Economic Exposure in Global Investing

Blog post

July 8, 2015

As companies expand their footprint globally, the geographic distribution of their revenues evolves over time and their economic exposures may diverge from their country of domicile and primary listing. We believe that this raises a critical issue for institutional investors.

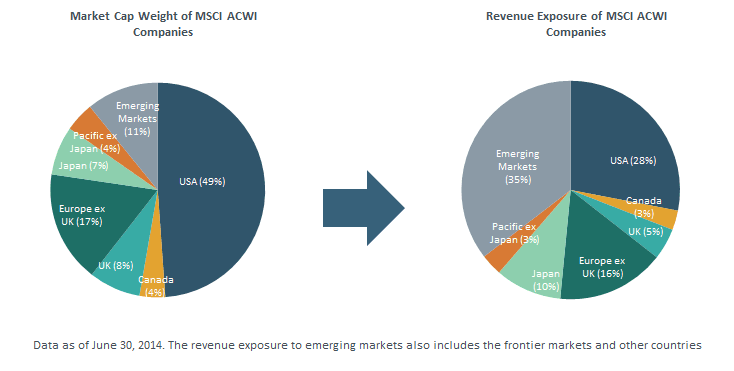

Indeed, with the continued integration of world markets, companies across different size segments are increasingly exposed to economic activity beyond their domestic borders. Consider this: As of June 30, 2014, Korea-domiciled Samsung Electronics Co. derived 90% of its revenues outside Korea and close to 50% outside emerging markets (EM). Yum Brands, a consumer discretionary company headquartered in the United States, generated 53% of its revenues from China and only 22% from the United States. We can see in the below exhibit how creating an index based on revenue exposures provides a striking contrast to one based on market capitalization.

Market Cap vs . Revenue Exposure of MSCI ACWI Index

In this global context, it is crucial to understand the geographic distribution of company revenues as it may enhance the investment decision processes for constructing and managing global portfolios. To that end, the MSCI Economic Exposure Indexes aim to reflect the performance of companies with high economic exposure to specific regions. Managers can use these in a number of different ways:

- Tilting their portfolios towards domestic stocks with higher international exposure.

- Creating a more "pure" domestic bias in their portfolio.

- Dynamically allocating to (or away from) securities in countries or regions that display momentum.

- Increasing or decreasing allocations via passive exposures.

- Developing an alternative way to diversify globally through a portfolio of companies with diversified regional exposure.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.