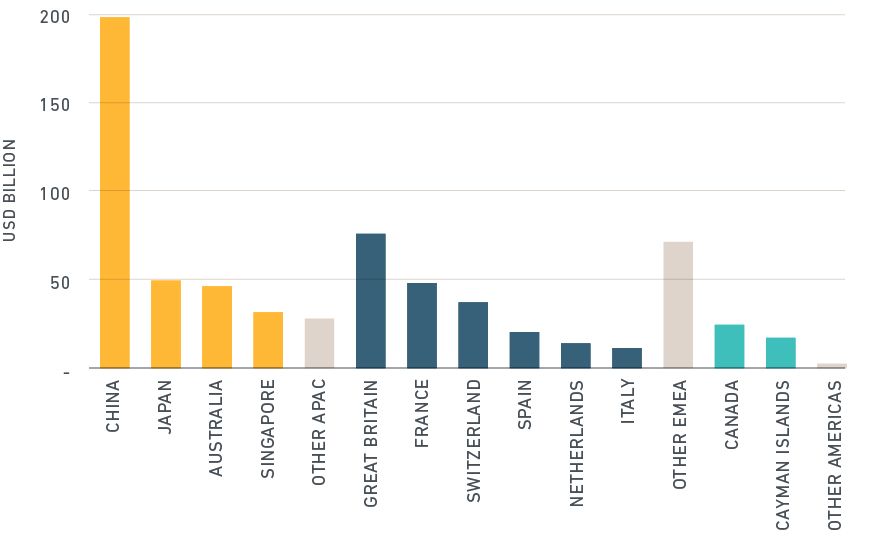

CoCos have become very popular financing tools since the financial crisis. Issuance has continued, mostly in APAC recently, with $675 billion in CoCo bonds outstanding worldwide (see exhibit below). For the foreseeable future, they are here to stay, offering higher yields in a low-yield environment. But their complex and somewhat opaque features make investing in them challenging, especially when an issuer faces a sharp reversal in fortune. A dedicated model offers a new tool to evaluate the potential risks from this market.

Global CoCo issuance totalled $675 billion

Source: Thomson Reuters, used with permission

The author thanks Andy Sparks for his contributions to this post.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.